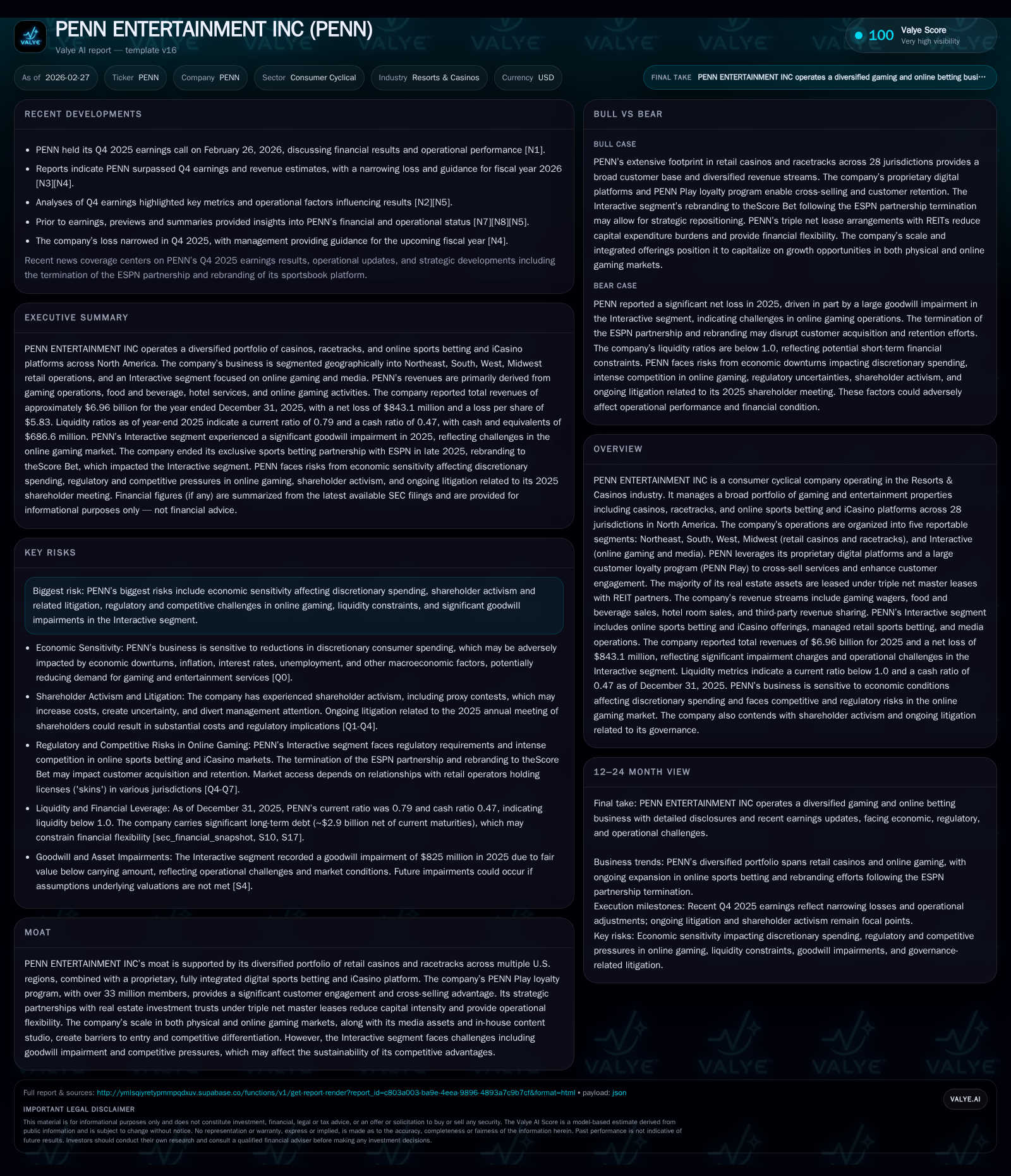

PENN Entertainment’s Impairment Challenges and Digital Pivot Pressure Returns Profitability Drag

PENN’s 2025 results reveal goodwill impairments in Interactive segment offsetting retail resilience amid evolving gaming landscape.

PENN Entertainment reported a significant net loss of $843 million in FY2025, driven largely by an $825 million goodwill impairment in its Interactive segment. While overall revenue remained broadly stable year-over-year at approximately $6.36 billion, operating income swung to a loss after prior profits, reflecting pressures from both economic sensitivity and competitive digital shifts. Capital allocation prioritized substantial share repurchases even amidst rising debt concentrations and a constrained liquidity position. Key risks include ongoing goodwill valuation uncertainty and regulatory headwinds in the burgeoning online gaming market.

Overview

PENN Entertainment Inc operates primarily as a diversified operator within the North American Resorts & Casinos industry encompassing both physical retail casinos and digital interactive gaming platforms. Its business model spans five reportable segments—Northeast, South, West, Midwest (all retail casinos and racetracks), and Interactive (online sports betting and iCasino)—with significant cross-selling synergy driven by their PENN Play loyalty program boasting over 33 million members [S1][S10][S22].

Strategically, PENN maintains its real estate largely through triple net master leases primarily with major REITs such as Gaming and Leisure Properties Inc (GLPI), reducing upfront capital needs though increasing rent-related expenses [S1][S11][S23]. This arrangement enables operational flexibility but anchors fixed costs.

Historical Performance: Revenue and Profit Trajectory

PENN's revenue demonstrated remarkable stability through recent years, progressing from roughly $3.58 billion in 2020 to over $6.36 billion by 2023 [F1]. The latest available full-year figures show slight declines:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -843 | 508 | -674 | -170.7% | ||

| 2024 | -311 | 359 | 73 | +36.4% | ||

| 2023 | 6.4 | -490 | 456 | -690 | -0.6% | -320.6% |

| 2022 | 6.4 | 222 | 878 | 974 | +8.4% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 354 | -46.0 |

| 2024 | 0 | -10.9 |

| 2023 | 150 | -15.3 |

| 2022 | 601 | 6.2 |

Source: SEC companyfacts cache [F1].

Note: Complete FY revenue figures for years after 2023 are not published yet; operating income, net income, CFO, capex, and buybacks are cited from [F1].

Revenue progression exhibits slight compression since FY22 (-0.6%), while operating income has experienced dramatic volatility—swinging from nearly a billion-dollar profit in FY22 to significant losses thereafter. This volatility stems mainly from sizable non-cash write-downs related to goodwill impairments within the Interactive segment.

Goodwill Impairment in Interactive Segment

A highlight—and concern—in PENN’s FY25 financials is an $825 million goodwill impairment recorded against their Interactive reporting unit which held roughly $775 million of goodwill at year-end ([S1]). Management employed complex valuation approaches incorporating discounted cash flow projections alongside peer EBITDA multiples in evaluating fair value.

The impairment reflects pressures including intense competition in the online sports betting/iCasino space, regulatory uncertainties across states/provinces, elevated operational costs tied to technology development and marketing expenses (evidenced partly by multiyear ESPN Sportsbook agreement costs), as well as weaker-than-expected revenue growth assumptions [S1][S14][S25].

Sensitivity analyses disclosed that a mere 10% decline in forecasted revenues or EBITDA for this segment could trigger additional impairments exceeding $100 million. This underscores the fragility of expected future cash flows amid a shifting regulatory environment.

Retail Operations Stability and Segmental Contributions

Outside Interactive, PENN's core retail segments remain the backbone of revenue generation and cash flows:

- Northeast: Largest contributor with about $2.77 billion revenue in latest figures.

- South: Strong regional presence with revenues north of $1 billion.

- West: Modest but steady contributions around mid-hundreds of millions.

- Midwest: Similar scale to West with roughly $1.18 billion [S10].

These geographic clusters consist primarily of casino operations augmented by racetracks, food & beverage services, hotel accommodations, and affiliated amenities [S1]. The company has a broad footprint across more than two dozen states facilitating operational diversity that helps offset localized economic fluctuations.

PENN’s integrated PENN Play loyalty platform is pivotal for cross-promoting offerings across these retail holdings as well as feeding into interactive channels enhancing customer lifetime value [S1].

Capital Allocation and Financial Position

Although profitability is under pressure from impairments and operational costs linked to marketing agreements (e.g., ESPN-related media spends), PENN has maintained aggressive capital return policies recently:

- Share repurchases topped approximately $354 million during FY25 despite net losses recorded [F1][S6].

- The company operates within a high-leverage framework with total long-term debt surpassing $2.9 billion including revolving credit draws (~$570 million), term loans, senior unsecured notes, and convertible instruments maturing mostly between 2026–2029 [S4][S7][F1].

- Liquidity metrics indicate some strain: Current assets around $1.17 billion versus current liabilities approximately $1.48 billion reflect a sub-1x current ratio near ~0.79 [F1].

- Interest expense remains elevated (net interest expense estimated at over $400 million for FY25), pressuring net margins further [S11].

Capex commitments remain focused on project developments correlating to casino expansions or new property openings with partial REIT funding participation ($280 million received from GLPI during FY25 for development projects) [S16].

Future Growth Drivers and Industry Context (Analysis)

Looking forward, PENN’s growth opportunities center on:

- Expanding penetration in online sports betting where regulatory frameworks continue evolving favorably but competition stiffens.

- Enhancing content offerings via proprietary iCasino product studio aiming at differentiation within crowded digital markets.

- Leveraging vast loyalty data analytics via PENN Play program for targeted promotions.

- Developing real estate assets prudently under triple net leases minimizes capex pressures while allowing flexibility.

Constraints include economic cycles impacting discretionary leisure spending regionally—especially given PENN's heavy reliance on local/regional customers rather than destination resort gambling akin to Las Vegas or Atlantic City [S14][S22]. Regulatory risks around state gaming laws also persist prominently especially affecting interactive verticals [S14].

Milestones & What To Watch (Analysis)

Analysts should monitor:

- Quarterly goodwill impairment reviews for Interactive segment amid evolving market conditions.

- Ongoing EPS trajectory vis-à-vis share repurchase cadence considering liquidity constraints.

- Changes or renewals regarding key marketing/media contracts affecting cost structures.

- Progress on project capital execution balanced against debt maintenance requirements under amended credit agreements.

- Regulatory developments shaping multi-jurisdictional availability for online betting platforms.

Conclusion

PENN Entertainment stands at an inflection marked by its hybrid business model combining traditional brick-and-mortar casinos with emerging digital interactive platforms. While retail operations deliver foundational cash flows stabilizing top-line revenue near previous peaks, profitability is hampered severely by impairment charges stemming from the challenging outlook for its Interactive segment.

Capital allocation shows management commitment to shareholders via buybacks despite profit headwinds but must be balanced carefully against mounting leverage and liquidity squeeze risks moving forward. The expansive footprint across North America coupled with proprietary technology assets present meaningful opportunities if regulatory trends sustainably support growth without further material asset impairments.

Continued vigilance around economic sensitivities, evolving competitor dynamics especially digitally native operators, and regulatory frameworks will be essential for gauging PENN’s financial trajectory going into mid-decade.

This analysis is based exclusively on publicly available information up to February 27, 2026, including SEC filings and recent earnings disclosures from PENN Entertainment Inc. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments