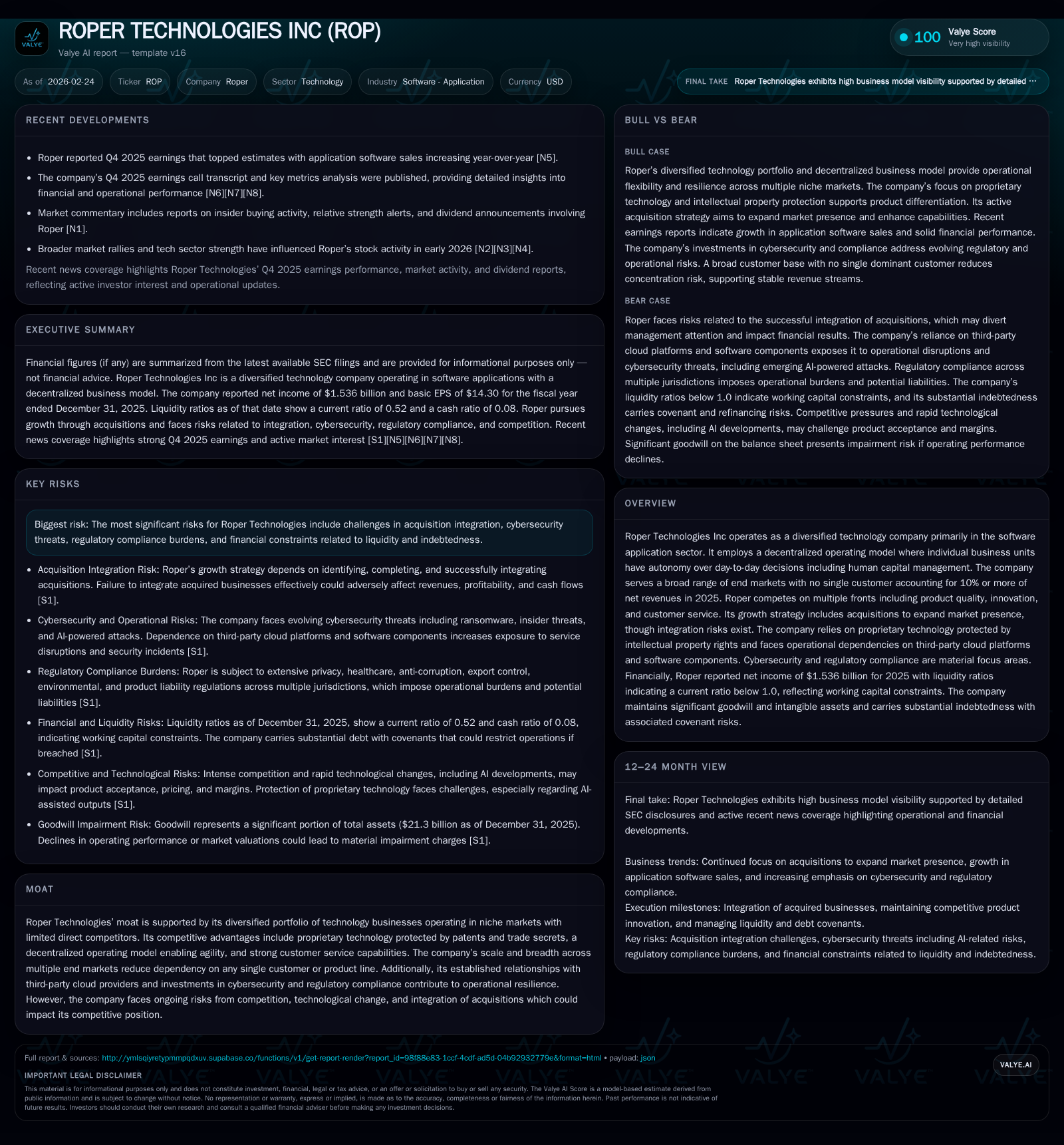

Roper Technologies’ Operating Leap and Strategic Challenges

Roper's significant earnings growth is propelled by its diversified tech portfolio while navigating acquisition integration and regulatory complexities.

Roper Technologies delivered a pronounced surge in operating and net income in fiscal 2025, driven by its diversified software application businesses and disciplined decentralized management. Its operating cash flow expanded steadily, underscoring strong internal capital generation amid conservative capex spending. The company's acquisitive growth model proved fruitful but poses integration risks alongside mounting regulatory compliance burdens, particularly in data privacy and healthcare sectors. Roper maintains disciplined capital allocation, balancing dividends with substantial share repurchases. Investors should watch for future acquisition execution, regulatory cost trajectories, and debt management as key determinants of ongoing performance.

A Compound Growth Story in Operating Income and Profitability

Fiscal year 2025 marked an extraordinary financial inflection for Roper Technologies Inc (ROP). Operating income catapulted to approximately $2.24 billion from $525 million in FY2024 — an eye-catching increase of around 326% YoY [F1]. Net income followed suit with a surge to about $1.54 billion from roughly $462 million the prior year, a remarkable rise of 232.3% [F1]. These gains underscore Roper's ability to leverage operational efficiencies within its software application portfolio amid broad market challenges.

This outsized climb was not driven solely by revenue growth—since top-line figures were not available per provided tags—but rather through refined execution including margin improvement, product innovation, and cost discipline within its decentralized units . Operating cash flow also exhibited strength by increasing 6.1% to $2.54 billion in FY2025 versus FY2024 [F1], illustrating potent cash conversion from core operations.

The sharp increase hints at effective absorption of fixed costs and scaling benefits inherent in software-related businesses where incremental sales can disproportionately amplify profitability. Notably, such leap reflects successful navigation of external pressures including competitive intensity and regulatory expenditure.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 1536 | 2.5 | 2.2 | +232.3% |

| 2024 | 462 | 2.4 | 0.5 | +18.8% |

| 2023 | 389 | 2.0 | 0.5 | -79.8% |

| 2022 | 1928 | 0.7 | 0.4 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 355 | 7.7 |

| 2024 | 322 | 2.5 |

| 2023 | 290 | 2.2 |

| 2022 | 262 | 12.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue data unavailable; Capex data prior to FY2018 unavailable; Buybacks not reported prior to FY2025 [F1]

Decentralized Business Model as an Agile Competitive Edge

Roper’s decentralized operating structure grants each business unit significant autonomy over day-to-day decisions including human capital and customer engagement strategies [S17]. This liberates individual units to innovate rapidly within their respective niches across diverse application software markets—from industrial automation controls to healthcare analytics.

This model reduces bureaucratic bottlenecks common in large conglomerates while enabling units to tailor offerings precisely according to customer demands, a critical advantage when competing on product quality, service flexibility, and intellectual property uniqueness [S20]. Moreover, it supports agility in adapting proprietary technologies protected by patents or trade secrets—a key moat element—while safeguarding against single-point operational failures.

In software segments increasingly exposed to rapid innovation cycles and SaaS/cloud platform dependencies, such decentralized governance promotes timely deployment of new capabilities including AI enhancements without waiting for centralized approvals—a vital edge amid technological disruption [S8]. Yet this autonomy requires robust corporate oversight for compliance alignment across jurisdictions given the complex regulatory landscapes faced globally.

Financial Highlights: From Income to Cash Flow Expansion

Examining balance sheet metrics reveals both strengths and challenges shaping Roper’s financial profile post-earnings leap [F1]. As of December 31, 2025, stockholders’ equity registered near $19.88 billion against net income of approximately $1.54 billion yielding an approximate return on equity (ROE) of 7.7%. While not stellar relative to some pure software players, this reflects measured capital utilization balanced against acquisition investments.

Operating cash flow climbed steadily by over six percent year-over-year to $2.54 billion from $2.39 billion in FY2024 reflecting durable core cash generation supportive of dividends and share repurchases [F1]. Capital expenditures showed only a marginal increase (~0.7%) consistent with efficient spending aligned with scalable software infrastructure rather than capital-intensive hardware buildout [F1][S14].

The conservative capex stance underscores operating leverage benefits while maintaining capacity for innovation investments and compliance obligations across regulated segments.

Liquidity-wise though, Roper shows tension: current assets approximate $1.93 billion versus current liabilities reaching about $3.73 billion at end-FY2025 producing a low current ratio near 0.52 indicating short-term obligations exceed readily liquid assets—an aspect warranting close monitoring of working capital management and covenant adherence given sizable debt exposure totaling over $9 billion [F1][S11].

Acquisition Strategy: Growth Engine and Integration Test

Acquisitions represent the cornerstone of Roper Technologies’ growth ambitions as management seeks expansion into new verticals while bolstering existing ones [S18]. This approach has fueled the scaling of multiple niche software platforms underpinning overall revenue and profit gains.

However, each deal introduces integration risk exposing challenges in harmonizing disparate technologies—especially given Roper’s patchwork portfolio where operational interoperability is non-trivial [S18]. Achieving synergy realization depends heavily on engineering effort aligning acquired IP with legacy platforms plus aligning cross-functional teams while preserving autonomous decision-making balance.

Investor vigilance is prudent regarding deal pipeline updates alongside qualitative disclosures on integration progress or headwinds encountered—a critical barometer impacting near-term profitability swings beyond organic factors.

Facing Compliance Complexities in Healthcare and Data Privacy

Regulatory compliance imposes mounting cost burdens on Roper’s businesses given global privacy laws including the European Union’s GDPR alongside U.S.-centric frameworks like the California Consumer Privacy Act (CCPA) currently expanded with additional processing limits especially affecting targeted advertising [S4][S15]. Compliance entails technical safeguards for data handling plus legal navigations across heterogeneous global statutes.

Healthcare-related regulations present further complexities chiefly due to FDA oversight governing diagnostic device manufacture and distribution under the FD&C Act alongside federal statutes like HIPAA that regulate sensitive health information privacy [S4][S5].

As software systems increasingly embed AI technologies sourced from third parties (OpenAI, Microsoft), cybersecurity resilience becomes paramount to prevent breaches potentially exposing personal data or intellectual property—necessary given growing cyber threats ranging from ransomware attacks to sophisticated persistent threats targeting critical SaaS providers [S6][S8][S23].

These factors collectively elevate compliance spend that can depress margins if not managed efficiently yet are indispensable for sustaining customer trust particularly within regulated verticals.

Capital Allocation: Dividends, Buybacks, and Returns to Shareholders

Roper maintains a balanced shareholder return strategy demonstrated by four consecutive years of dividend increases culminating at approximately $355 million paid out in FY2025 up from $262 million in FY2022 suggesting commitment to consistent income streams alongside steady earnings growth [F1].

Complementing dividends was significant share repurchase activity with nearly half a billion dollars deployed towards buybacks in FY2025 evidencing confidence in intrinsic value enhancement backed by free cash flow estimated at roughly $2.49 billion (operating cash flow minus capex) underpinning such distributions without unduly raising leverage risk [F1].

Maintaining dividend coverage ratio stability amid earnings volatility will remain key while strategically balancing buybacks against acquisition funding needs particularly as debt remains elevated requiring stewardship over financial flexibility [S11].

Outlook and Risks: What Investors Should Monitor Next

Looking ahead, several factors warrant close observation:

- Quarterly earnings guidance updates which may reveal sustained momentum or potential contraction influenced by macroeconomic or sector-specific dynamics [N3][N4][N9]

- New acquisition announcements or completion reports indicating continued inorganic expansion or potential strain on integration capacity

- Regulatory environments around AI adoption evolving notably under regulations like EU’s AI Act posing operational hurdles impacting product design or deployment timelines [S10]

- Liquidity position monitoring due to current ratio below benchmark levels paired with sizeable indebtedness requiring adherence to credit covenant terms avoiding defaults or increased borrowing cost burdens [S11]

- Cybersecurity posture maintenance especially concerning third-party cloud provider dependencies (AWS, Azure) where outages or pricing shifts could impair service continuity and profitability [S6]

- Market sentiment analysis including options activity potentially presaging volatility shifts tied to event risk exposures or macroeconomic changes affecting discretionary IT spends [N14]

In sum, while Roper boasts robust earnings improvement powered by diversified niche software businesses managed through decentralized autonomy facilitating agility and innovation—the company must prudently manage acquisition complexities alongside intensifying regulatory costs relating especially to data privacy and healthcare mandates amidst high leverage conditions.

Disclaimer: This analysis is for informational purposes only based on publicly available data as of February 24, 2026 ([F1], [N#], [S#]). It is not investment advice nor should it be construed as a recommendation regarding any securities of Roper Technologies Inc or any other entity.

Comments