PSEG Grows Regulated Rate Base to $36B While Managing Nuclear Assets and Regulatory Challenges

Public Service Enterprise Group Inc advances its capital investments and operational stability through regulated utilities and nuclear generation.

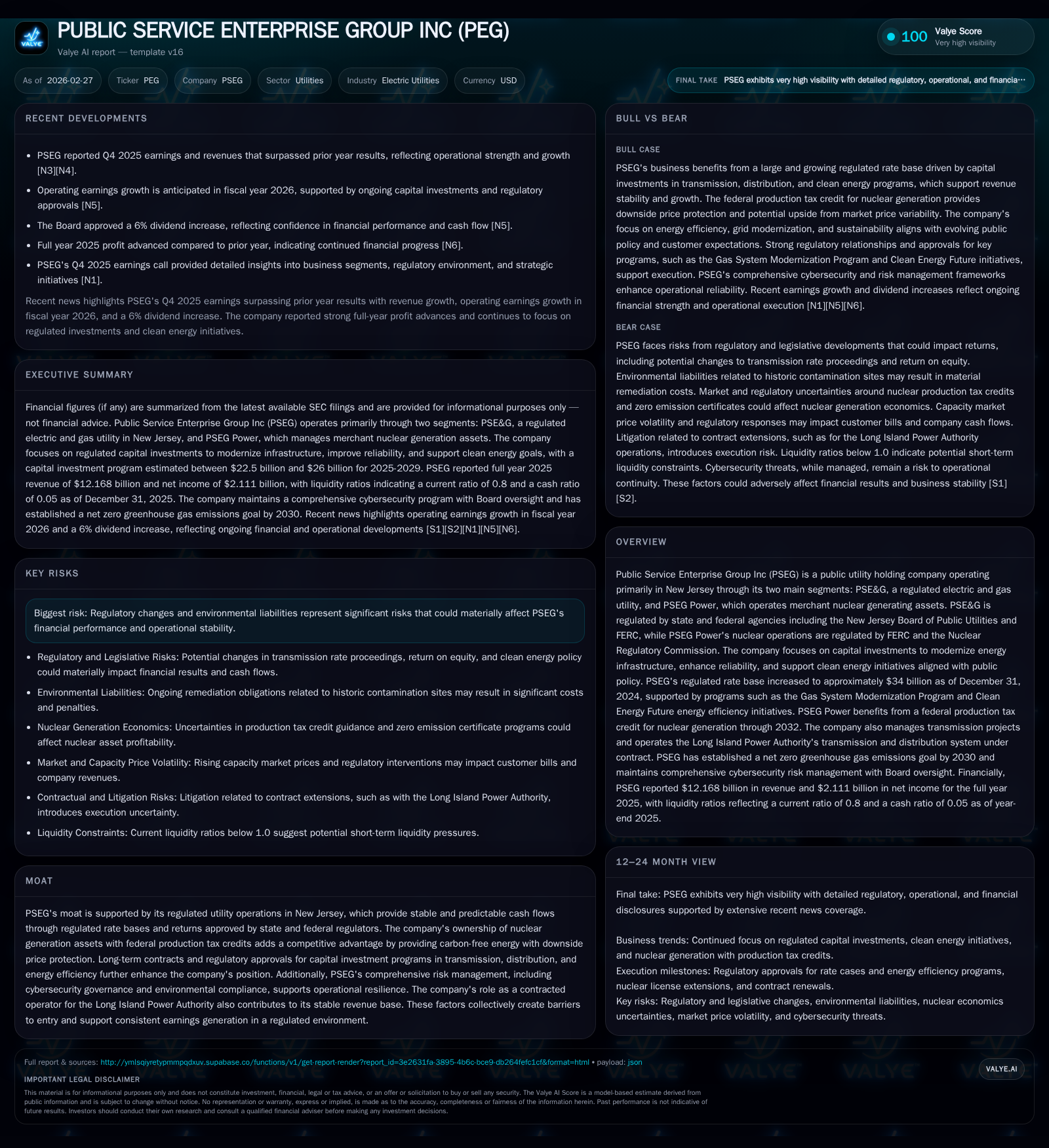

Public Service Enterprise Group (PSEG) combines stable, regulated utility operations in New Jersey with merchant nuclear generation assets to deliver consistent financial performance. Its rate base expanded from $34 billion at the end of 2024 to approximately $36 billion by the end of 2025, driven by focused investments in transmission, distribution, and energy efficiency programs. Despite facing regulatory uncertainties and environmental liabilities, PSEG sustains strong operating cash flow and recently raised dividends by 6%, reflecting confidence in its growth trajectory and capital allocation discipline. The company’s nuclear assets benefit from federal production tax credits through 2032, providing downside price protection amid competitive energy markets.

Company Overview

Public Service Enterprise Group Incorporated (PSEG) operates predominantly as a regulated electric and gas utility through Public Service Electric and Gas Company (PSE&G) in New Jersey and owns merchant nuclear generation assets via PSEG Power LLC. The company's dual-segment model provides steady cash flow from its regulated businesses while leveraging carbon-free nuclear energy assets supported by federal incentives.

The firm is subject to regulation primarily by the New Jersey Board of Public Utilities (NJBPU), the Federal Energy Regulatory Commission (FERC), and the Nuclear Regulatory Commission (NRC) for its nuclear operations [S1][S17][S18].

Historical Financial Performance

Over recent years, PSEG has delivered solid financial results backed by its substantial regulated rate base and nuclear portfolio. Revenue experienced significant growth between fiscal years 2023 and 2025, driven by expanded capital investments and supportive regulatory frameworks. Notably:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.2 | 2.1 | 3.3 | 3.0 | +18.3% | +19.1% |

| 2024 | 10.3 | 1.8 | 2.1 | 2.4 | -8.4% | -30.9% |

| 2023 | 11.2 | 2.6 | 3.8 | 3.7 | +14.7% | +148.6% |

| 2022 | 9.8 | 1.0 | 1.5 | 1.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 1258 | 26 | |

| 2024 | 1196 | 0 | -1247 |

| 2023 | 1137 | 0 | 481 |

| 2022 | 1079 | 500 | -1385 |

Source: SEC companyfacts cache [F1].

Despite a slight dip in capex for FY2025 compared to FY2024 (-3%), operating cash flows grew materially (+54.6%) indicating improved operational efficiency and working capital management [F1]. Dividend payments maintained a steady upward pattern reflecting strong cash generation capacity.

Drivers Behind Past Growth

Two main drivers underpinning PSEG's recent growth are:

Growth in Regulated Rate Base: Investments in transmission & distribution infrastructure along with expansions tied to New Jersey’s clean energy initiatives have substantially grown the regulated rate base from approximately $30 billion at year-end 2023 to $34 billion in late-2024 and further to about $36 billion at end-2025 [S1][S18]. This expansion underlies higher revenue recognition due to allowed returns on these invested assets.

Capital Programs: The Gas System Modernization Program (GSMP) continued to replace aging infrastructure whereas the Clean Energy Future Energy Efficiency Program (CEF-EE II), approved for ~$2.9 billion over early-2025 to mid-2027, supports deepening customer engagement on energy savings – critical for meeting state policy goals [S1][S2].

On the merchant side, PSEG Power benefits from federal Production Tax Credits which provide downside price protection through at least the end of this decade [S1].

Future Growth Prospects

Looking ahead, PSEG expects to continue investing heavily:

The regulated capital investment budget is anticipated between $22.5 billion and $25.5 billion for fiscal years ending between 2026 to 2030, implying a compound annual growth rate of about 6–7.5% in the regulated rate base during this period [S1]. The majority of these funds will support grid modernization, renewables integration, EE programs extensions beyond current authorization, and capacity additions responding to demand growth.

Potential incremental investments may arise due to emergent projects aligned with New Jersey's aggressive clean energy mandates.

The sustained federal nuclear Production Tax Credit supports a stable earnings floor from merchant power operations through at least FY2032 [S1], cushioning against wholesale power market volatility.

The company’s contract operation of Long Island Power Authority’s T&D system also contributes a predictable revenue stream.

Key Milestones/Forecasts/Guidance to Monitor

While no explicit EPS or EBITDA guidance was revealed in the latest filings or news releases around February/March 2026 earnings events [N1–N5], significant datapoints include:

- Continued timeline on the extension progress of GSMP II beyond Dec '25.

- Execution details surrounding CEF-EE II projects scheduled through approx mid-2030 factoring into overall capex programs.

- Dividend policy adherence or increments given recent quarterly hikes; latest indicative full-year dividend stands at $2.68 per share post a Q1'26 increase [N5][S8].

- Watch for updates on regulatory approvals which can materially affect capital deployment stair-step patterns.

Capital Allocation & Returns

PSEG has demonstrated disciplined capital deployment prioritizing sustaining and growth capex within its regulated business while maintaining prudent liquidity:

Dividends: Steady increases demonstrate confidence; dividend paid reached approximately $1.26 billion in FY2025 [F1]. The Board raised quarterly dividends to $0.67/share in Q1'26 representing an estimated annual yield near $2.68 per share [S8][N5].

Share Repurchases: No material open-market buybacks were reported recently; repurchases mostly target share delivery under employee compensation plans (~850k shares last quarter of '25) [S10].

Capital Expenditures: Around $3.27 billion spent on capex in FY2025 primarily directed toward electricity/gas T&D systems reliability and modernization along with EE projects [F1][S16].

Operating Cash Flow: CFO grew impressively (+54%) reaching almost $3.3 billion last fiscal year despite heavy capex needs evidencing robust cash conversion capabilities [F1].

Liquidity & Debt: PSEG manages liquidity via revolving credit lines totaling nearly $3.8 billion across corporate entities with available liquidity exceeding short-term usage substantially as of end Q3'25 [S4][S15]. Credit ratings remain stable BBB/Baa2 level which supports cost-effective external financing access.

The approximate return on equity computed from trailing net income over historical equity figures stands near 16%, underscoring reasonable profitability relative to invested capital levels given utility sector norms [F1].

Operational & Strategic Risk Factors

Significant aspects impacting PSEG’s outlook include:

Regulatory Environment: Changes by state regulators like NJ Board or federal policies can alter allowed returns or program approvals affecting earnings visibility [S25]. Regulatory risk remains heightened given evolving clean energy mandates and infrastructure debates.

Environmental Liabilities: As a utility with gas operations and legacy environmental exposure plus obligations related to nuclear decommissioning/resolutions, potential liabilities add complexity [S25].

Cybersecurity & Physical Security: The safeguarding of critical electric grid infrastructure remains paramount; PSEG deploys extensive multi-layered cyber defenses including third-party vendor risk assessments, AI-assisted threat detection protocols, mandatory training regimes for personnel access provisioning, plus coordination with governmental agencies [S1]. This comprehensive risk management fosters resilience against increasingly sophisticated cyber threats.

Sector Context Analysis (Non-company Specific)

In regulated utilities covering dense urban/suburban territories like New Jersey’s service area, companies must balance growth capital injections required for aging asset replacements against rate case cycles often lagging inflation pressure on costs; success lies in demonstrating superior reliability metrics combined with constructive regulatory relationships that ensure allowed returns permit sustainable ROE targets typically north of low double digits.

In parallel, ownership of merchant nuclear plants provides a wedge exposure to wholesale market dynamics but benefits heavily when paired with long-dated federal incentives like production tax credits that act as quasi-subsidies reducing downside revenue risks for baseload carbon-free generation assets — critical under accelerating decarbonization agendas.

Technological transformations including digitization deployments across smart meters, grid sensors, and customer billing platforms are essential for regulatory compliance with new energy efficiency directives but entail upfront investments whose returns sometimes only materialize over multiple future regulatory review periods.

Conclusion Summary Notes

PSEG presents a well-diversified public utility holding structure anchored by its large regulated footprint in New Jersey coupled with nuclear power generation assets benefitting from governmental incentives supporting carbon-free energy output. Its recent financials show strong revenue growth fueled mainly by strategic capital campaigns growing its rate base almost continually over successive years while preserving operating cash adequacy amid large ongoing expenditures. Dividends have risen steadily supported by improving earnings trends although share repurchases remain negligible beyond employee award-related transactions thus far recently. Continuing risk premised largely on regulatory shifts especially affecting investment recovery parameters plus environmental legacy deserves close attention alongside robust cybersecurity vigilance essentials for system integrity preservation. Future growth appears bounded but steady within publicly stated investment frameworks promising moderate compounding due largely to expansion of existing utility infrastructure refurbishment programs married with opportunities arising out of state-led clean energy policies. Monitoring upcoming regulatory filings regarding extensions or expansions of core programs GSMP II / CEF EE II will be pivotal surveillance points informing revised outlook projections.

This analysis summarizes information drawn exclusively from disclosed SEC filings including Forms10-K/10-Q/8-K up-to February28th,2026 plus mentioned news transcripts without speculative inference or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments