Pony Group Inc. Confronts Liquidity and Margin Pressure in Niche Travel Services

Latest 10-Q reveals acute liquidity stress and declining margins amid recurring losses in Pony Group's cross-border car service operations.

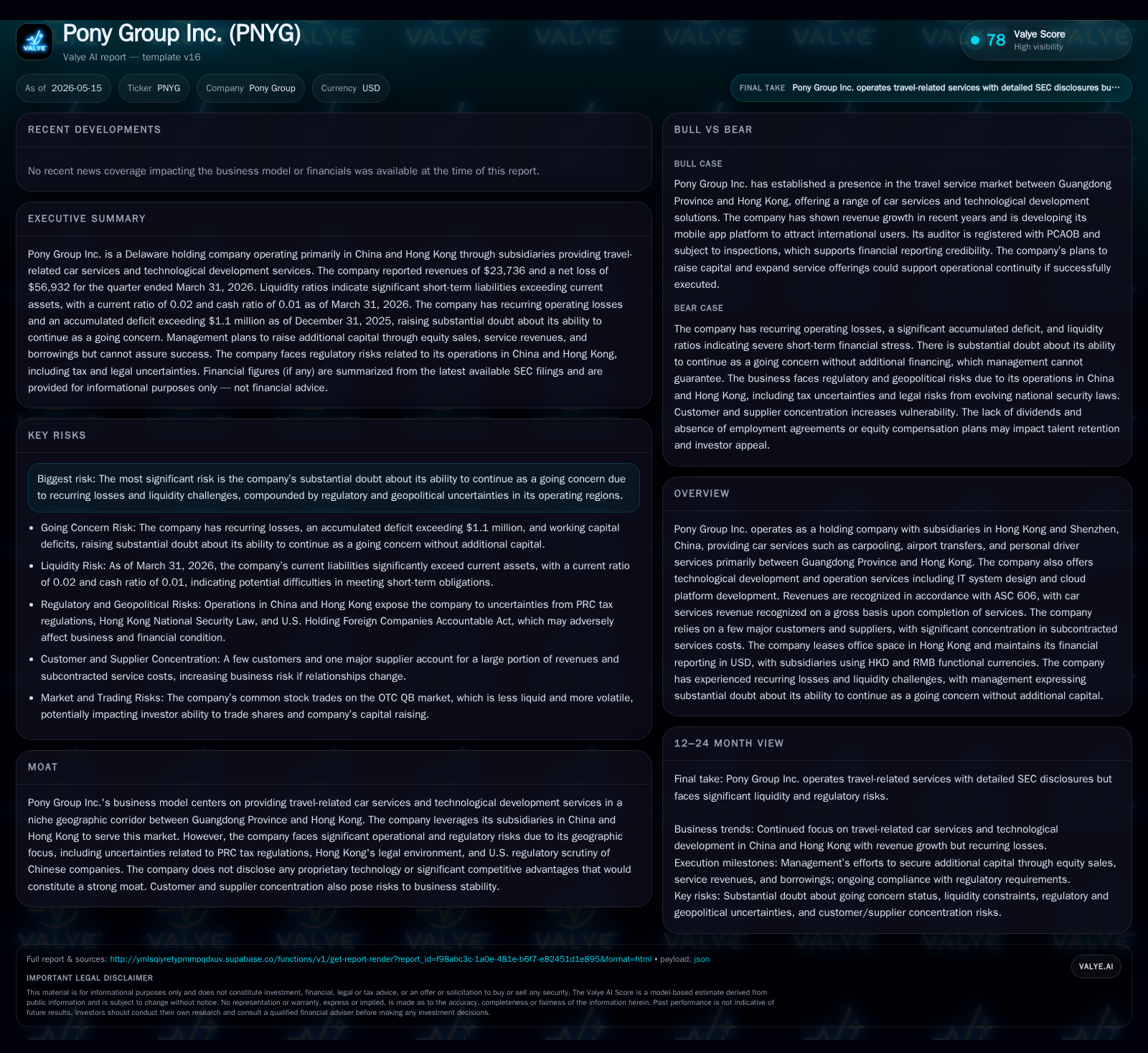

Pony Group Inc., operating primarily carpooling and personal driver services between Guangdong Province and Hong Kong, disclosed worsening liquidity and compressed gross margins in its latest quarterly filing. Despite a modest top-line increase from new clients in 2025, the company faces substantial going concern doubts due to a working capital deficit exceeding $1 million and relentless net losses. Concentration risks with key customers and suppliers intensify operational fragility, while regulatory complexities between China and Hong Kong add uncertainty. Growth prospects hinge on expanding app-based travel solutions for international users, yet financial headwinds and regulatory risks constrain near-term outlook.

Latest Quarterly Operating Update: Signals of Strain

In its most recent 10-Q filed May 15, 2026, Pony Group Inc. paints a stark picture of heightened financial stress. The company reports a current ratio of just 0.02 as of March 31, 2026, with current liabilities exceeding $1 million versus current assets under $16 thousand [F1][S2]. This severe working capital imbalance exacerbates longstanding liquidity challenges previously flagged in the annual report. Net cash burn through operating activities remains substantial, underscoring ongoing negative operational cash flow dynamics.

Revenues for full year 2025 increased to $141,393 from $97,394 in 2024, largely attributable to onboarding a significant new client—Benfu Development Ltd.—accounting for over $55K of car services revenue [S1]. Yet this top-line growth failed to translate into improved profitability; gross margins fell precipitously from 43% in 2024 to 33% in 2025 as Pony adopted aggressive price concessions to secure market share amid intense competition [S1]. Operating expenses soared by over 40%, propelled by accrued but unpaid consulting fees that further pressured earnings.

Business Model and Service Offerings: The Cross-Border Car Service Niche

Pony Group operates primarily as a holding company with subsidiaries based in Hong Kong and Shenzhen focused on providing transportation solutions between Guangdong Province and Hong Kong [S1]. Its core service lines include carpooling, airport transfers, and personalized driver engagements aimed at both individual travelers and groups.

Revenue derives chiefly from these car service contracts recognized on a gross basis upon service completion per ASC 606 standards. The company functions largely as an intermediary: it aligns travelers with drivers via agreements with third-party car fleet operators who provide the actual transport capacity [S1]. This subcontractor-dependent model means that costs are closely tied to service volume but offer limited pricing leverage. Cost of revenue scales approximately with sales volume but has risen faster than revenues recently due mainly to subcontractor cost increases.

Beyond transport services, Pony develops travel-related IT systems including multi-language mobile apps tailored for foreign visitors seeking one-stop travel booking encompassing car rental, hotel reservations, tickets, and English-speaking drivers. This technology segment aims at differentiating the user experience within its geographical corridor but remains nascent relative to overall revenues.

Customer concentration is pronounced: Benfu Development emerged as a dominant client contributing roughly 39% of annual revenue in 2025 [S1], presenting risk should this relationship falter or terms deteriorate.

Competitive Positioning and Industry Structure in Guangdong-Hong Kong Corridor

The geographic focus confines Pony’s market scope principally to the Guangdong-Hong Kong corridor—a region marked by fragmented transportation providers where numerous small-scale operators compete intensely on price.

Pony’s dependency on a concentrated pool of subcontracted vehicle providers introduces supplier-side concentration risks. Subcontracted services represent a majority share of direct costs for car services, limiting margin expansion potential unless Pony can negotiate more favorable rates or improve operational efficiencies [S8].

The lack of any disclosed proprietary technology or patents implies there are minimal barriers preventing new entrants from offering comparable services or replicating Pony's booking platform enhancements. Furthermore, limited customer switching costs further restrict pricing power across this fragmented peer group.

Regulatory complexity adds another layer of challenge. Cross-border operations must navigate PRC enterprise income tax statutes addressing indirect asset transfers (Bulletin 7), Hong Kong local regulations governing transportation licensing and contract enforcement, plus evolving U.S. regulatory scrutiny—specifically concerning audit inspections mandated by the Holding Foreign Companies Accountable Act (HFCAA) which could affect listing status if audit access gaps persist [S1][S8][S25]. These factors inject uncertainty around compliance costs, potential penalties, or operational restrictions which could impact growth trajectories.

Growth Drivers: Opportunities and Limitations

Pony aims to leverage its mobile app—"Lets Go App"—to expand beyond localized transport by becoming a broader travel service platform catering especially to international tourists drawn to China’s Guangdong region [S1]. The app offers multi-lingual interfaces (Chinese/English) with planned enhancements such as PayPal integration for seamless payments.

Potential growth vectors include:

- Scaling user acquisition outside China through digital marketing targeting inbound leisure/business travelers.

- Forming strategic partnerships with capital-rich marketing entities or technology providers capable of accelerating reach and product breadth.

- Expanding ancillary travel bookings (hotels, tickets) alongside existing car rental/driver services to create integrated offerings enhancing user retention.

However, these ambitions face hurdles linked not only to operating losses limiting reinvestment but also high customer/supplier concentration capping achievable volume gains without diversification. Product development timelines coupled with required talent recruitment increase execution risk. Gross margin deterioration due to aggressive pricing erodes financial flexibility needed for sustained innovation.

Risks and Watchpoints: Operational, Regulatory, and Financial Vulnerabilities

The overriding risk evident from filings is Pony’s precarious financial footing characterized by persistent losses ($246K net loss in FY2025) driving an accumulated deficit exceeding $1.13 million alongside a substantial working capital gap placing existential stress on continuity absent successful capital infusion [S2][F1].

Operationally, heavy reliance on one major client heightens counterparty risk; loss or renegotiation could cause dramatic revenue swings. Supplier concentration magnifies vulnerability should subcontractors alter pricing or availability adversely affecting delivery capability.

From a regulatory standpoint:

- PRC tax rules (notably Bulletin 7) concerning indirect asset transfer taxation introduce exposure if corporate structures or transactions are challenged post hoc.

- HFCAA-driven audit inspection requirements necessitate transparent access for PCAOB review; any impediment risks delisting jeopardizing investor confidence and capital markets access.

- Hong Kong legal nuances surrounding contractual enforceability for transportation operators add jurisdictional complexity affecting operational stability.

Finally, management concedes that raising additional financing—whether equity issuances dilutive to shareholders or debt incurring restrictive covenants—is critical but uncertain given market conditions and historical financial performance [S4][S5]. Failure here would imperil Pony's capacity even to fund daily operations let alone execute growth strategies.

What to Watch Next: Funding, Operational Trajectory, and Market Penetration

Key upcoming milestones likely influencing Pony’s near-term outlook include:

- Quarterly operating results indicating whether margin compression stabilizes or reverses amidst customer mix shifts or revised pricing policies.

- Progress (or failure) in raising incremental liquidity via equity sales or bank borrowings which management views as necessary for survival [S2][S4].

- Expansion metrics from Lets Go App adoption rates internationally reflecting success penetrating non-Chinese traveler segments vital for scaling beyond commodity transportation offerings.

- Announcements regarding strategic partnerships that can supply technology resources or marketing muscle improving distribution reach are material catalysts—or absence thereof signals stalled growth potential.

- Regulatory developments affecting audit clarity under HFCAA inspections that could reduce compliance uncertainties enhancing investor sentiment.

These watchpoints together map out critical inflection points around operational viability versus impending structural constraints impacting continuity decisions.

Financial Snapshot: Liquidity Challenges and Balance Sheet Pressure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $8050 | |

| 2026-03-31 | ||

| Current assets | $15593 | |

| 2026-03-31 | ||

| Current liabilities | $1031537 | |

| 2026-03-31 | ||

| Current ratio | 0.02x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot underscores the dire liquidity state despite incremental revenue growth. Net losses sustained over consecutive periods cumulatively erode shareholder equity impeding organic fund generation.[F1]

This analysis reflects information publicly disclosed up through Pony Group Inc.'s latest filings without extrapolation beyond reported data points. It does not constitute investment advice but serves as an industry-focused evaluation highlighting critical operational dynamics amid continuing financial distress within niche cross-border car services concentrated in the Guangdong-Hong Kong corridor.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments