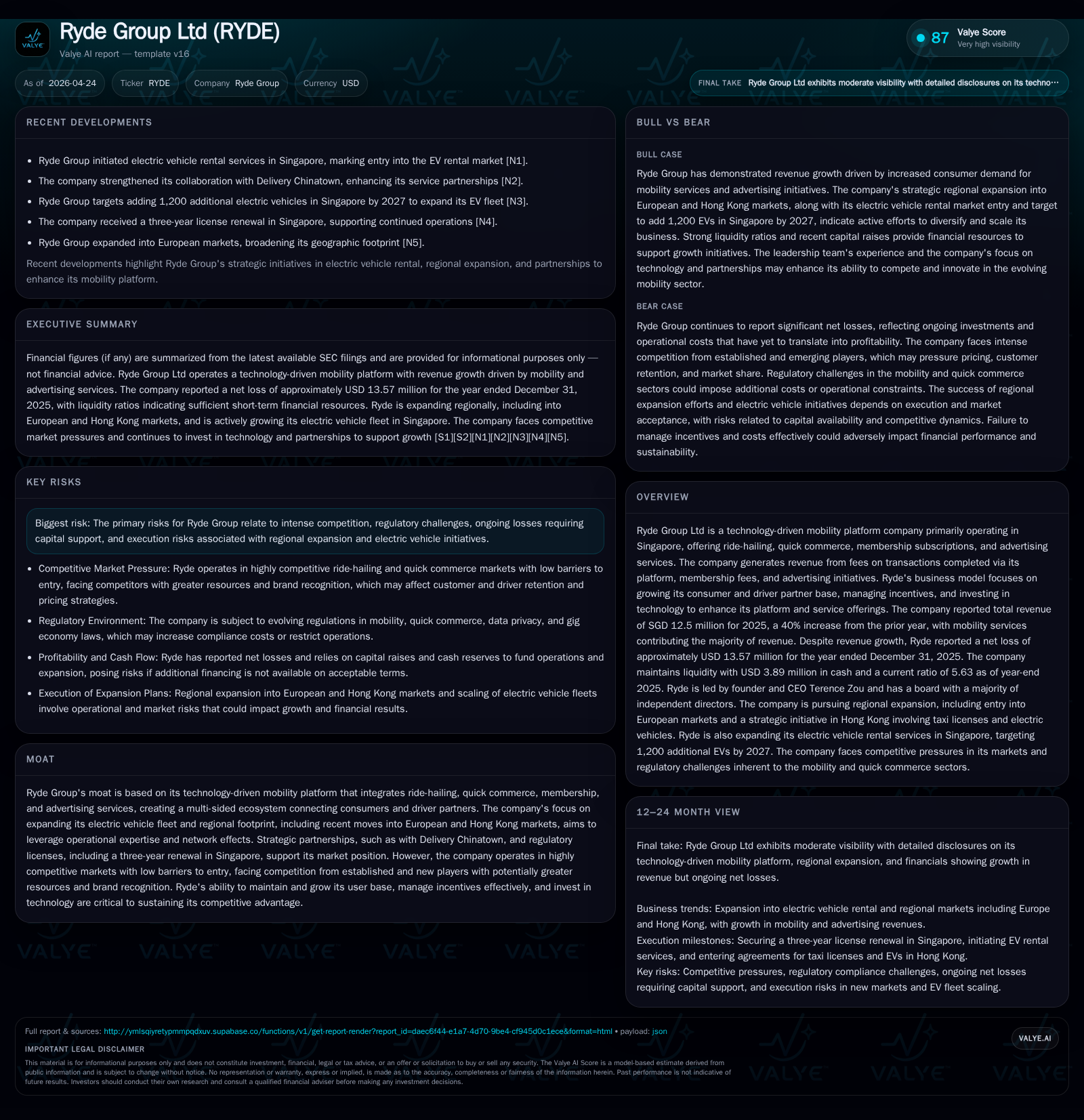

Ryde Group’s Expansion and Platform Synergies Set to Reshape Regional Mobility

Ryde Group accelerates its regional growth strategy with key market entry into Hong Kong, leveraging platform integration and capital raises.

In its latest quarterly filing dated April 14, 2026, Ryde Group Ltd announced strategic moves to expand beyond its core Singapore base by securing an option to acquire Hong Kong taxi licenses and electric vehicles, reflecting a targeted push into densely populated urban centers prioritizing sustainable mobility. This expansion is supported by a recent private equity raise closing on April 13, 2026, signaling Ryde's commitment to capital-intensive geographic diversification. The company’s business model synergizes ride-hailing, quick commerce, subscriptions, and advertising through an integrated technology platform geared toward network effects among consumers, driver partners, and advertisers. Competitive pressures remain intense with low barriers to entry and strong rival incumbents, but Ryde’s platform approach and EV fleet focus offer growth levers amid regulatory challenges and cost constraints. Financially, Ryde sustains liquidity yet continues generating net losses as it scales.

Recent Operating Update: Hong Kong Expansion and Funding Raise

Ryde Group Ltd recently unveiled a pivotal development aligned with its strategic regional expansion ambitions. In the quarter ending April 14, 2026, the company entered into a Call Option and Agency Agreement granting it the right—but not the obligation—to purchase up to 50 taxi licenses along with an equal number of electric vehicles in Hong Kong via Envision W International Ltd [S2]. This initiative taps into Hong Kong’s dense urban population demanding reliable transportation services enhanced by environmental sustainability preferences. The option agreement requires a refundable deposit of USD 14.5 million valid for six months from April 14th.

Simultaneously, Ryde closed a previously announced private placement on April 13th issuing approximately 37.25 million Class A shares at $0.40 per share [S3]. The influx of fresh equity underscores management's resolve to back geographic diversification and capital-intensive projects like fleet electrification despite continuing operating losses. By concretely linking capital raising efforts to strategic asset acquisition rights in one of Asia's most dynamic urban markets, Ryde signals a decisive shift from solely Singapore-centric operations to a broader regional footprint.

Business Model: Multi-Sided Mobility Ecosystem Anchored in Technology

At its core, Ryde operates a multi-sided digital mobility platform generating revenue primarily through transaction fees on ride-hailing and quick commerce orders processed via its app. Membership subscription fees add recurring revenue streams while advertising initiatives monetize platform traffic further [S1]. This integration positions Ryde as more than just a ride service—it's cultivating a super app ecosystem where consumer demand drives driver partner engagement and vice versa.

This network effect is critical; the company actively promotes user acquisition for both customers and drivers through incentive programs designed to stimulate platform usage frequency while balancing unit economics carefully around fare rates and commission structures [S1]. Technological investment supports app enhancements and infrastructure upgrades necessary for scaling hyperlocal operations across diverse regulatory jurisdictions encountered beyond Singapore.

Competitive Environment: Navigating Intense Rivalry and Market Fragmentation

Ryde faces an aggressive competitive landscape comprising large incumbents with substantial marketing heft alongside nimble new entrants deploying low-cost or specialized offerings [S5]. The ride-hailing sector’s low barriers enable rapid competition-induced price adjustments with upward pressure on incentive spend for drivers and riders alike.

Customer retention is challenged not only by pricing but also by differentiated service experiences ranging from vehicle quality to app usability. Competitors may rapidly integrate product feature parity or innovate with alternative pricing models which compress Ryde's margin leverage. Moreover, consolidation dynamics within the Asian mobility space could concentrate market power among fewer entities with deeper pockets threatening Ryde’s scale advantages.

Growth Drivers: Platform Synergies, Regional Footprint, and Electric Vehicle Focus

Ryde’s pathway for scaling revenue encompasses multiple interrelated growth pillars:

- Geographic expansion, particularly the Hong Kong foray targeting ultra-dense urban transport needs aligned with sustainable EV deployment.

- Platform synergies that cross-leverage quick commerce ordering capabilities alongside core mobility services fostering higher wallet share per user.

- Membership enhancements aimed at increasing locked-in customer revenue streams.

- Electric vehicle fleet adoption addressing growing regulatory mandates favoring low-emission transportation while appealing to environmentally conscious riders.

Ryde believes hyperlocal market customization combined with scalable technology infrastructure can unlock efficiencies vital for profitability gains over time [S2], [S1], [F1].

Key Constraints: Competition, Regulatory Hurdles, and Cost Management

Among notable structural headwinds are intense price competition necessitating sustained incentives that erode margins; complex regulatory landscapes especially around licensing (evident from the Hong Kong taxi license maneuver) requiring cautious compliance investments; data privacy laws impacting operational flexibility; evolving gig economy rules that influence driver-partner labor models; and execution risks associated with foreign market entry including cultural adaptation challenges [S9].

Capital requirements remain substantial given ongoing net losses (about $13.57M FY2025) coupled with negative operating cash flows demanding frequent equity or debt financing rounds which can dilute existing shareholders or increase leverage exposure respectively [F1]. Balancing aggressive growth versus long-term profitability remains a critical execution dimension.

Strategic Partnerships and Innovation as Revenue Levers

Ryde leverages strategic collaborations such as its alliance with insurance firms providing tailored insurance services for platform users—a source of supplementary revenue beyond traditional ride commissions [S1].

Prospective partnerships spanning food delivery chains or vehicle rental fleets offer avenues for incremental revenue modules while potentially lowering operating costs through shared resource utilization. Such alliances deepen ecosystem stickiness creating switching costs difficult for competitors to replicate immediately.

Outlook and What To Watch Next

Investors should monitor several key milestones including:

- Whether Ryde exercises its option within the six-month window expiring October 2026 for acquiring the Hong Kong taxi licenses and EV fleet,

- Progress in scaling EV deployment successfully without ballooning operational costs,

- User base growth metrics particularly post-Hong Kong entry reflecting consumer adoption rates,

- Any subsequent capital raises driven by cash burn or growth initiatives,

- Regulatory developments impacting licensing renewals or data compliance standards,

- Trends in profitability improvements vis-à-vis incentive spending rationalization.

Fiscal discipline paired with timely execution of expansion plans will be essential for Ryde’s sustainable competitive positioning.

Financial Health Overview: Liquidity, Profitability, and Capital Structure

Ryde closed FY2025 with revenues totaling approximately SGD 12.5 million (about USD equivalent considering exchange rates), marking a robust year-over-year increase of around 40% over FY2024 levels [F1]. Nonetheless, operating income remained negative at roughly USD -4.87 million while net losses amounted to about USD -13.57 million reflecting continued investment in growth areas [F1].

Operating cash flow was heavily negative at approximately USD -18.3 million indicating burn driven by cost-intensive incentive programs plus technology investments surpassing cash inflows from operations [F1]. Capital expenditures stood modestly at around USD 3 thousand suggesting focus on technology over physical asset accumulation currently.

Balance sheet strength is anchored by USD 3.89 million in cash equivalents paired against current assets far exceeding current liabilities resulting in a current ratio above 5.6—a comfortable liquidity cushion allowing short-term obligations management without strain [F1]. Total debt was modest based on last available figures ($2.16 million at end-2023), implying limited leverage though updated debt profiles remain unconfirmed as of latest filings [F1].

Overall financial posture supports Ryde's near-term expansion plans but ongoing losses underline dependency on external funding sources until meaningful operating profitability materializes.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -14 | -18 | -5 | 3000 | +0.7% |

| 2024 | -14 | -9 | -6 | 20000 | -40.6% |

| 2023 | -10 | -1 | 2000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -18 | -54.8 |

| 2024 | -9 | -470.2 |

| 2023 | -1 | 174.7 |

Source: SEC companyfacts cache [F1].

- Revenue converted estimate based on SGD figures provided [F1]

Disclaimer: This analysis is based solely on publicly available filings as of April 2026 without any investment recommendation or speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments