Paramount Skydance Advances Warner Bros. Discovery Merger While Managing Operational and Financial Complexity

PSKY reported modest operational improvements in Q1 2026, balancing merger-driven expenses with steady revenue growth amid evolving content and streaming markets.

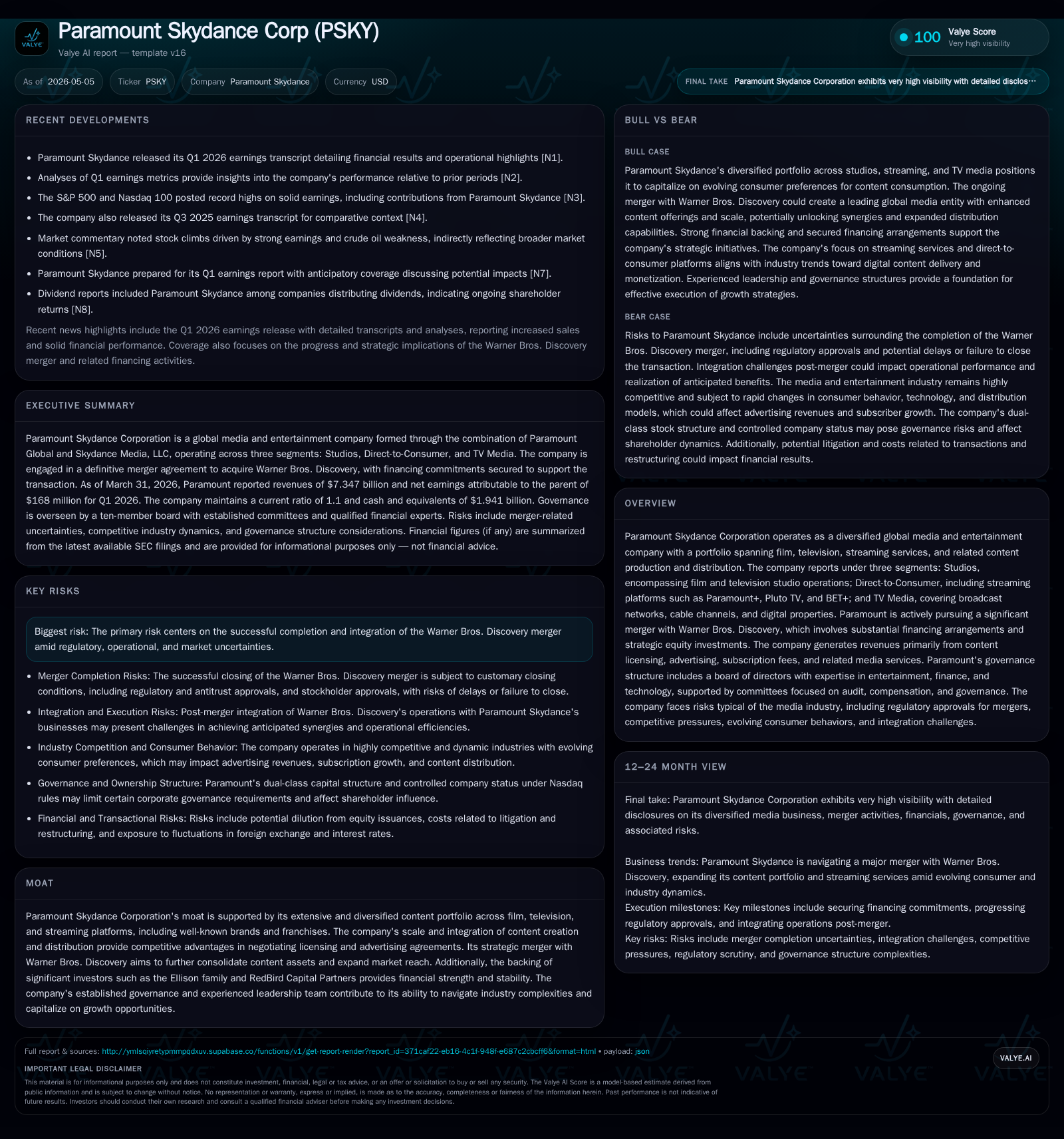

Paramount Skydance Corporation (PSKY) delivered a stable first quarter in 2026, with revenues increasing slightly to $7.3 billion, driven by strong studio and direct-to-consumer segments. Operating income improved, although increased amortization and restructuring costs reflected ongoing integration efforts ahead of the Warner Bros. Discovery (WBD) merger. The company’s business model centers on a diversified media portfolio spanning film, television studios, streaming platforms, and advertising-driven networks, positioning it well in a consolidating industry. Growth catalysts include the anticipated WBD merger, expanded streaming subscriber bases, and global content licensing opportunities. Risks remain around successful merger execution, high leverage from acquisition financing, and potential market shifts impacting advertising and subscription revenues. Near-term monitoring should focus on merger milestones, content investment effectiveness, and debt management metrics.

Recent Operating Update: Q1 2026 Performance Highlights

Paramount Skydance's latest quarterly filing dated May 4, 2026 ([S2]) reveals incremental operational progress against the backdrop of significant corporate transformation driven by its proposed acquisition of Warner Bros. Discovery (WBD). For the three months ended March 31, 2026, PSKY reported revenues of $7.347 billion compared to $7.192 billion in the prior-year period. This controlled revenue growth reflects robust contributions across its Studios and Direct-to-Consumer segments anchored by popular franchises and expanding streaming subscribers.

Operating expenses were tightly managed at $6.731 billion but included $362 million in depreciation and amortization—an increase signaling intensified capitalization of content assets—and restructuring plus transaction-related charges of $103 million related to ongoing integration initiatives tied to the WBD deal process.

Operating income was $616 million versus $550 million a year ago; however, net income attributable to PSKY’s parent stood at $168 million given higher income tax provisions ($155 million) and equity losses of approximately $62 million from investee companies—partially reflecting transitional impacts within industry partnerships ([S2]).

Liquidity remains adequate despite large-scale transactions in process; cash and equivalents were about $1.94 billion against total debt near $14.82 billion as of quarter-end ([F1]). The company recently utilized its revolving credit facility to finance a significant termination fee paid to Netflix amounting to $2.8 billion incurred during strategic reshuffling of content distribution agreements ([S5]). The revolving credit line commitments have been expanded temporarily to enhance financial flexibility.

An accompanying 8-K filing ([S3]) underscores continued diligence on shareholder communications amid these developments.

Business Model Overview

Paramount Skydance operates fundamentally as a diversified global media conglomerate spanning production studios specializing in film and television; direct-to-consumer streaming services including Paramount+, Pluto TV, BET+; as well as traditional television media comprising broadcast networks and cable channels ([S1]).

Revenue streams are principally derived from four categories:

- Content Licensing & Distribution: Selling film/TV rights globally across theatrical windows, pay-TV outlets, syndication deals.

- Subscription Fees: Recurring revenue through paid streaming services incentivized by original programming investments.

- Advertising Sales: Monetization of TV networks’ linear airtime plus digital platform ad inventory tied to substantial viewer engagement.

- Ancillary Media Services: Additional income from merchandise licensing and content-related partnerships.

This structure creates inherent cross-pollination whereby blockbuster franchises produced by the Studios serve as exclusive driver content for streaming platforms that build sticky subscriber bases willing to pay recurring fees while facilitating higher advertising inventory value across their broadcast/cable assets.

Margins vary: studios typically carry high upfront production costs with longer amortization cycles; streaming platforms absorb intensive content spend but benefit from subscription economics; advertising margins depend on audience scale and pricing power within dynamic market conditions.

The firm’s ability to bundle vast content libraries alongside multi-channel distribution creates negotiating leverage vis-à-vis advertisers and licensees while building consumer switching costs within its ecosystem.

Industry Structure & Competitive Position

The global entertainment industry is consolidating rapidly amid heightened competition for consumer attention driven by technological evolution towards on-demand video consumption. PSKY’s handling of studios + direct-to-consumer + traditional media forms an integrated platform notable for scale amidst fragmented peer groups.

Competing against entrenched giants such as Netflix, Disney (including Hulu), Amazon Prime Video, as well as legacy cable networks requires consistent investment in hit-driven franchises coupled with technology innovation in UX/UI for streaming platforms.

PSKY’s pending consolidation with WBD aims to rationalize overlapping assets like HBO Max under one roof creating a formidable combined entity expected to leverage cost synergies through content rationalization plus marketing efficiency gains ([S4]). This strategic maneuver intends to address market pressures from escalating content costs that can erode margins for less diversified operators.

Financial backing by influential private investors such as the Ellison family ensures access to patient capital supporting long-term content development cycles beyond typical quarterly sales pressures ([S26]).

Growth Drivers

WBD Merger Completion & Integration Synergies

The most significant immediate catalyst lies in consummating the Warner Bros. Discovery acquisition per regulatory approvals expected progressively through mid-2026 ([S4],[S21]). This merger will substantially enlarge PSKY’s aggregated content portfolio with tentpole IPs across multiple genres fostering cross-platform monetization opportunities beyond current reach.

Streaming Subscriber Expansion & Monetization Mix Shift

Streaming remains central to PSKY’s growth strategy which hinges on attracting subscribers through differentiated original offerings while progressively enhancing advertising revenue share via hybrid ad-supported tiers accessible globally ([S1],[N9]). Emphasis on balancing subscription price increases against competitive churn dynamics is critical here.

Global Content Licensing & Programming Sales

Beyond owned platforms pipeline enhancements involve selling premium content licenses internationally — an avenue bolstered by new output from combined studio capabilities serving territories where localized SVOD may not yet be dominant.

Advertising Market Recovery & Innovation

As linear TV viewing stabilizes post-pandemic disruption with digital addressable ads gaining traction on network properties ([S1]), the firm pursues advanced data analytics targeted advertising models promising improved CPMs while navigating audience measurement issues intrinsic to this evolving area.

Risks & Watchpoints

- Merger Execution Risk: The highly complex PSKY-WBD transaction faces potential regulatory hurdles outside U.S. jurisdictions along with operational integration challenges including retention of creative talent crucial for sustained franchise production ([S4],[S17]).

- Leverage & Refinancing Risk: Elevated debt levels (~$14.8B total) resulting from bridge loans used for acquisition financing pose refinancing risks especially if market conditions tighten or cash flow generation encounters headwinds ([F1],[S5]). Covenant compliance remains a key watch metric.

- Market Dynamics Impacting Advertising Revenues: Shifts in consumer behavior towards ad avoidance or changes in advertising budgets linked to economic cycles could pressure margin profiles notably within TV Media segment ([S1],[S4]).

- Content Spend Intensity & Amortization Pressure: Significant recent increases in amortization expense signal heavy upfront investment which if not matched by commercial success could impair earnings quality ([S2]).

- Talent Retention & Labor Relations: Creative personnel availability issues or labor disputes could disrupt production pipelines impacting release schedules critical for subscriber retention ([S17]).

- Stockholder Structure & Class Voting Rights Risks: Concentrated ownership limits stockholder influence potentially affecting governance dynamics relevant during transformative periods ([S1],[S13]).

What To Watch Next

Key upcoming milestones include:

- Closing announcements on regulatory clearances especially Europe and Asia regulatory bodies assessing antitrust risks of WBD combination.

- Quarterly subscriber count disclosures for Paramount+ and Pluto TV providing insight into competitive positioning against peer platforms.

- Updates on restructuring progress including realized cost synergies reported through mid-to-late 2026 filings.

- Debt covenant ratios previewed via quarterly filings revealing balance-sheet flexibility amidst elevated financial leverage.

- Market reaction to any announced strategic alliances or additional equity syndications aimed at diluting acquisition financing risk exposure ([S26]).

- Management commentary on navigating evolving advertising markets especially regarding addressability advancements across PSKY’s media portfolio ([N1],[N12]).

Financial Snapshot (As of March 31, 2026) [F1]:

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1941mm | |

| 2026-03-31 | ||

| Total debt | $14.8bn | |

| 2026-03-31 | ||

| Net debt | $12.9bn | |

| 2026-03-31 | ||

| Current assets | $11.6bn | |

| 2026-03-31 | ||

| Current liabilities | $10.5bn | |

| 2026-03-31 | ||

| Current ratio | 1.1x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD Millions) |

|---|---|

| Cash & Equivalents | 1,941 |

| Total Debt | 14,821 |

| Net Debt (Debt - Cash) | ~12,880 |

| Current Assets | 11,555 |

| Current Liabilities | 10,503 |

| Current Ratio | 1.10 |

Overall liquidity is supported by a sizable credit facility ($5B revolver), though usage spiked early Q1 due primarily to transactional costs including Netflix termination fees ([S5],[F1]). Meeting leverage covenants set at maximum total leverage ratio of 4.5x trailing EBITDA reflects ongoing scrutiny over indebtedness levels amidst large-scale acquisitions ([S5]).

Disclaimer

This analysis is based solely on publicly available disclosures up through May 2026 filings by Paramount Skydance Corporation (PSKY) including SEC materials and selected news sources. It does not constitute investment advice or recommendations but aims only to provide an informed review of company operations within its industry context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments