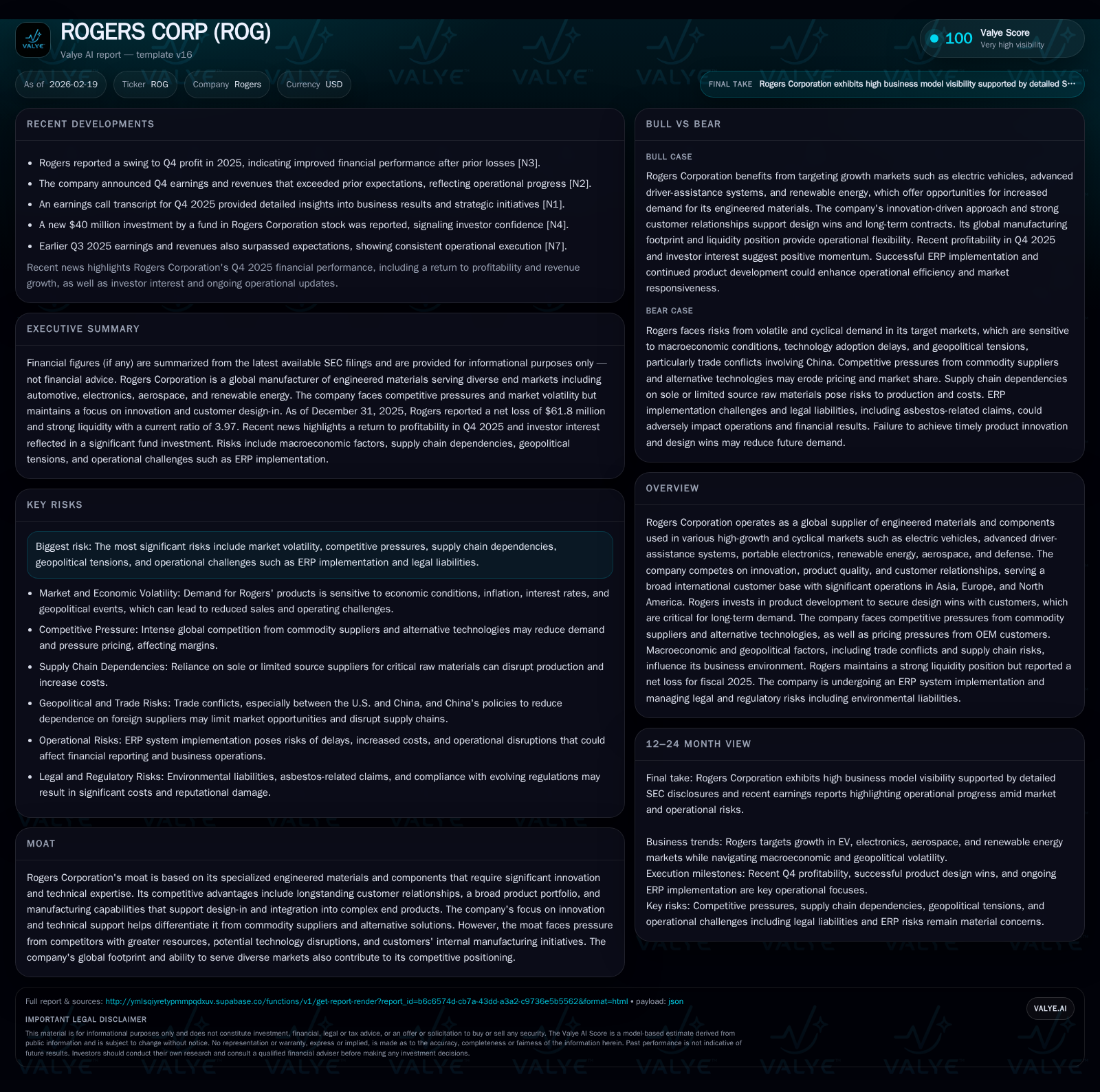

Rogers Corp Faces Growth Challenges Amid Innovation Demands and Geopolitical Risks

Specialized engineered materials provider Rogers Corporation experienced a sharp earnings downturn in 2025 while contending with competitive and macroeconomic headwinds.

Rogers Corporation, a global supplier of engineered materials critical to sectors like EVs, aerospace, and renewable energy, encountered a marked decline in operating and net income in 2025 despite solid operating cash flows. Key growth drivers remain product innovation and design wins within high-growth markets such as advanced driver-assistance systems and portable electronics. However, pricing pressures from OEMs, competitive intensity from commodity and alternative technology suppliers, supply chain constraints, and geopolitical tensions—especially impacting operations in China and Asia—pose risks. The company maintains a strong liquidity position and has deployed meaningful share buybacks recently. Going forward, monitoring the pace of new product adoption, capital investment efficiency, ERP implementation success, and regulatory compliance costs will be important.

Company Overview

Rogers Corporation is a global manufacturer specializing in engineered materials and components integral to products across several high-growth end markets. These include electric vehicles (EV/HEV), advanced driver-assistance systems (ADAS), portable electronics, renewable energy installations, aerospace applications, and defense equipment [N1][S1][S4]. The company's strategic edge lies in its continual product innovation capabilities coupled with robust technical engineering support designed to secure “design wins” — a critical factor for long-term stable demand as customers integrate these components into complex systems.

The global footprint is extensive with a substantial presence in Asia (notably China), Europe (including Germany, Belgium, England), and North America (headquartered in Chandler, Arizona) [S19][S24]. This international scale drives both opportunity and risk exposure.

Historical Performance

The financial trajectory over recent years shows some volatility reflecting sector cyclicality and macroeconomic impacts:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -62 | 101 | -45 | 30 | -336.8% |

| 2024 | 26 | 127 | 25 | 56 | -53.9% |

| 2023 | 57 | 131 | 85 | 57 | -51.5% |

| 2022 | 117 | 129 | 144 | 117 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 52 | 71 | -5.2 |

| 2024 | 20 | 71 | 2.1 |

| 2023 | 0 | 74 | 4.5 |

| 2022 | 25 | 13 | 9.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue data for FY2019 and earlier show inconsistency likely due to reporting changes; hence recent years' revenue is not displayed.

Operating income experienced a steep decline turning negative in the latest fiscal year after steady increases through FY2022–2024 [F1]. Net income followed this downward trajectory exposing operational pressures despite positive cash flows from operations which remain robust but diminished relative to peak years.

Capital expenditures dropped sharply indicating a pause or completion phase following earlier capacity expansions and investments related to new technology platforms [F1]. Meanwhile share repurchase activity accelerated markedly suggesting confidence in long-term value despite short-term earnings headwinds.

Growth Drivers & Challenges

Growth Catalysts

- Innovation-led design wins: Rogers invests heavily in R&D to continuously develop high-performance engineered materials critical for newer technologies such as electric vehicles' thermal management systems or ADAS sensor substrates [S16]. Successful integration of these materials into customer designs remains key.

- Expanding end-market demand: Growth opportunities persist in renewable energy infrastructure buildouts and increasing electrification/automation trends globally.

- Geographic diversification: With nearly three-quarters of sales outside the U.S., emerging market growth especially in Asia remains vital [S15].

Constraints & Risks

- Competitive pressure: Commodity material producers exert pricing pressure due to lower cost bases; alternative technologies may disrupt traditional application domains [S6].

- Supply chain vulnerabilities: Lean inventory models increase sensitivity to raw material shortages or cost spikes amid global logistics challenges [S10].

- Geopolitical & regulatory effects: Trade conflicts notably between the U.S.-China impact access to critical customers; tariffs and export controls can restrict market participation [S8][S9]. Environmental regulations (e.g., PFAS restrictions) will impose rising compliance costs [S14][S18].

- Operational execution risk: ERP system migration introduces complexity with potential for cost overruns or control lapses [S21].

- Asbestos litigation exposure: Legacy product liability claims continue as uncertain contingent liabilities [S7][S11].

Capital Allocation & Financial Health

Rogers maintains a strong net cash position supported by healthy operating cash generation surpassing capital expenditure needs even through challenging periods.

The firm returned over $52 million via significant share buybacks during FY2025 representing an aggressive capital return posture despite earnings losses [F1]. No dividend payout data is available within provided figures.

Approximate return on equity for FY2025 was negative at about -5%, illustrating net loss impact on equity base but operating cash flow resilience supports business sustainability [F1].

Current assets materially exceed current liabilities yielding a current ratio near four times indicating comfortable short-term liquidity coverage [F1].

Industry Context & Competitive Positioning

The engineered materials sector serves niche yet vital functions underpinning high-value industries that often have switching costs favoring established providers like Rogers with integrated services including engineering support and quality assurance [S6].

One intricate sector detail is Rogers' ability to customize substrate materials for ADAS sensors enabling heightened signal fidelity around electromagnetic interference—a technical barrier competitors struggle to match without equivalent R&D budgets or partnerships.

However, commoditization tendencies persist with some OEMs pushing component pricing downwards while exploring vertical integration options reducing third-party reliance—this dual pressure mandates continuous innovation balanced against cost competitiveness.

What To Watch Forward (Analysis)

- ERP implementation progress: Delays or issues could affect operational efficiency metrics or internal controls.

- Design win traction within EV/ADAS segments: Early indicators from customer inventories or shipment orders would signal organic growth sustainability.

- Supply chain stabilization: Improvement would mitigate margin compression risks.

- Regulatory cost impact: Especially related to evolving carbon emissions rules in Europe affecting production economics.

- Management capital deployment decisions: Future buybacks versus R&D spending balance informs strategic priorities amid weak earnings.

- Potential litigation settlements/cost escalations: Monitoring disclosures on asbestos claims or environmental liabilities remain material for risk assessment.

Summary

Rogers Corporation's specialized portfolio positions it well at the intersection of technology-driven growth markets requiring innovative material solutions. Yet the company faces multiple intertwined challenges including intensifying competition from lower-cost and alternate technology providers, significant geopolitical trade uncertainties centering on its China exposure (~41% of revenues), evolving regulations increasing operational complexity and cost burdens, as well as execution risks inherent to major IT system upgrades.

Financially strong cash flow generation supported ongoing capital return programs even as profitability faltered sharply in the most recent fiscal year signaling potential early-cycle softness that may require close monitoring of timing around new product ramp-ups or market recoveries.

As Rogers navigates this complex landscape, maintaining innovation momentum while reinforcing supply chain resilience will be central to regaining prior operating income levels amid broader industry cyclicality.

Disclaimer: This analysis presents factual data points and contextual interpretation based on publicly available filings and reports for informational purposes only without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments