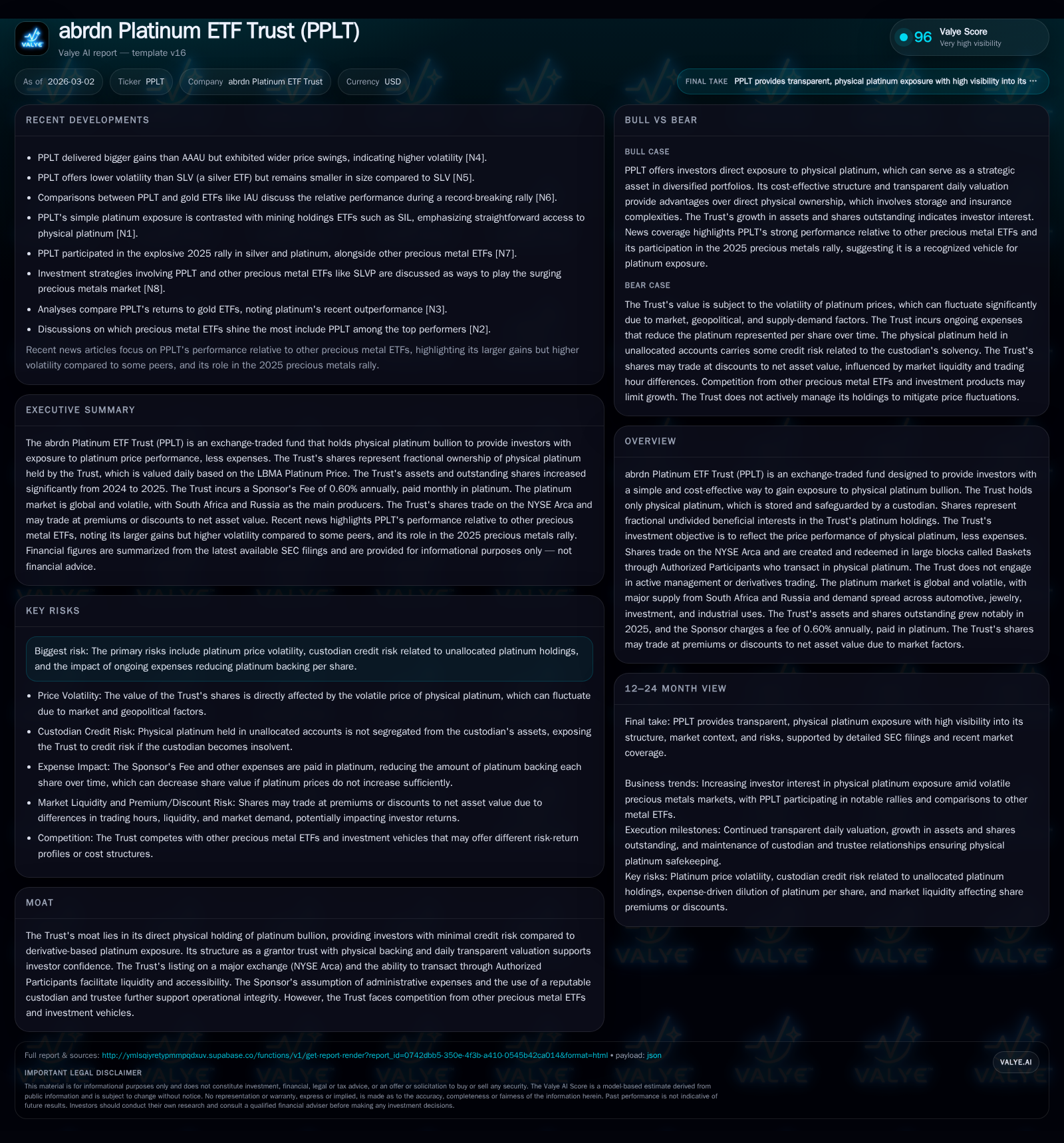

abrdn Platinum ETF Trust’s Resurgence and Price-Linked Dynamics in 2025

A detailed review of how abrdn Platinum ETF Trust’s physical platinum holdings and volatile commodity prices sparked a significant financial rebound in 2025.

abrdn Platinum ETF Trust (PPLT) experienced a sharp turnaround in net income in FY2025, propelled by rising platinum prices and increased share issuance. The Trust's structure as a grantor trust holding physical platinum bullion shields investors from derivative market credit risks, while its liquidity is supported by Authorized Participants transacting physical platinum Baskets. Despite operational integrity backed by Premier custodians and controlled expenses, risks remain around custodian liabilities, regulatory environments, and expense-induced value erosion. Investors should monitor ongoing platinum price volatility, basket creation/redemption trends, and potential regulatory shifts to gauge the Trust’s trajectory.

From Losses to Profit: Tracking PPLT’s Financial Turnaround

abrdn Platinum ETF Trust (PPLT) emerged from consecutive years of losses in FY2023 (-$32.8 million) and FY2024 (-$94.7 million) to an impressive profitability milestone in FY2025 with net income reaching approximately $1.34 billion [F1]. This extraordinary net income growth of roughly 1517% year-over-year corresponds to a valuation rebound propelled primarily by the increase in the underlying physical platinum prices held directly by the Trust.

Simultaneously, equity expanded nearly threefold from about $1.02 billion at end-2024 to roughly $2.86 billion at end-2025, reflecting heightened investor inflows and subsequent issuance of shares [F1][S1]. Outstanding shares rose from 12.2 million to 15.55 million during this period, consistent with expanded assets under custody. The increase in share count aligns closely with higher platinum bullion inflows facilitated through basket creations by Authorized Participants.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 1342 | +1517.0% |

| 2024 | -95 | -188.6% |

| 2023 | -33 | -151.7% |

| 2022 | 63 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 46.9 |

| 2024 | -9.3 |

| 2023 | -3.3 |

| 2022 | 5.8 |

Source: SEC companyfacts cache [F1].

Note: Share count data available only for FY2024-FY2025.

This dramatic turnaround underscores the sensitivity of the Trust's performance to platinum price movements rather than operating leverage or traditional earnings mechanics.

Platinum Price Swings and Their Impact on PPLT’s Share Value

The valuation of PPLT shares depends almost exclusively on spot prices of physical platinum bullion held by the Trust [S1][S7]. Major producers such as South Africa and Russia dominate global supply chains; any disruptions or policy shifts in these regions reverberate through prices given their outsized market share [S1]. Demand drivers encompass diverse sectors including autocatalysts for vehicles (a crucial source amid tightening emissions standards), jewelry manufacture reflecting cyclical consumer tastes, industrial applications including electronics, and investment demand responding to inflationary expectations.

Investor behavior notably shapes volatility: hedge funds’ trading strategies can accentuate swings via speculative positioning while producer hedging activities sometimes exert downward pressure when futures contracts are sold aggressively [S1]. Additionally, currency fluctuations (notably U.S. Dollar strength), macro interest rate changes affecting opportunity costs of holding precious metals versus yield-bearing securities contribute to short-term fluctuations [S7]. Recently documented online campaigns targeting precious metal investments demonstrate how public sentiment can transiently elevate or depress prices [S1].

Such volatility not only affects underlying NAV but also creates opportunities for premiums or discounts relative to NAV on PPLT trading due to timing differences between NYSE Arca trading hours and global platinum markets closing times outside U.S. daylight hours [S20].

Trust Structure and Moat: Physical Bullion vs Derivative Competitors

PPLT operates as a grantor trust exclusively backed by physical platinum bullion stored under stringent custodial arrangements with ICBC Standard Bank Plc [S1][N1]. This direct holding model differentiates the Trust from competing ETFs that gain exposure via derivatives or futures contracts subject to counterparty credit risk—a material risk given recent derivative market disruptions elsewhere.

The Trustee (The Bank of New York Mellon) maintains fiduciary responsibility for asset safekeeping and accurate valuation based on the LBMA Platinum Price PM benchmark pricing framework [S9][S21]. Investors benefit from transparent daily net asset value reporting tied closely to spot metal prices.

However, not all holdings are fully allocated; small amounts temporarily reside in unallocated accounts for processing baskets trades which introduces nominal credit exposure to the Custodian governed under English law—historically challenging for U.S.-based enforcement if losses occur [S8]. Despite this structural limitation, the operational integrity is fortified by use of reputable custodians endorsed by LPPM standards with insurance maintained over business operations though not directly covering platinum losses [S12].

Authorized Participants and Liquidity Mechanics Behind Shares Movement

Liquidity within PPLT shares is principally enabled via Authorized Participants who create or redeem large blocks called Baskets (each Basket representing 50,000 shares) by physically delivering or receiving equivalent ounces of platinum bullion [S9]. This mechanism ensures tight coupling between share issuance/redemption volumes and underlying metal holdings.

Authorized Participants must be registered broker-dealers or financial institutions with access to both physical platinum markets and futures hedging facilities allowing efficient arbitrage that keeps trading prices near NAV [S24]. Transaction fees apply on creations/redemptions which influence short-term pricing dynamics but generally promote liquidity.

The continuous issuance or redemption flows driven by investor demand modulate trust equity size over time—explaining movements seen between FY2024 and FY2025 alongside price effects [F1][S23]. Nevertheless, residual premiums/discounts do emerge occasionally due to timing mismatches between NYSE Arca trading close and London/Zurich precious metals markets closure.

Risks Linked to Custody, Regulatory Environment, and Expense Deductions

Several risk factors merit detailed attention. Notably:

Custody risk arises chiefly because unallocated account holdings are commingled within Custodian assets without segregation; legal recourse might be limited under English law if loss or theft occurs since liability is capped often only to direct negligence or fraud consequences [S8][S12][S14]. Insurance coverage does not extend explicitly to the Trust's platinum nor require sub-custodians to maintain coverage.

Regulatory oversight includes dual frameworks: The UK Financial Conduct Authority governs aspects related to financial market participants in London-based wholesales markets while U.S. Commodity Futures Trading Commission oversees commodities futures activities indirectly relevant given the Trust's avoidance of derivatives exposure itself but participant behaviors affect underlying markets [S4][S5].

Ongoing expenses borne by the Trust include administrative fees absorbed mainly by the Sponsor but certain costs not assumed result in occasional sales of platinum impacting backing per share adversely over time [S23][S17]. Additionally, periodic Sponsor fees charged monthly in-kind reduce ounce equivalency incrementally.

Trading price deviations from NAV can widen during off-hours when major precious metals markets are closed causing potential temporary illiquidity effects disadvantaging some shareholders on disposition timing.

Capital Allocation Trends: Equity Growth Amid Zero Cash Balances

Financial statements confirm no cash or equivalents held at fiscal year ends indicating all capital is directly deployed into physical platinum inventory rather than operating cash reserves or cash equivalents—typical for grantor trusts structured solely around commodities custody without operational business assets [F1].

The absence of dividends or buyback programs reinforces that capital returns manifest mainly through appreciation in underlying metal values instead of periodic cash distributions [F1][S16][S23]. This aligns with structural design focused on maximizing asset growth rather than income generation.

Calculated approximate return on equity based on FY2025 figures is near 47%, as measured by net income divided by equity capital suggesting highly efficient deployment of shareholders’ invested capital despite no active management leverage mechanisms typical for corporate entities [F1].

Therefore, investors must view returns strictly through the lens of commodity price appreciation influencing net asset value rather than traditional corporate cash flow distributions.

What Investors Should Watch Next: Key Market and Operational Milestones

Forward-looking considerations center around:

- Continued monitoring of global geopolitical tensions affecting South African and Russian production—sanctions regimes or mining strikes could sharpen supply shocks influencing spot prices [N3][N6].

- Evolving demand trends particularly from catalytic converter regulator tightening globally boosting automotive palladium substitution back toward platinum usage potentially demanding tight inventories [N7][N8].

- Changes in Authorized Participant activity levels signaling inflows/outflows that affect shares outstanding plus any new entrants altering liquidity profiles [N2][N4].

- Regulatory updates emanating from FCA guidance on derivatives-like exposures although less applicable directly here—but shifts affecting ancillary market participants could have knock-on effects on pricing behavior [S4][S5].

- Announcement of custodian substitutions or trustee changes that may disrupt operations or introduce new counterparty risks warrant vigilance given critical roles played currently by ICBC Standard Bank Plc and BNY Mellon respectively [S28].

- Technology-driven enhancements related to pricing benchmarks as ICE Benchmark Administration assumes responsibility mid-2026 may refine transparency but also induce transitional volatility around LBMA Platinum Price benchmarks used for NAV calculations daily [S21][S22].

Analysts suggest that while PPLT offers one of the most straightforward ways for retail investors to access physical platinum price movements with minimal credit counterparty concerns compared with derivative-laden ETFs ([N1]), inherent commodity price volatility remains paramount shaping both upside opportunities and downside risk scenarios ([N4], [N5]). Institutional investors should thus maintain active attention on macro market conditions alongside operational disclosures issued quarterly.

disclaimer: This report is intended solely for informational purposes based on publicly available filings as of March 2nd, 2026. It contains no investment advice or recommendations regarding abrdn Platinum ETF Trust (PPLT) securities. Readers should perform their own due diligence before making investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments