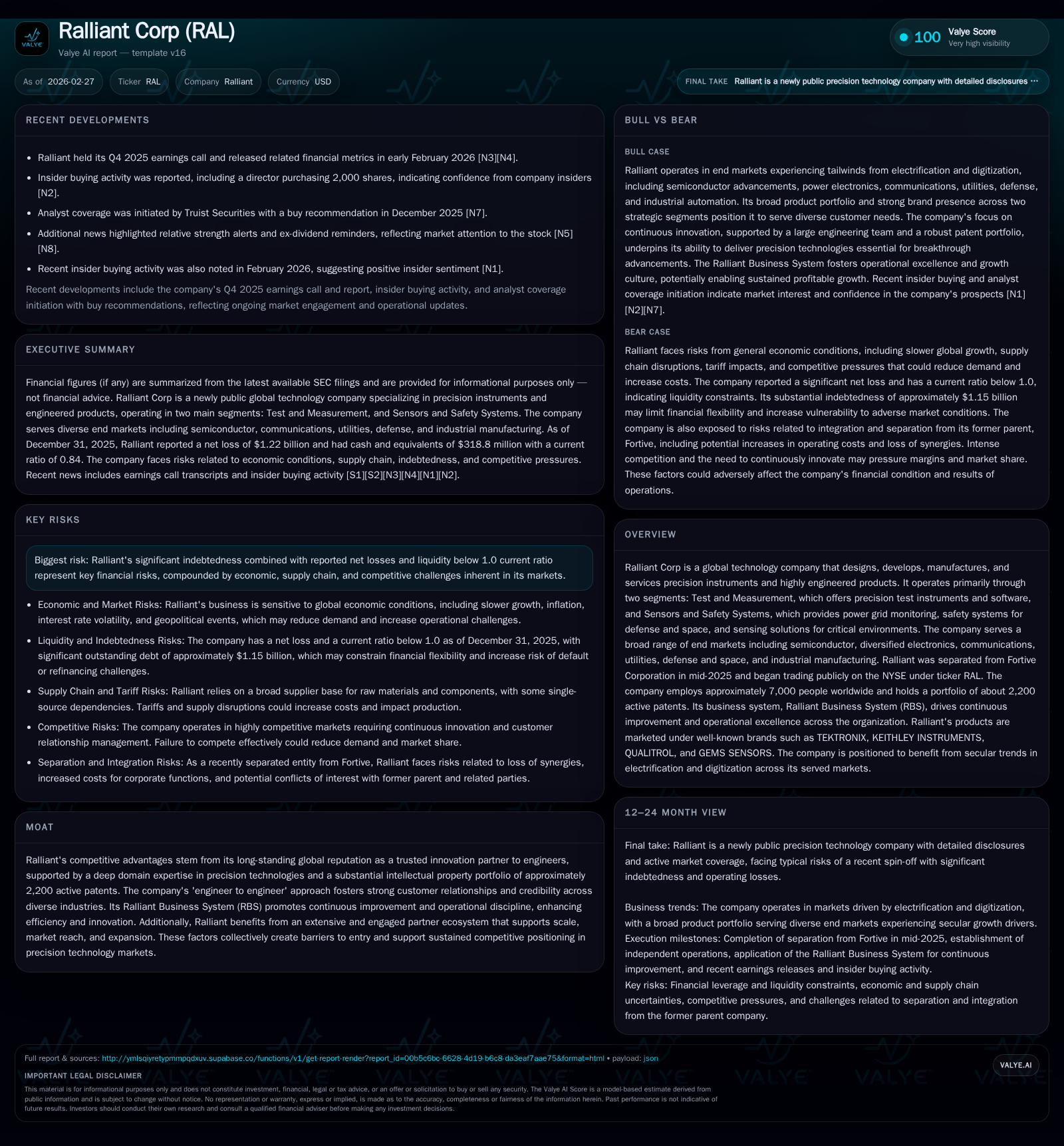

Ralliant Corp’s Transition to Independent Public Company Highlights Financial Strains and Growth Challenges

Following its 2025 spinoff, Ralliant Corp confronts significant net losses and liquidity constraints while leveraging its precision technology portfolio to drive future growth.

Ralliant Corporation, having separated from Fortive in mid-2025, now operates as an independent public company specializing in precision instruments and engineered products. Despite a rich patent portfolio and strong domain expertise, the company reported substantial net losses and a current ratio below 1.0 at fiscal year-end 2025. Its forward prospects hinge on expanding in electrification and digitization markets across semiconductor, defense, utilities, and industrial sectors. Operational discipline through its Ralliant Business System underpins growth ambitions, though heavy indebtedness and regulatory risks temper near-term outlooks.

Background and Corporate Overview

Ralliant Corporation emerged as an independent entity following its June 2025 separation from Fortive Corporation's Precision Technologies segment [S1]. Headquartered in Raleigh, North Carolina, Ralliant harnesses a global workforce of about 7,000 employees serving over 90,000 customers in more than 90 countries [S1]. The company designs, develops, manufactures, and services precision instruments and advanced engineered solutions through two primary segments: Test and Measurement (T&M) and Sensors and Safety Systems (S&SS) [S1].

The T&M segment provides high-performance test instruments like oscilloscopes, semiconductor test systems, power supplies, and associated software tools under notable brand names such as TEKTRONIX and KEITHLEY INSTRUMENTS. It primarily serves semiconductors, communications infrastructure providers, hyperscalers, electric mobility manufacturers, among others [S1][S18][S22].

The S&SS segment offers critical safety systems for defense aerospace applications alongside power grid monitoring technologies targeting mission-critical utilities infrastructure. It also supplies premium sensing products used in food processing, semiconductor equipment manufacturing, data centers for environmental monitoring, etc., operating brands like QUALITROL and GEMS SENSORS [S1][S18][S22].

Ralliant leverages approximately 2,200 active patents supporting sustained competitive advantages through longstanding global reputation as a trusted partner to engineers employing an "engineer-to-engineer" collaborative approach that enhances credibility across diversified industries [S1].

Historical Performance Drivers

Ralliant’s inaugural fiscal year as an independent company ended December 31, 2025. The year was marked by challenging operational results primarily reflecting non-cash goodwill impairments involving the EA Elektro-Automatik business within the T&M segment [F1][S1]. This impaired operating income substantially contributed to an operating loss of roughly $1.18 billion [F1]. Consequently, the net loss registered approximately $1.22 billion for the full year [F1]. Liquidity metrics showed pressure with current liabilities exceeding current assets—current ratio estimated at approximately 0.84 [F1].

Despite these headline losses weighing on profitability measures (approximate ROE of -74.8%), underlying cash flow fundamentals were more resilient. The company generated positive free cash flow of about $358 million after capital expenditures reflecting solid operational cash flow management amidst restructuring charges [F1]. This free cash flow profile highlights potential for financial recovery conditional on operational stabilization.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Revenue information for the standalone fiscal year is not explicitly stated in disclosed filings.

Future Growth Prospects

Ralliant aims to capitalize on shifting global trends toward electrification and digitization that drive demand for precision test instrumentation and reliable sensing technologies within multiple large addressable markets including semiconductors, diversified electronics manufactured for smart infrastructure applications, power utilities advancing grid modernization efforts, and aerospace defense programs requiring stringent safety protocols [S12][S18][S25][S26].

Sector-specific tailwinds include intensifying requirements for high power density semiconductor components that enhance energy efficiency critical in AI compute hardware; expansion of smart grids necessitating advanced power asset monitoring; rising aerospace launch frequency calling for reliable energetic material control; plus increasing automation in industrial manufacturing necessitating highly precise sensors [S12][S18][S25].

Ralliant leverages its robust patent estate alongside its culture fostered by the Ralliant Business System (RBS), which integrates lean operation principles with innovation acceleration via AI-powered methodologies to improve speed-to-market and continuous product improvement cycles [S17]. These capabilities are crucial given intense competition demanding ongoing enhancement to product capabilities as well as cost structures.

However, several factors could constrain growth: macroeconomic uncertainties including inflationary pressures could suppress capital spending among key customers; geopolitical tensions may disrupt supply chains or export licensing affecting international sales; fluctuating raw material costs impact margins; moreover regulatory compliance costs especially related to defense contracts (e.g., cybersecurity mandates) could reduce profitability cushions [S4][S13][S14].

Forecasts and Milestones to Monitor

While explicit full-year guidance remains undisclosed post-spin-off [N1], investor presentations from early February conferences emphasize plans to drive profitable growth through operational improvements guided by RBS metrics focused on quality delivery cost growth innovation [N3][S3]. Key upcoming milestones include leveraging AI integration into development pipelines to accelerate innovation velocity alongside expanding geographic penetration especially targeting growing markets such as Asia-Pacific electric mobility players [N3][S3]. Monitoring quarterly earnings releases will be critical to assess progress on reducing impairment-related non-cash charges burdening operating income.

Returns and Capital Allocation Strategy

Given significant end-of-year indebtedness approximating $1.15 billion coupled with interest expense risks tied to floating rate loans per disclosed credit agreements [F1][S9][S19], capital allocation prioritizes debt service capability over shareholder distributions currently. No dividends or repurchase programs have been initiated reflecting a cautious stance amid rebuilding balance sheet resilience [F1][S17].

Free cash flow generation capacity positions Ralliant favorably relative to servicing this debt burden provided operating performance improves consistent with ongoing RBS execution initiatives aiming at driving efficiencies across manufacturing scale economies supply chain optimization product portfolio rationalization [S17]. However risks persist if adverse conditions pressure cash flows triggering restrictive credit covenants outlined in credit facility agreements requiring maintaining leverage ratios or limiting strategic flexibility around asset dispositions dividend capacity or incremental borrowing [S9][S11].

Risks Summary

The company's risk profile is multifaceted:

- Financial risks from sizable indebtedness combined with tight liquidity highlighted by less than unity current ratio [F1][S9]; exposure to interest rate fluctuations due to variable rate debt adds uncertainty.

- Operational risks include dependence on complex supply chains vulnerable to geopolitical tensions natural disasters or pandemics causing sourcing disruptions increasing input costs or inventory obsolescence challenges [S12][S18].

- Competitive risk features intense rivalry necessitating continuous investment in innovation requiring management focus plus potential pricing pressures limiting margin expansion opportunities.

- Regulatory/compliance risk spans export controls especially relevant given global footprint diverse products including those used by defense agencies evolving cybersecurity mandates environmental health & safety regulations posing operational cost burdens plus potential litigation exposures noted in civil claims or warranty matters .[N2]

- Geopolitical/economic risks include foreign currency volatility impacting translation of international sales approx. half of revenues come outside U.S.; trade policy shifts such as tariffs impact cost structure; heightened political instability in emerging markets where Ralliant seeks growth may impede operations or collections.

Industry Context Analysis (Non-Company Specific)

Precision instrumentation markets exhibit heightened cyclical sensitivities correlating with semiconductor capex cycles energy infrastructure upgrades defense spending patterns combined with accelerated digitization mandates across manufacturing verticals globally. Consolidation trends among customers impose more bargaining power on suppliers driving demand for integrated end-to-end solutions that provide analytics alongside hardware which Ralliant must build into future offerings via RBS innovation pillar investments.

AI-driven testing tools increasingly play a role enabling faster iterative design validation especially important in next-gen chip architectures where performance gains amplify complexity exponentially thus elevating T&M importance. In sensing/safety systems innovations focused on miniaturization ruggedized field deployment improved diagnostics align with rising automation requiring persistent remote condition monitoring elevating relevance of companies like Ralliant.

Conclusion

Ralliant’s formative year as a public company reflected substantial transition-related headwinds marked by steep non-cash impairments producing large net losses yet supported by underlying operational cash flows demonstrating some financial resilience. The firm’s significant patent moat engineering-centric culture embedded through RBS offer meaningful levers for medium-term commercial recovery anchored on secular electrification/digitization market tailwinds spanning semiconductors utilities defense aerospace sectors.

Managing leverage amid macroeconomic uncertainties maintaining supply chain robustness navigating evolving regulatory environments executing on disciplined innovation acceleration remain vital guardrails shaping company trajectory further beyond initial public independence phase.

This report is based exclusively on publicly available information up to February 27, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments