Ferrari N.V. Accelerates Luxury Performance Through Scarcity and Capital Discipline

A detailed examination of Ferrari's financial evolution, scarcity-driven pricing power, and disciplined capital allocation underpinning its sustainable growth.

Ferrari N.V. has demonstrated consistent revenue and net income growth through strict control of production volumes, enabling premium pricing in the luxury automotive sector. The company's commitment to innovation, notably in electrification initiatives aligned with its heritage brand, alongside disciplined capital deployment via dividends and share buybacks, supports a strong return on equity exceeding 40%. However, Ferrari faces inherent risks tied to economic cycles impacting luxury demand and evolving regulatory frameworks. Monitoring forthcoming model rollouts and EV market acceptance will be critical for assessing future trajectory.

Unfolding Growth: Revenue and Profit Trends Through 2025

Ferrari's financial progression over the past four years presents a steadfast upward trajectory emblematic of its well-honed model balancing exclusivity against expanding profitability. Revenues have soared from approximately EUR 5.1 billion in FY2022 to about EUR 7.15 billion by FY2025 [F1], evidencing a compounded annual growth rate (CAGR) nearing 13%. This top-line surge reflects not a volume scale-up typical of mass manufacturers but rather deft management of product scarcity combined with resilient price elasticity typical of ultra-luxury goods markets.

Net income has similarly expanded from EUR 939 million in 2022 to just under EUR 1.6 billion by the end of 2025 [F1]. This increase is attributable to incremental operating leverage gains facilitated by fixed cost absorption as revenues rise without corresponding linear cost growth. Ferrari's unique position allows it to implement premium price points sustainably, extracting 'volume scarcity premiums' that underpin margins. These dynamics affirm Ferrari’s command over a luxury supercar niche that privileges brand aura and craftsmanship.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 7.1 | 1600 | +7.0% | +4.8% |

| 2024 | 6.7 | 1526 | +11.8% | +21.3% |

| 2023 | 6.0 | 1257 | +17.2% | +33.9% |

| 2022 | 5.1 | 939 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): CFO, OpInc, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 532 | 40.9 |

| 2024 | 440 | 43.1 |

| 2023 | 329 | 41.0 |

| 2022 | 250 | 36.1 |

Source: SEC companyfacts cache [F1].

Note: Operating income, cash flow metrics, buyback figures not available in the provided data.

The Scarcity Model: Controlling Supply to Maintain Premium Pricing Power

Central to Ferrari's moat is its disciplined control over production volumes—deliberately calibrated supply scarcity preserves the brand’s allure among an affluent clientele that associates exclusivity with value retention and prestige [S1]. This constrained production run optimization ensures that while the absolute unit numbers remain controlled, each vehicle commands a substantial volume scarcity premium that enhances revenue per car beyond direct manufacturing economics.

Within luxury automotive vernacular, this tight rein on output protects Ferrari from commoditization risks pervasive in broader auto sectors faced with aggressive competition and discounting pressures [S6]. The interplay between volume control and brand loyalty enables Ferrari not just to sustain elevated pricing but also to cultivate a secondary market where its vehicles retain or appreciate their worth—a virtuous cycle reinforcing demand elasticity on the higher end.

Innovation in Motion: Ferrari’s Investment in R&D and Electrification Strategy

Ferrari’s R&D approach reconciles the demands of maintaining heritage combustion technology excellence while charting a credible path toward electrification compliance [S4]. Notably, investment focuses intensely on platform electrification efforts—integrating electric powertrains without diluting the performance ethos distinguishing Ferrari’s supercars [N13].

Terms like 'powertrain innovation' and 'next-gen chassis development' typify Ferrari's attempt to craft bespoke technical solutions tailored for ultra-performance Electric Vehicles (EVs). This strategic pivot avoids generic electrification but instead targets engineering refinement that preserves driving dynamics highly prized by Ferrari enthusiasts [N2]. Such positioning underscores Ferrari’s intent to remain technologically superior within the luxury sphere despite increasing environmental regulatory pressures.

Anticipating the Road Ahead: Growth Drivers and Regulatory Challenges

Future growth prospects for Ferrari hinge upon sustained demand robustness among global luxury consumers willing to pay premiums for exclusivity balanced with product innovation [N4]. Key drivers include successful introduction of new models incorporating hybrid or fully electric propulsion without compromising traditional performance benchmarks — an engineering tightrope given legacy brand expectations.

Regulatory shifts present notable challenges; compliance costs tied to emissions standards and electrification mandates elevate operating expenses while accelerating investment cycles [S5]. Yet unlike mass-market automakers, Ferrari operates within a sector exhibiting less price sensitivity but greater exposure to cyclical wealth effects influencing discretionary spending patterns worldwide.

Capital Deployment Excellence: Share Buybacks, Dividends, and Cash Management

Ferrari exhibits exemplary capital allocation discipline highlighted by active dividend increases aligning with earnings growth alongside methodical share repurchase programs recently disclosed [S7][N7][N11]. Dividend payments have scaled upwards consistently—from EUR 250 million in FY2022 to over EUR 530 million by FY2025—as part of a stable shareholder return model supported by generous free cash flow generation reported periodically [F1].

Additionally, liquidity remains robust with cash and equivalents standing at approximately EUR 1.47 billion at year-end 2025—providing ample buffer for both organic investments in R&D capex and opportunistic capital returns . This balance mitigates financial leverage risks while optimizing equity base usage.

Return Metrics Decode: Understanding Ferrari’s Impressive ROE Trajectory

Return on equity (ROE) approximated at about 40.9% in FY2025 illustrates Ferrari’s operational efficiency translating net income into substantial equity returns despite inherent capital intensity associated with automotive manufacturing [F1].

The high ROE reflects disciplined working capital management intertwined with scalable net income improvements outpacing modest equity base increments annually. It denotes strong equity turnover augmented by profitability expansions rather than leverage amplification—consistent with cautious balance sheet stewardship designed not to compromise brand integrity or financial flexibility.

Risks on the Horizon: Economic Sensitivity and Sector Shifts

Economic elasticity remains pronounced given Ferrari’s client base predominantly composed of ultra-high net worth individuals whose purchasing behavior exhibits sensitivity toward global macroeconomic downturns or geopolitical uncertainties impacting luxury consumption levels [S5][N12].

Moreover, competitive pressures intensify as rival supercar manufacturers embrace electrification faster or innovate aggressively around alternative propulsion technologies potentially reshaping customer preferences over time [N9]. Regulatory compliance costs constitute another structural risk vector requiring ongoing investment that could compress margins absent equivalent pricing power adjustments.

Key Milestones to Watch: Signals for Future Operational Performance

Absent explicit forward guidance in filings or recent disclosures, attentive monitoring should focus on upcoming vehicle launches integrating EV capabilities—especially uptake efficacy reflecting consumer validation of platform electrification strategies [N4][N13].

Further indicators include updates on the scale and pace of share repurchase continuation alongside dividend policy evolutions offering insights into free cash flow trajectories post-capital expenditure soak-ups. Regulatory developments around European Union emissions targets or China’s EV incentives also warrant scrutiny as they materially influence operational cost structure assumptions.

This analysis synthesizes available SEC-reported data alongside recent news insights without extrapolating unavailable specifics such as operating cash flow or capex figures not present in company XBRL tags or filings cited. Investors should consider these constraints when evaluating liquidity or capital efficiency metrics herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

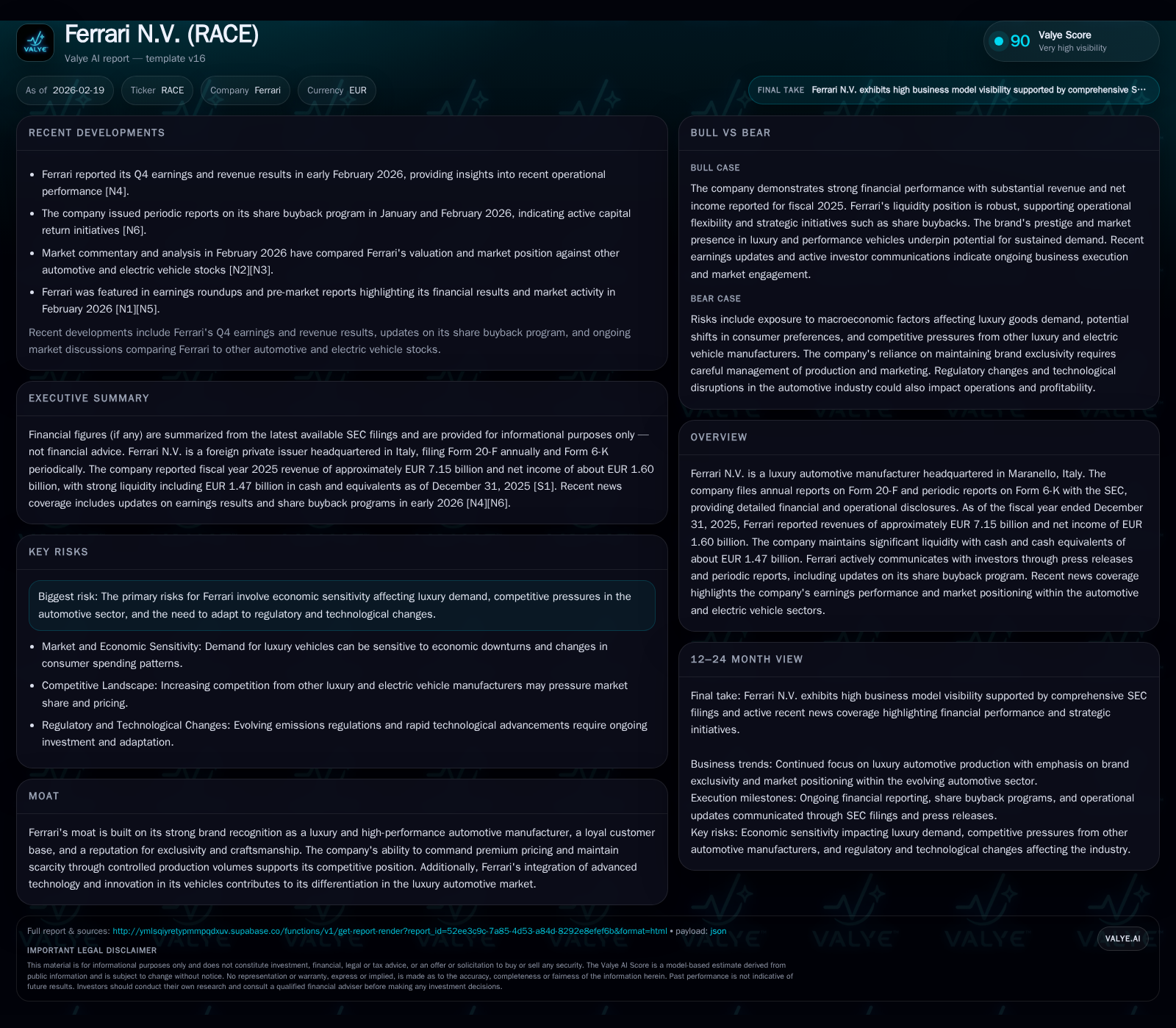

Comments