Quality Industrial Corp. Faces Leadership Change and Liquidity Strains in Core LPG Operations

QIND’s latest quarter reveals operational continuity amid executive turnover and financial pressure, highlighting industry positioning and growth challenges.

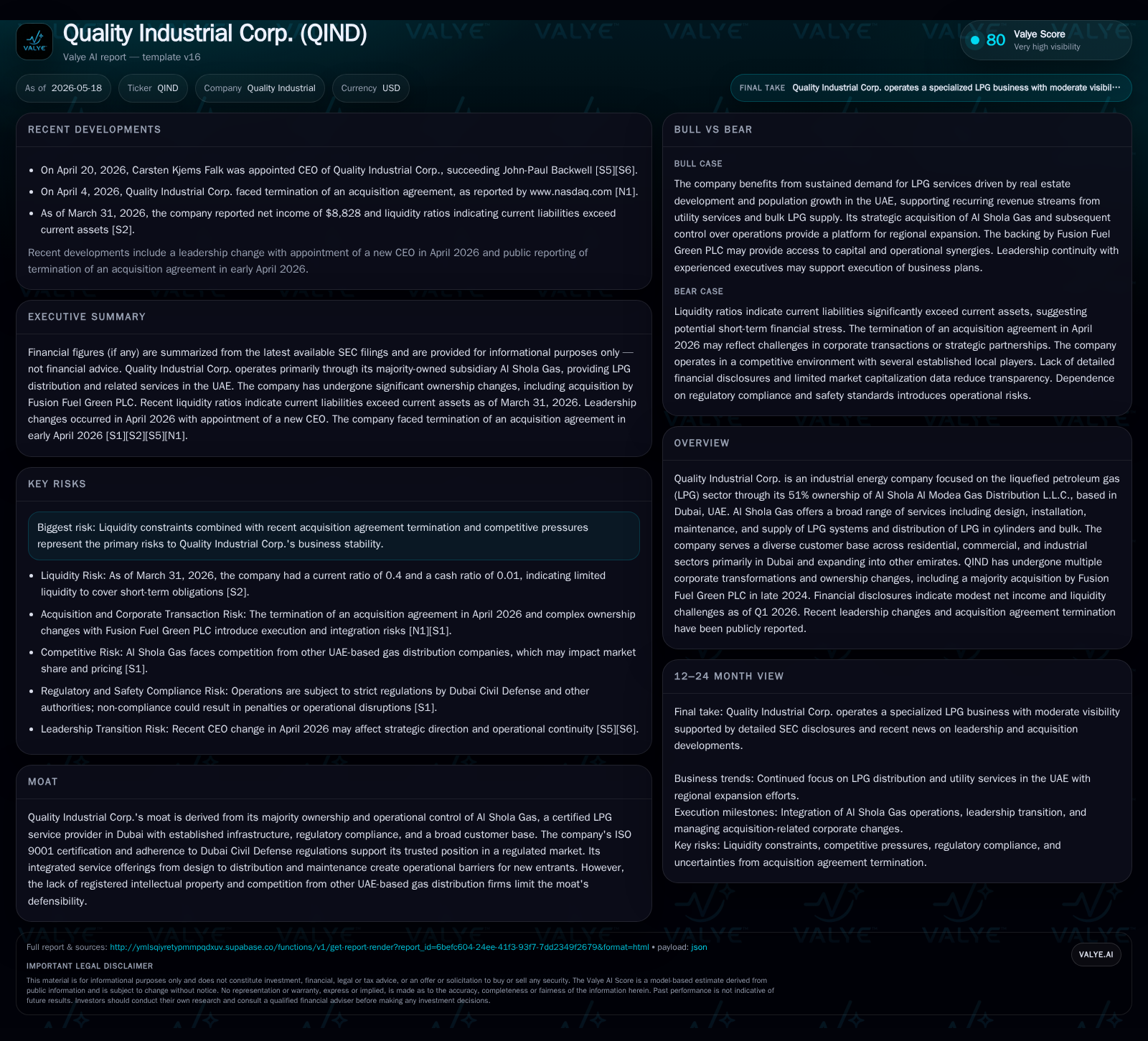

Quality Industrial Corp. (QIND) reported a recent leadership transition with a new CEO appointed in April 2026 after the prior CEO’s resignation. Operating primarily through its 51%-owned subsidiary Al Shola Gas in Dubai, QIND offers integrated LPG system services and distribution to diverse commercial and residential customers. The latest filings reveal liquidity constraints with a strained balance sheet, low current ratio, and ongoing legacy debt defaults, posing operational risks. However, the company benefits from established regulatory certifications and a multifaceted service offering that underpin its competitive presence in the UAE's growing LPG sector. Key growth drivers include geographic expansion within the UAE and rising LPG demand from real estate development, but execution is contingent on resolving financial hurdles and competitive pressures.

Recent Operating Update: Leadership Transition Amid Financial Constraints

Quality Industrial Corp. disclosed a significant leadership change in April 2026 with the resignation of CEO John-Paul Backwell effective immediately and the appointment of Carsten Kjems Falk as the new CEO [S3][S8][S9]. Falk brings extensive experience within QIND having previously served as interim CFO and Chief Commercial Officer, alongside leadership roles at Fusion Fuel Green PLC. This change suggests an internal strategy shift aimed at stabilizing operations amid ongoing financial challenges.

The most recent quarterly filing dated May 15, 2026 [S2] does not indicate material changes to core operations but underscores continuing liquidity issues embedded in the company’s balance sheet—specifically a cash position under $200K as of March 31, 2026 [F1], juxtaposed with current liabilities over $18 million which produces a precarious current ratio of just 0.4 [F1]. Notably absent from the filing is any indication of resolution on matured convertible promissory notes exceeding $2.5 million as of December 31, 2025 [S1], which remain unpaid and subject to default interest penalties that materially elevate financial risk.

Business Model Overview: Integrated LPG Solutions in an Expanding Market

QIND operates predominantly through its majority-owned subsidiary Al Shola Al Modea Gas Distribution L.L.C., based in Dubai [S1]. The business model centers on providing comprehensive liquefied petroleum gas (LPG) services encompassing engineering design, installation, maintenance, supply logistics (both bulk and cylinders), along with post-installation utility operations for residential, commercial, mixed-use developments, and industrial clients.

Revenue streams are diversified yet concentrated around three pillars:

- One-time engineering and system installation fees for new central LPG systems,

- Recurring revenue through metered utility services that provide steady cash flow post-project handover,

- Bulk LPG deliveries leveraging supplier relationships with Emirates General Petroleum Corporation allowing volume scale.

Cylinder distribution is robustly supported by an extensive delivery fleet enabling monthly dispatches exceeding 20,000 units within Dubai [S1]. Additionally, specialized logistics facilitate bulk LPG supply aligned with industrial customer demands across multiple emirates. This product breadth positions QIND with an operationally integrated value chain—from system conception through supply to maintenance—allowing cross-selling opportunities but also exposing the company to capital intensity inherent in fleet management.

Industry Structure and Competitive Position

Operating in Dubai’s tightly regulated LPG market imbues QIND with both regulatory advantages and barriers to entry for competitors. Al Shola Gas is certified by Dubai Civil Defense for safety compliance and holds ISO 9001 certification, establishing operational credibility essential for securing contracts from property developers and facilities managers who prioritize safety.

However, the absence of proprietary intellectual property or patented technologies—commonplace barriers in energy sector innovation—diminishes long-term defensibility against competing firms that may leverage scale or pricing flexibility. The company faces competition primarily from other UAE-based gas distribution providers who contend over limited high-density urban development projects.

QIND’s relatively modest scale compared to regional energy conglomerates combined with organizational instability (including recent CEO turnover) may constrain its ability to secure large-scale contracts or pricing power going forward.

Growth Drivers

Demand for QIND’s offerings is structurally linked to macro trends driving LPG consumption in the UAE:

- Sustained real estate expansion: Ongoing residential constructions fuel one-time installation revenues as well as ongoing metered service contracts.

- Population growth: Drives residential gas consumption volume increments.

- Geographic expansion: Efforts underway to penetrate northern emirates such as Sharjah, Ras Al Khaimah, Fujairah extend addressable markets beyond Dubai [S1].

- Industrial consumption: Food service outlets and manufacturing units requiring reliable bulk LPG supplies support volume growth.

Operational KPIs like total cylinders distributed monthly (>20,000), bulk LPG volumes (>500k liters/month), contract renewals on maintenance services will be key demand markers [S1].

Risks / Watchpoints / Growth Constraints

Key risks impeding QIND’s path forward include:

- Liquidity constraints: Extremely low cash reserves versus liabilities create solvency concerns; ongoing defaults on convertible notes raise the specter of legal enforcement actions jeopardizing asset control [S1][F1].

- Acquisition agreement termination: Recent news highlighted termination of a potential acquisition deal that might have alleviated funding or strategic burdens [N1].

- Leadership change execution: While Falk has relevant experience internally, abrupt CEO transitions can disrupt strategic continuity during critical turnaround phases [S3][S8].

- Competition intensification: Limited technological differentiation exposes QIND to pricing pressure amid other well-capitalized UAE energy service providers.

- Regulatory compliance costs: Strict adherence to Dubai Civil Defense standards requires continuous investment in operations and safety verification.

These constraints necessitate vigilant oversight on working capital management alongside successful execution against growth priorities.

What to Watch Next

Market participants should monitor several upcoming milestones:

- Quarterly updates focusing on liquidity trends including cash burn rates and any new financing initiatives.

- Progress on geographic expansion plans beyond Dubai into northern emirates quantified by new project awards or installations.

- Operational metrics such as cylinder sales volumes or recurring revenue contraction/expansion trends indicating customer retention strength.

- Management commentary around strategic repositioning post leadership change for indications of refocused business priorities or cost rationalizations.

- Any developments surrounding legacy debt restructuring or legal settlements pertaining to promissory note obligations.

These elements will clarify whether QIND can stabilize its balance sheet while leveraging structural demand drivers inherent in UAE’s growing energy infrastructure needs.

Brief Financial Profile Context

As of March 31, 2026, Quality Industrial recorded minimal cash & equivalents of approximately $172K against current liabilities nearing $18.0 million resulting in a current ratio of roughly 0.4—a classic indicator of short-term liquidity distress [F1]. Total debt stood near $432K (best-effort data mid-2024) with net debt marginally above $259K when accounting for available cash [F1].

Moreover, historically defaulted convertible promissory notes aggregating over $2.5 million remain outstanding since late 2025 [S1], complicated by elevated default interest rates (15–20%) and dilution risks due to conversion features below market prices. Operating losses persisted through end of fiscal year 2025 with net income negative by over $5 million illustrating profitability challenges [F1].

Cash conversion cycles are likely strained given capital-intensive logistics operations supporting bulk transport fleet management. Therefore financial discipline alongside successful recapitalization remains critical for sustaining operational viability.

This analysis synthesizes recent regulatory disclosures alongside industry context devoid of investment guidance or speculation beyond documented facts. It highlights Quality Industrial Corp.’s ongoing struggles balancing operational capacity within a regulated energy niche against persistent liquidity pressures amidst leadership transitions.

Financial position in context

As of 2026-03-31, companyfacts shows $172548 in cash and equivalents [F1]. Current assets of $7mm and current liabilities of $18mm imply a current ratio near 0.4x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments