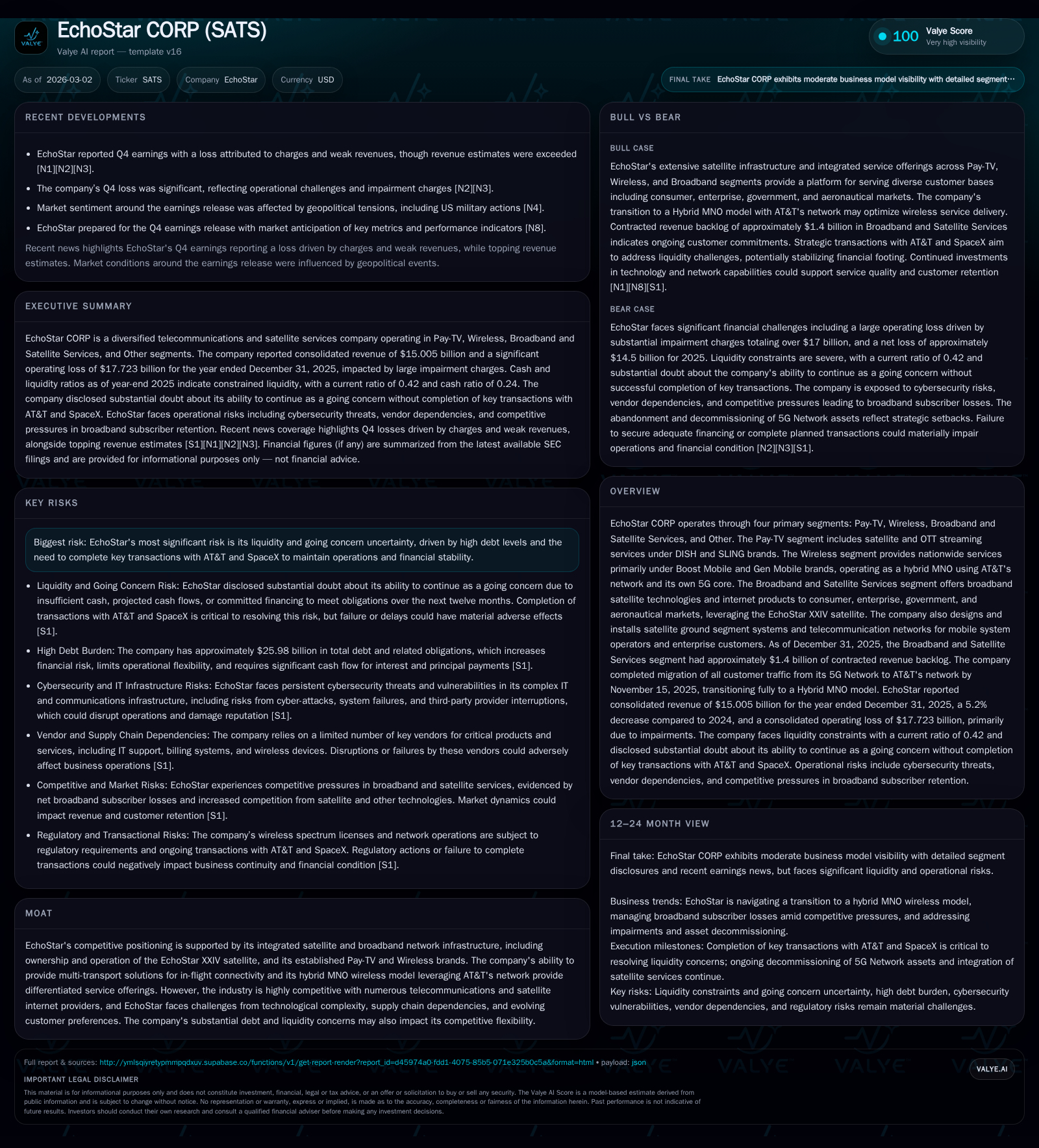

EchoStar's Massive Losses and Liquidity Risks Constrain Growth Despite Strategic Satellite Assets

EchoStar confronts severe financial headwinds and operational shifts amid a competitive satellite and wireless services market.

EchoStar CORPORATION reported substantial operating losses in its FY2025 results, driven by impairments and strategic restructuring following major transactions with AT&T and SpaceX. The company’s core segments—Pay-TV, Wireless, and Broadband and Satellite Services—face fierce competition and technological challenges, constraining revenue growth prospects. Liquidity and going concern issues loom large due to high debt levels and negative cash flows, despite a $1.4 billion contracted backlog in their Broadband segment. Capital allocation remains cautious with modest buybacks and no dividends reaffirmed as liquidity concerns persist.

Historical Performance

EchoStar CORP's financial trajectory through the past four years highlights dramatic variability culminating in severe losses for FY2025. Total revenue for FY2025 was approximately $1.3 billion [F1], showing minimal growth compared to prior years, yet masking underlying operational challenges.

Operating income deteriorated sharply from a loss of approximately $304 million in FY2024 to an unprecedented -$17.7 billion in FY2025 [F1]. This plunge is primarily attributable to massive non-cash impairment charges related to the abandonment of parts of EchoStar's proprietary 5G Network following regulatory and strategic transactions with AT&T and SpaceX [S11][S26].

Net income mirrored this steep decline, producing an FY2025 loss nearing $14.5 billion after being only modestly negative in earlier periods [F1]. Operating cash flow also turned negative (-$99 million) for the first time since FY2022, while capital expenditures remained high at almost $966 million as the company continued to invest in satellite infrastructure and network maintenance [F1][S11].

Historical performance (annual)

| FY | CFO ($bn) | OpInc ($bn) | Capex ($bn) |

|---|---|---|---|

| 2025 | -0.1 | -17.7 | 1.0 |

| 2024 | 1.3 | -0.3 | 1.5 |

| 2023 | 2.4 | -0.9 | 3.1 |

| 2022 | 0.5 | 0.2 | 0.3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 49 | -1065 |

| 2024 | 89 | -292 |

| 2023 | 89 | -668 |

| 2022 | 89 | 204 |

Source: SEC companyfacts cache [F1].

Note: Revenue reported pertains predominantly to Broadband and Satellite Services as other segments have undergone reorganization during these years.

Business Segments Overview

EchoStar operates across four main segments: Pay-TV, Wireless, Broadband and Satellite Services (BSS), and Other [S13].

Pay-TV encompasses traditional satellite TV services under DISH® and SLING® brands, delivering both DBS-based satellite TV as well as OTT streaming via SLING TV aimed at cost-conscious consumers seeking alternatives to cable.

Wireless offers nationwide mobile connectivity primarily through Boost Mobile® and Gen Mobile® brands. Transitioning from an MVNO model leveraging multiple host networks, EchoStar moved to a hybrid MNO approach using AT&T's cellular spectrum post-November 2025 [S13][N1]. As part of this pivot, the company ceased customer traffic on its independent 5G Network after FCC-mandated spectrum sales tied to the AT&T Transactions [S13][S19].

Broadband & Satellite Services is anchored by the EchoStar XXIV satellite providing broadband internet products for consumer (residential SMBs), enterprise, government, and aeronautical sectors. This unit benefits from hardware manufacturing capabilities including gateways and terminals deployed for other satellite customers [S6]. Contracted backlog at December 31, 2025 stood at approximately $1.4 billion for this segment alone—a significant forward revenue indicator amidst a challenging market [S6].

Other includes legacy infrastructure primarily linked to the redundant portions of its former 5G deployment which are now being decommissioned post-SpaceX deal [N1][S13].

Future Growth Prospects

Growth trajectories for EchoStar hinge largely on successfully leveraging its satellite capacity via BSS offerings amid intensifying competition from other satellite internet providers (e.g., ViaSat Communications owned by Viasat/Exede) as well as rollout of hybrid wireless services utilizing partner networks [S6][S13].

The company's Pivot toward a hybrid MNO wireless model aims to reduce capex intensity while capitalizing on its proprietary core network capabilities combined with AT&T’s expansive radio access network coverage [N1][S13]. However, relinquishing control over last-mile network assets increases reliance on partner agreements subject to renegotiation risks.

On the Pay-TV front, EchoStar’s position within conventional DBS satellite delivery faces secular subscriber declines caused by cord-cutting trends benefiting OTT streamers; SLING TV attempts partial mitigation but operates in crowded OTT markets requiring aggressive pricing and content investments [S13][N2].

Satellite broadband ambitions depend critically on newly launched satellites like EchoStar XXIV maintaining operational excellence amid weather risks, spectrum coordination challenges requiring regulatory approvals internationally, and potential interference concerns given evolving FCC policies on spectrum sharing [S9][S20]. New technological standards such as LEO constellation internet challenge geostationary players like EchoStar but also open partnership opportunities.

Forecasts, Milestones & What To Watch (Analysis)

Explicit forward guidance is not provided; key milestones include monitoring:

- The execution success of remaining AT&T Transactions and SpaceX Transactions which underpin liquidity improvement plans by divesting legacy assets [S24].

- Progress in subscriber net additions or reductions within BSS broadband service amid competitive pressures.

- Further impairments or capital write-downs tied to phased-out network elements impacting earnings volatility.

- Regulatory developments affecting spectrum usage rights impacting wireless segment strategies.

- Backlog realization pace into actual revenues signaling sustainability of enterprise contracts.

Returns & Capital Allocation

ROE suffers deeply from the immense net losses recorded; approximated at -251% using FY2025 net income against equity base [$5.77 billion] suggesting value destruction rather than creation currently [F1]. Ongoing capital expenditures remain substantial reflecting continuous investment in core infrastructure albeit lowered from prior peak levels indicating recalibrated investment pacing [F1][S11].

Cash flow remains strained with free cash flow negative exceeding one billion dollars when subtracting capex from operating cash flow [-$99 million minus $966 million] highlighting cash burn risk [F1]. Liquidity concerns echoed by management manifest through a current ratio of only 0.42 given current liabilities vastly exceed current assets [F1], underscoring short-term solvency stress.

Dividend payments have been suspended reflecting need to conserve liquidity; share repurchases continue moderately with approximately $48 million spent in FY2025 versus prior authorization to repurchase up to $2 billion of common stock through end-2026 which exhibits management intent but practical restraint amidst financial uncertainty [S4][F1].

Competitive Position & Risks

EchoStar’s integrated satellite asset base including ownership of EchoStar XXIV alongside branded Pay-TV (DISH/SLING) user bases provide differentiated market positioning not easily replicated by smaller competitors . However, entrenched competition arises from numerous telecommunications entities offering terrestrial broadband solutions (fiber optic, cable), alternative satellite ISPs leveraging newer LEO constellations, plus strong OTT streaming services creating churn risks for Pay-TV units [S6].

Risks extend beyond competition with significant exposure to environmental disruptions that can damage satellites or ground infrastructure given extreme weather events reported by management as increasingly frequent operational hazards entailing potentially large costs for mitigation or repair [S9]. Supply chains for critical wireless devices face instability due to geopolitical trade policy shifts leading to increased costs or delays impacting subscriber acquisition campaigns particularly in wireless segment buildouts [S17].[Refined sourcing strategy remains essential.] Cybersecurity threats represent ongoing operational vulnerabilities including risk of system outages or data breaches affecting customer trust and compliance requirements across jurisdictions where EchoStar operates internationally [S20].

Liquidity constraints pose material risks; management acknowledges going concern uncertainties due primarily to high leverage levels compounded by weak cash generation capacity necessitating timely completion of asset sale transactions (AT&T/SPACEX deals) or risk prolongation of financial distress possibly culminating in restructuring actions [S24][N12]. Debt covenants restrict financial flexibility further constraining capital allocation decisions under adverse market conditions [S18].[Such debt servicing risks elevate credit costs impacting all activities.]

Conclusion

EchoStar stands at a crossroads complicated by massive asset impairments destabilizing earnings visibility despite underlying backbone assets represented by satellite infrastructure backlog valued at $1.4 billion. Strategic shifts such as transition to hybrid wireless model reflect adaptation attempts constrained by regulatory mandates necessitating divestitures while competitive landscapes exert revenue pressure across all segments.

Liquidity remains paramount challenge shaping cautious capital deployment marked by curtailed buybacks and null dividends reinforcing focus on survival rather than expansion currently. Performance recovery hinges heavily on successfully executing planned transactions with AT&T/SpaceX entities alongside stabilizing subscriber bases within broadband and pay-TV lines amidst intensifying competition.

A watchful eye should be kept on transaction outcomes alongside operational metrics particularly subscriber trends within Wireless and Broadband segments that will ultimately determine whether EchoStar can leverage its technological moat effectively or see continued value erosion under prevailing market pressures.

This analysis is based solely on publicly available data as of early March 2026 including SEC filings and reported earnings transcripts without prediction or recommendation regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments