Progressive Corp’s Growth Engine Accelerates: Data-Driven Pricing and Capital Strategy in Focus

Progressive’s sharp underwriting and capital deployment have fueled robust top-line and earnings growth, while navigating complex risks in a competitive insurance landscape.

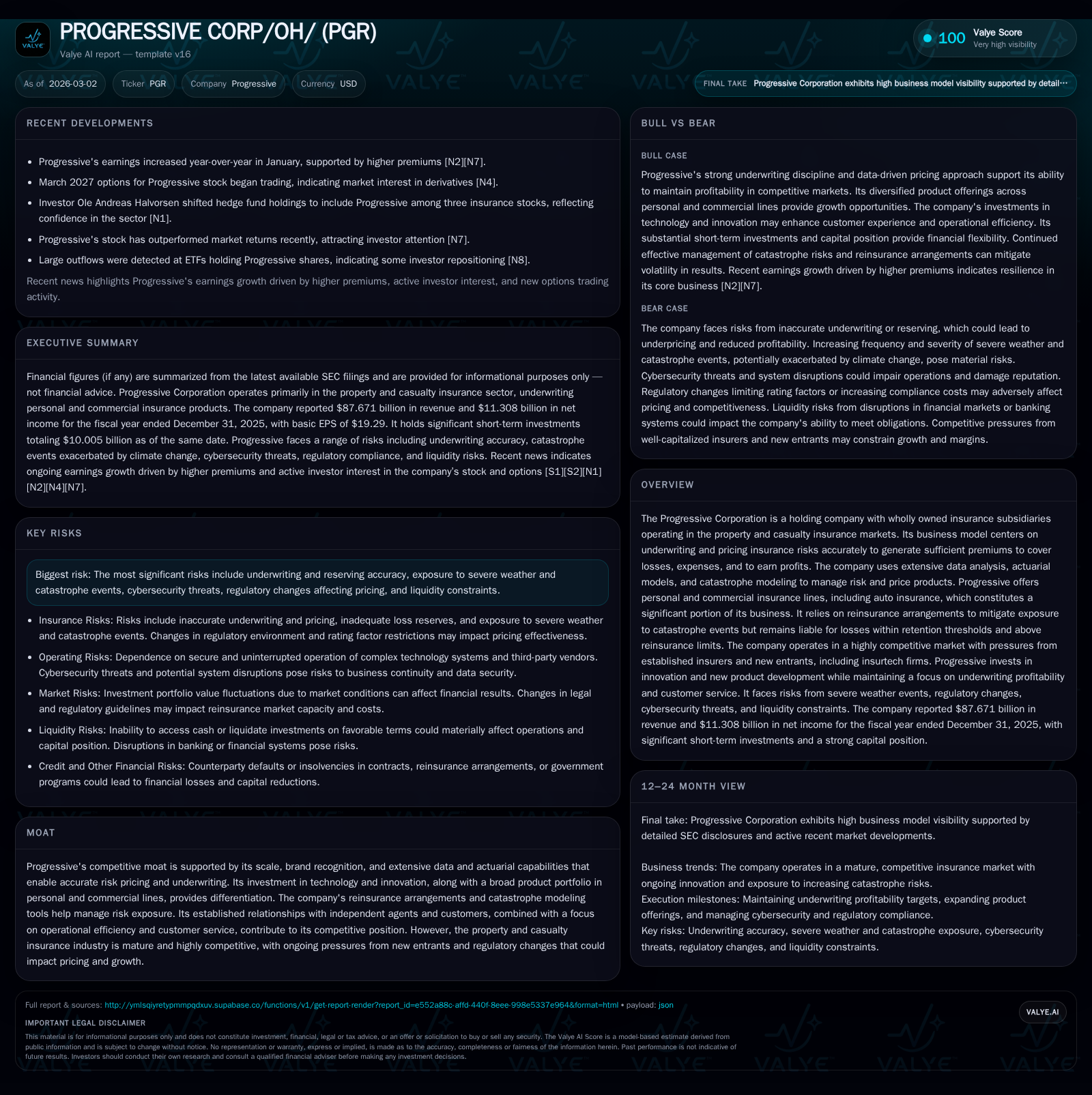

The Progressive Corporation has demonstrated a strong growth trajectory driven by precise actuarial models, innovative technology integration, and disciplined underwriting. For fiscal year 2025, revenues expanded 16.3% to $87.7 billion, with net income surging 33.3% to $11.3 billion, supported by underwriting profitability and operating efficiencies. The company’s competitive moat is anchored by scale, brand recognition, and advanced data analytics capabilities that underpin pricing power in a mature, highly contested property-casualty insurance market. Residual risks from catastrophe events, cybersecurity, and regulatory shifts remain significant challenges. Progressive’s capital allocation reflects aggressive share repurchases aligned with equity compensation needs and retains substantial cash flow for reinvestment. Looking ahead, growth prospects exist but are moderated by evolving competition from insurtech entrants and market cyclical dynamics.

Revenue and Earnings Surge Driven by Sophisticated Underwriting

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 87.7 | 11.3 | 17.5 | 348 | +16.3% | +33.3% |

| 2024 | 75.4 | 8.5 | 15.1 | 285 | +21.4% | +117.3% |

| 2023 | 62.1 | 3.9 | 10.6 | 252 | +25.2% | +440.9% |

| 2022 | 49.6 | 0.7 | 6.8 | 292 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($bn) | ROE% |

|---|---|---|

| 2025 | 17.2 | 37.3 |

| 2024 | 14.8 | 33.1 |

| 2023 | 10.4 | 19.2 |

| 2022 | 6.6 | 4.5 |

Source: SEC companyfacts cache [F1].

Progressive has sustained accelerated growth propelled by its data-centric underwriting philosophy. In the fiscal year ending December 31, 2025, Progressive reported revenues of approximately $87.67 billion, marking a 16.3% increase from $75.37 billion reported in 2024 [F1]. This surge is largely attributed to finely tuned pricing models that harness extensive historical claims data combined with forward-looking estimates of accident frequency and severity.

Net income displayed even more pronounced expansion, rising 33.3% year-over-year to $11.31 billion up from $8.48 billion in the prior year period [F1]. Such a gain underscores Progressive’s ability not only to grow premiums but also to maintain rigorous control over loss adjustment expenses and overall underwriting expense ratios.

Operating cash flow correspondingly grew by 16.1% to nearly $17.55 billion as the company harnessed underlying portfolio strength alongside disciplined claim payments and expense controls [F1]. Capital expenditure remained modest relative to operations at $348 million but rose by over 22%, reflecting ongoing investments in technology infrastructure critical to refining pricing precision and customer experience.

This financial momentum reflects Progressive’s disciplined adherence to an underwriting profitability target around a combined ratio of approximately 96 — balancing growth ambitions against loss cost realities highlighted explicitly in their filings as a core objective [S4]. The firm’s actuarial rigor ensures premiums appropriately reflect risk exposures while accounting for inflationary pressures on claim settlements.

Dissecting Progressive’s Competitive Moat: Scale, Technology, and Pricing Power

The company leverages its competitive moat through multiple dimensions: scale economies that reduce per-unit acquisition costs; expansive brand recognition supported by decades-long market presence; advanced analytic capabilities that enable granular segmentation of insured pools; and integrated catastrophe modeling that informs reinsurance strategies [S8],[S24].

Such capabilities afford Progressive an edge in controlling its combined ratio — a key performance metric encompassing loss costs plus expenses relative to earned premiums — thereby allowing selective rate adjustments even within highly regulated jurisdictions where insurers face pricing constraints.

Customer distribution is diversified across direct-to-consumer channels as well as a strong independent agent network specializing in personal auto policies—the largest revenue component—as well as commercial lines which carry greater growth potential but complexity due to diverse risk profiles like trucking fleets or ridesharing operations impacted specifically by evolving transportation technologies [S24].

In an increasingly digital marketplace challenged by insurtech entrants deploying AI-enabled underwriting platforms or alternative risk assessments via telematics data aggregation, Progressive maintains competitive defense through long-established actuarial databases combined with continuous investments in IT systems that support customer segmentation and claims automation.

Navigating Emerging Challenges: Catastrophe Risks, Cybersecurity, and Regulatory Scrutiny

Progressive's exposure to severe weather events remains a prominent risk vector especially when catastrophe losses exceed reinsurance protection layers resulting in retention-driven impact on earnings volatility [S1], [S4]. To mitigate this threat, the company continuously refines its catastrophe modeling incorporating climate science advances that underpin strategic reinsurance placement ensuring layered coverage at economically feasible terms.

Cybersecurity represents an operational risk given Progressive’s reliance on technology platforms housing sensitive customer data including personal identifiers and proprietary models critical for competitive positioning [S17]. The company discloses comprehensive multi-tier controls but acknowledges the evolving threat landscape necessitates ongoing investment.

Regulatory complexity compounds these challenges as Progressive operates under the oversight of multiple state insurance regulators each imposing specific caps on rate changes or requiring prior approval processes which can limit responsiveness during market cycles or sudden shifts in claims cost structures [S4], [S10]. Federal regulations concerning use of artificial intelligence in underwriting or marketing further compound compliance burdens requiring agile legal counsel integration into product deployment decisions.

Capital Allocation: A Closer Look at Share Repurchases, Dividends, and Return on Equity

Capital stewardship remains tightly aligned with operational success metrics consistent with shareholder interests yet cautious preservation for reinvestment.

With equity expanding from ~$25.6 billion in FY2024 to ~$30.3 billion for FY2025—an increase supporting organic growth—the company achieved an approximate return on equity (ROE) of 37.3%, signaling high efficiency in translating equity base into net income generation [F1].

Free cash flow (operating cash flow minus capex) approximated $17.2 billion for FY2025 reflecting strong liquidity allowing flexibility in capital deployment strategies [F1].

Progressive aggressively pursues dilution-neutral share repurchase programs aimed primarily at offsetting issuance related to equity-based employee compensation plans as approved by the board with authorization for up to 25 million shares without expiration date reported for mid-2025 onward activity; these buybacks complement historically minimal dividend pay-outs demonstrating preference for internal capital recycling over yield distribution given growth priorities and capital adequacy considerations [F1], [S6], [S22].

Future Outlook: Growth Prospects Balanced Against Market Saturation and Competitive Dynamics

Looking forward, the company continues initiatives focused on premium rate adequacy enhancements through incremental actuarial model refinements paired with product innovation targeting both personal auto segments (including usage-based insurance offerings) and expanding commercial lines where margin potential remains attractive albeit volatile due to exposure heterogeneity such as heavy trucking versus emerging mobility service coverages.

Insurers traditionally face cyclicality characterized by "hard" markets with elevated rate levels followed by "soft" periods marked by aggressive price competition eroding returns—a cycle Progressive manages actively maintaining near-target combined ratios even during soft phases via underwriting discipline and operational efficiency gains noted across reports [N1],[N13].

Competitive pressure from nimble insurtechs leveraging new data streams such as IoT sensor feeds or AI-driven claims automation remains an evolving threat necessitating vigilant adaptation efforts including partnership explorations or targeted acquisitions although execution risks remain inherent for any expansion beyond core competencies as acknowledged internally within risk disclosures related to new product developments outside traditional lines [S4], [S24].

Key Performance Indicators to Watch Ahead

Monitoring combined ratio trends remains paramount as fluctuations can signal shifts in underlying loss experience or expense management effectiveness directly affecting underwriting margins vital for sustainable profitability.

Tracking premium yield changes against inflationary cost pressures offers early insights into pricing power retention versus competitive discounting across diverse markets.

Catastrophe loss frequencies/severities provide leading signals regarding adequacy of reinsurance structures particularly when correlated with emerging climate pattern disruptions.

Finally technological adoption rates measured through digital quote penetration or claims cycle times highlight operational improvements influencing customer retention metrics crucial amid tightening marketplace competition.

Industry-Specific Risk Management: Reinsurance Strategies and Loss Reserving Practices

Progressive employs layered reinsurance arrangements sized carefully according to modeled catastrophe exposures consistent with internal risk appetite frameworks balancing retention limits against premium cost optimization thereby stabilizing earnings against large-scale loss events exceeding primary policyholder risk pools [S1], [S4].

Reserve adequacy undergoes rigorous actuarial evaluation incorporating stochastic modeling techniques integrating development patterns from historical claim payments enabling precision estimates minimizing reserve deficiency surprises that have posed existential threats historically within property-casualty insurers.

Transparency around reserving methodologies serves both regulatory reporting compliance needs across jurisdictions imposing diverse requirements as well as investor relations functions seeking clear articulation of underlying assumptions impacting future earnings realizations.

Disclaimer: This report is based solely on publicly available information provided through SEC filings and verified news sources as of March 2026. It is intended solely for informational purposes without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments