Pulmatrix’s Transition: from Innovation in Inhaled Therapeutics to Strategic Integration

Pulmatrix transitions from clinical-stage inhalation therapeutics development to a strategic merger with Cullgen amid pipeline pauses and capital constraints.

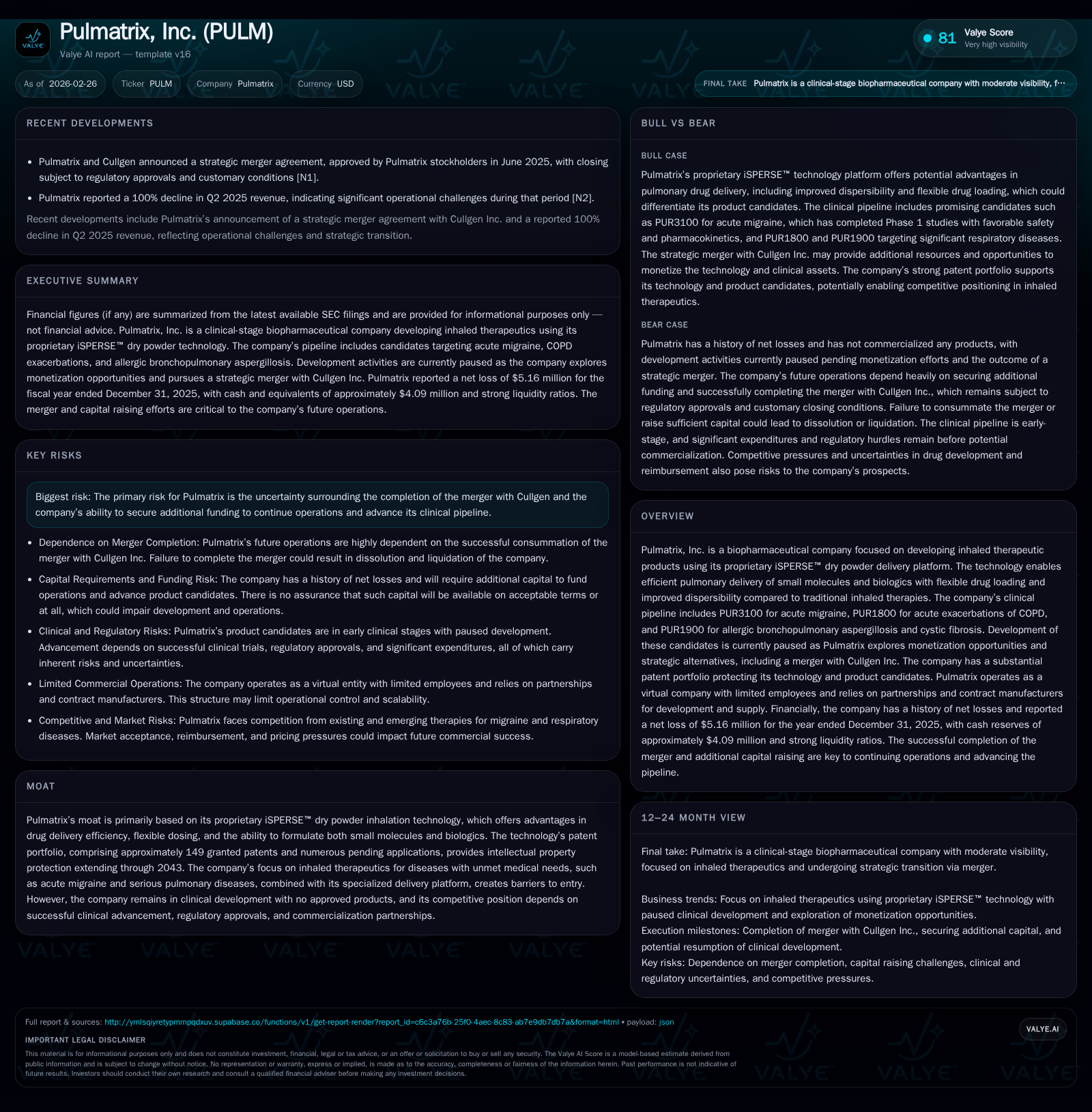

Pulmatrix, a biopharmaceutical firm pioneering inhaled therapies with its proprietary iSPERSE™ dry powder platform, has experienced significant financial losses typical of clinical-stage biotech despite a revenue surge in 2019. The company’s clinical development programs are currently paused as it pursues a strategic merger with Cullgen Inc., aiming to monetize assets and revitalize its corporate trajectory. Pulmatrix faces key regulatory and financial challenges ahead, including successful closing of the merger and navigating healthcare pricing reforms.

Historical Financial and Operational Trajectory: Growth and Investment Patterns

Pulmatrix's financial history reflects the volatility typical of clinical-stage biopharmaceutical companies. From 2016 through 2019, the company saw dramatic revenue growth characterized by a revenue jump from $153K in fiscal year (FY) 2018 to nearly $7.91 million in FY2019—a year-over-year increase exceeding 5,000% [F1]. This surge appears tied to initial partnerships or milestone recognitions typical within biotech licensing rather than sustained product sales.

Despite this top-line growth spike, operating losses have been persistent. Operating income improved from negative $18.95 million in FY2022 to about negative $5.17 million in FY2025 [F1]. Net income trends mirror this pattern with FY2025 net loss approximating negative $5.16 million — indicating some stabilization but continued unprofitability. Operating cash flows further highlight ongoing cash burn; the company posted roughly negative $5.43 million CFO in FY2025 while maintaining steady capital expenditures near $398K during recent periods [F1].

This profile underscores a classic research-driven bio-pharma lifecycle: investment-heavy with sporadic revenue primarily from licensing or partnerships rather than commercial product launches.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | -5 | -5 | 398000 | +46.0% |

| 2024 | -10 | -11 | -10 | 398000 | +32.3% |

| 2023 | -14 | -16 | -15 | 676000 | +25.0% |

| 2022 | -19 | -19 | -19 | 86000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -135.5 |

| 2024 | -11 | -106.8 |

| 2023 | -17 | -78.5 |

| 2022 | -19 | -60.5 |

Source: SEC companyfacts cache [F1].

Operating losses show improvement from heavy R&D spending normalization; yet sustainable profitability remains out of reach.

iSPERSE™ Technology: Core Innovation and Competitive Advantages

Pulmatrix’s core differentiator lies in its proprietary iSPERSE™ engineered dry powder inhalation technology designed for optimized pulmonary drug delivery [S1]. This platform produces small yet dense particles exhibiting superior dispersibility compared to traditional lactose-blend DPI formulations commonly used across inhaled therapies.

From a pharmacotechnical viewpoint, iSPERSE™ powders enable enhanced lung deposition efficiency potentially improving both local airway targeting and systemic uptake depending on molecule formulations—critical factors for therapeutic efficacy especially for diseases like COPD or CNS disorders.

This flexibility extends across molecular types—supporting both small molecules and biologics—a notable technical feat given biological sensitivity challenges inherent in dry powder formulations [S1].

Pulmatrix maintains an extensive patent portfolio with approximately 149 granted patents plus numerous pending applications consolidating protection until at least 2043 [S1]. These patents cover multiple facets of the formulation technology itself as well as process innovations crucial for manufacturing.

Clinical Pipeline Status and Strategic Pauses

Pulmatrix’s clinical pipeline historically included three lead candidates leveraging the iSPERSE™ platform: PUR3100 targeted acute migraine treatment; PUR1800 aimed at acute exacerbations of chronic obstructive pulmonary disease (COPD); while PUR1900 focused on allergic bronchopulmonary aspergillosis (ABPA) and cystic fibrosis management [N1].

However, as of early 2026 these development programs are paused following a strategic review that yielded a decision to explore monetization options rather than immediate further investment [N1]. This operational halt reflects challenges faced by smaller biotech firms encountering funding ceilings against high costs of late-stage trials.

This pause simultaneously mitigates near-term cash outflows while preserving asset value through intellectual property until clearer commercial pathways or deal structures materialize.

Merger with Cullgen: Strategic Rationale and Deal Risks

On November 13th, 2024 Pulmatrix entered into a merger agreement with Cullgen Inc., effectuated via Pulmatrix’s wholly owned subsidiary PCL Merger Sub merging into Cullgen which will survive as a wholly owned subsidiary post-transaction [N1][S1]. The transaction received stockholders’ approval mid-2025; however closing remains conditional upon customary regulatory consents including Nasdaq stock exchange listing approval and China Securities Regulatory Commission clearance under relevant filing rules for overseas listings by domestic enterprises [N1][S3].

Strategically this merger aims to provide Pulmatrix liquidity relief and operational scale by integrating Cullgen's business interests while allowing disposition or licensing of legacy assets—transitioning Pulmatrix from an isolated clinical-stage entity into a combined entity with broader potential pathways forward.

Key risks include:

- Dilution risk impacting current stockholder influence due to significant share issuance tied to Merger consideration,

- Market price dilution linked with expected common stock issuance,

- Uncertainties regarding timing causing erosion of anticipated benefits if deal delays occur,

- Integration execution risks typical of biotech mergers,

- Potential status as 'shell company' post-legacy asset disposal imposing stricter reporting requirements.

Executives from Cullgen are set to hold major management roles post-merger introducing shifts in corporate governance which current stockholders must monitor closely [S1].

Capital Structure, Liquidity, and Returns on Equity

At end-FY2025 Pulmatrix reported liquidity reflecting total current assets of approximately $4.13 million against current liabilities near $329K resulting in a robust current ratio around 12.55—a strong short-term solvency indicator uncommon for pre-commercial biotechs demonstrating prudent cash management [F1].

Cash flow dynamics underscore ongoing operations consumption: operating cash flow was negative roughly $5.43 million versus modest capex near $398K leading to an estimated free cash flow deficit around $5.83 million during FY2025 [F1]. These figures affirm reliance on external financing activities or transaction proceeds for sustaining operational runway.

Return on equity metrics remain deeply negative at approximately minus 135%, reflecting accumulated losses relative to equity base near $3.81 million at fiscal year-end [F1]. This underscores continued shareholder value erosion characteristic during extended pre-commercial stages absent revenue-generating products.

Investor focus should be placed on cash runway adequacy particularly bridging period until merger completion or successful asset monetization transactions materialize.

Regulatory Environment and Healthcare Pricing Pressures

Regulatory context presents complexities beyond classical FDA approval processes focused on safety/efficacy endpoints into compliance domains including manufacturing standards under cGMP guidelines applicable domestically and internationally [S6][S13].

Pulmatrix has limited experience executing late-stage filings such as New Drug Applications (NDAs), heightening risk for procedural delays or nonconformity potentially affecting timelines [S16]. Moreover post-approval marketing faces scrutiny under federal anti-kickback statutes and false claims provisions necessitating rigorous compliance frameworks even before commercialization begins [S4][S10][S12].

Healthcare pricing reforms further complicate market potential: the Inflation Reduction Act initiates Medicare price negotiations starting in 2026 coupled with inflation-linked rebates constraining manufacturer pricing powers—the impact on innovative inhalation therapeutics like those envisaged by Pulmatrix remains uncertain but potentially margin compressive [S11]. Additional state legislations impose transparency mandates potentially elevating compliance costs.

Global regulatory considerations include EU centralized marketing authorization pathways enabling streamlined cross-border access but requiring robust data packages aligned with EMA standards underscoring resource demands facing Pulmatrix especially under virtual company status without internal manufacturing infrastructure [S19].

Key Milestones Ahead and Investor Watchpoints

Critical milestones include:

- Successful closing conditions for the merger including Nasdaq’s approval for listing shares issued during the transaction,

- Regulatory sanction progress from the China Securities Regulatory Commission vital given cross-border securities offerings landscape,

- Post-merger strategic decisions concerning whether paused pipelines will resume development or undergo divestiture/licensing pivots,

- Monitoring capital structure changes driven by equity issuances tied to merger consideration impacting shareholder dilution dynamics,

- Tracking healthcare policy developments influencing reimbursement environments that could materially affect product commercialization viability following any future approvals.

Given the binary nature surrounding transaction closure events coupled with regulatory barriers intrinsic to pharmaceutical innovation cycles investors should maintain vigilance around forthcoming SEC disclosures regarding progress updates alongside any new development programs initiated post-merger integration phase.

Disclaimer: This report is prepared solely for informational purposes based on publicly available data up to February 26th, 2026 without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments