Rezolute Pursues Regulatory Approval in Wake of Phase 3 Trial Outcomes

The latest quarterly filings reveal Rezolute’s clinical trial challenges and regulatory strategies while underscoring its strong liquidity position.

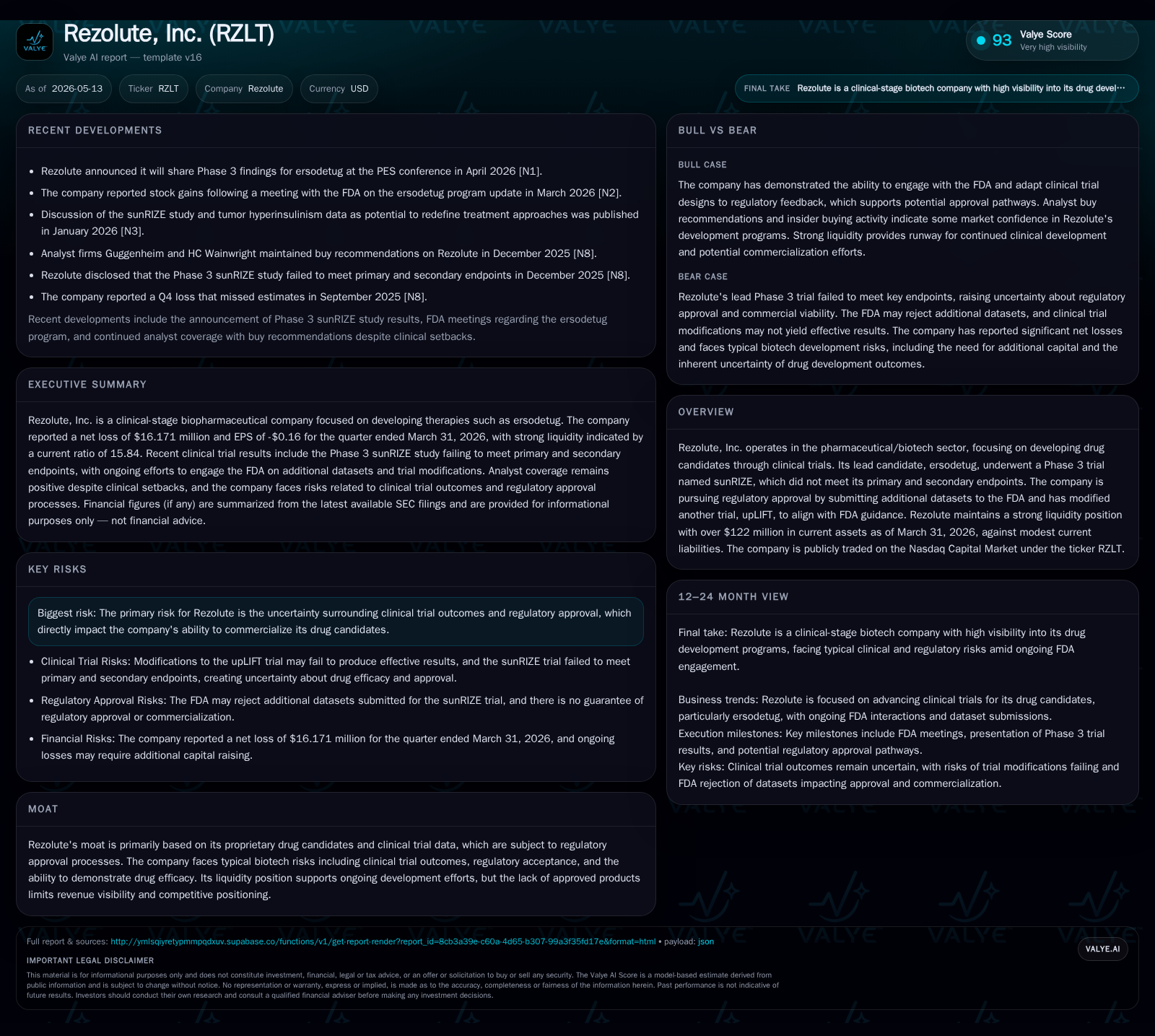

Rezolute reported that its pivotal Phase 3 sunRIZE trial for ersodetug did not meet primary or secondary endpoints but is actively engaging with the FDA by submitting supplemental datasets for review. The company has also modified its ongoing upLIFT trial to better align with FDA guidance, aiming to improve efficacy signals without placebo controls. While these developments prolong uncertainty, Rezolute’s liquidity position remains robust, supporting continued clinical programs and regulatory efforts. Risks persist around trial outcomes and FDA acceptance, but upcoming milestones could clarify the path forward.

Latest Operating Update: Clinical Trials and Regulatory Interaction

Rezolute's recent quarter ending March 31, 2026, accompanied by the May 12 filings ([S2], [S3]), centers on updates to its clinical development programs. The headline event continues to be the Phase 3 sunRIZE trial of ersodetug, which failed to meet both primary and secondary efficacy endpoints. Though disappointing, this outcome has not closed the door on regulatory progress; notably, the FDA has expressed openness to reviewing additional datasets beyond the sunRIZE topline results. Rezolute is submitting study reports and analysis data for independent FDA evaluation, signaling a pivot towards supplementing existing data rather than relying solely on traditional endpoint success.

Alongside this, Rezolute modified its upLIFT trial design following discussions with the FDA—specifically removing the randomized, double-blind, placebo-controlled framework using hypoglycemia events as endpoints ([S2], [S12]). These modifications aim to enhance the probability of demonstrating drug efficacy under an adjusted protocol that may better reflect real-world effectiveness without placebo-controlled benchmarks. However, the company candidly notes there is no assurance these changes will yield favorable outcomes or fully satisfy regulatory requirements.

Business Model and Pipeline Overview

Rezolute operates as a clinical-stage biopharmaceutical company focused on developing proprietary drug candidates through rigorous multi-phase trials. The core value lies in advancing candidates through clinical validation stages critical for eventual commercialization rights and market entry ().

The lead candidate, ersodetug, is positioned for unmet medical needs targeted via neurological or metabolic pathways – typical of innovative biotech ventures investing heavily in research-intensive clinical development rather than commercial product sales at present. With no approved products generating revenues yet, financial sustainability hinges primarily on capital markets support aligned with pipeline progress milestones.

Revenue mechanics involve securing potential milestone payments from partnership deals (if any), followed by eventual product sales upon approval — all contingent on successful clinical outcomes and regulatory green lights. Contractual engagements with clinical research organizations (CROs), manufacturing partners, and regulatory consultants compose significant operating expenses during development phases.

Industry Positioning Within Biotech Drug Development

Rezolute sits squarely in the high-risk/high-reward pharmaceutical biotech sector reliant on innovation pipelines validated through FDA (and other regulators’) approval processes (). The company faces a competitive landscape populated by similarly situated small-to-mid-cap biotechs grappling with equivalent scientific uncertainties and regulatory hurdles.

A key moat resides in proprietary molecules backed by intellectual property rights bolstered during early research phases. Yet this moat is vulnerable until commercial launch due to absence of product differentiation observable by prescribers or payors.

Pricing power remains contingent on ultimate approval status and market access conditions. Capacity constraints are typical of biotechnology firms depending on CRO networks instead of manufacturing scale at this stage.

Switching costs are largely irrelevant since patients cannot access these therapies outside trials; instead, retention pertains chiefly to investigator sites and patient enrollment continuity. Hence execution risks associated with patient recruitment, retention, data integrity, and compliance weigh heavily within this industry segment.

Growth Drivers: Unlocking Value Through Trials and Approval Pathways

Development momentum at Rezolute depends fundamentally on regulatory dialogue outcomes and subsequent trial progress success. Key growth catalysts include:

- FDA Acceptance of Supplemental Data: Submission of additional datasets from sunRIZE for independent review opens potential pathways for conditional approval or expanded data requirements. Positive reception could materially alter valuation expectations.

- Modified upLIFT Trial Results: Aligning trial design closer to FDA preferences aims to foster clearer efficacy signals without placebo controls; successful endpoints here would represent validation for ersodetug’s therapeutic claims.

- Potential New Indications or Partnerships: Expanding therapeutic applications or licensing deals could broaden market opportunity scope beyond initial target populations ([N1]).

- Investor Confidence via Presentations: Public disclosure of phased findings (such as PES conference presentations) helps maintain visibility among stakeholder groups despite delayed definitive approvals.

This multi-pronged approach illustrates how Rezolute is attempting to engineer checkpoints that de-risk future stages incrementally while preserving optionality around commercial prospects.

Risks and Constraints: Clinical Outcomes and Regulatory Hurdles

Rezolute's binary risk profile intensifies given recent Phase 3 trial failures. Principal threats detailed in the May 12 10-Q update ([S2], [S12]) include:

- Efficacy Uncertainty: Despite protocol modifications in upLIFT, no guarantees exist that efficacy endpoints will be met or accepted by regulators.

- FDA Rejection of Supplemental Datasets: Even with dataset submissions providing granular information beyond topline failures, the FDA may decline these as sufficient grounds for approval.

- Regulatory Delays or Additional Studies Requirement: Prolonged review timelines increase cash burn risks without revenue inflows.

- Litigation Risk Post-SunRIZE Disclosure: Following unmet endpoints announcements, investigatory actions from plaintiffs' firms targeting securities laws violations pose distraction and potential liability ([S13]).

- Revenue Visibility: Absence of any currently approved products means financial sustainability depends entirely on capital availability until commercialization potential materializes.

These factors coalesce into typical biotech execution hazards compounded by recent operational setbacks requiring strategic agility.

Upcoming Milestones and Catalysts to Monitor

Market participants should track several near-to-medium term events expected to shape Rezolute’s trajectory:

- Final Readouts From Modified upLIFT Trial: Completion dates for updated protocol results will provide essential clarity on therapeutic viability under revised designs ([S3], [N1]).

- FDA Decision Timelines For Supplemental Dataset Review: Explicit regulatory feedback windows will act as key inflection points determining approval feasibility versus further study demands.

- Partnership Announcements or Licensing Deals: Should occur if Rezolute seeks external funding sources or commercialization allies in light of increased development risks ([S4]).

- Financing Activities: Given ongoing capital needs absent revenue streams, observing capital market maneuvers such as equity raises informs financial runway considerations ([S3]).

Concerted focus around these milestones offers a practical lens through which operational execution quality can be appraised objectively.

Financial Snapshot: Liquidity Supports Near-Term Development

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $11.24mm | |

| 2026-03-31 | ||

| Current assets | $122.05mm | |

| 2026-03-31 | ||

| Current liabilities | $7.70mm | |

| 2026-03-31 | ||

| Current ratio | 15.84x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Despite sizable operating losses reported previously (operating income loss $79.9 million as of mid-2025 [F1]), Rezolute maintains a healthy liquidity buffer facilitating ongoing R&D investments. Key balance sheet metrics as of March 31, 2026 ([F1]) highlight:

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | $11.24 million | |

| 2026-03-31 | ||

| Current Assets | $122.05 million | |

| 2026-03-31 | ||

| Current Liabilities | $7.70 million | |

| 2026-03-31 |

The resulting current ratio roughly stands at 15.8x, indicative of strong short-term financial health supporting clinical operations without immediate liquidity concerns.

This analysis summarizes public disclosures without providing investment advice or price opinions. It emphasizes operational fundamentals grounded in recent SEC filings and market data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments