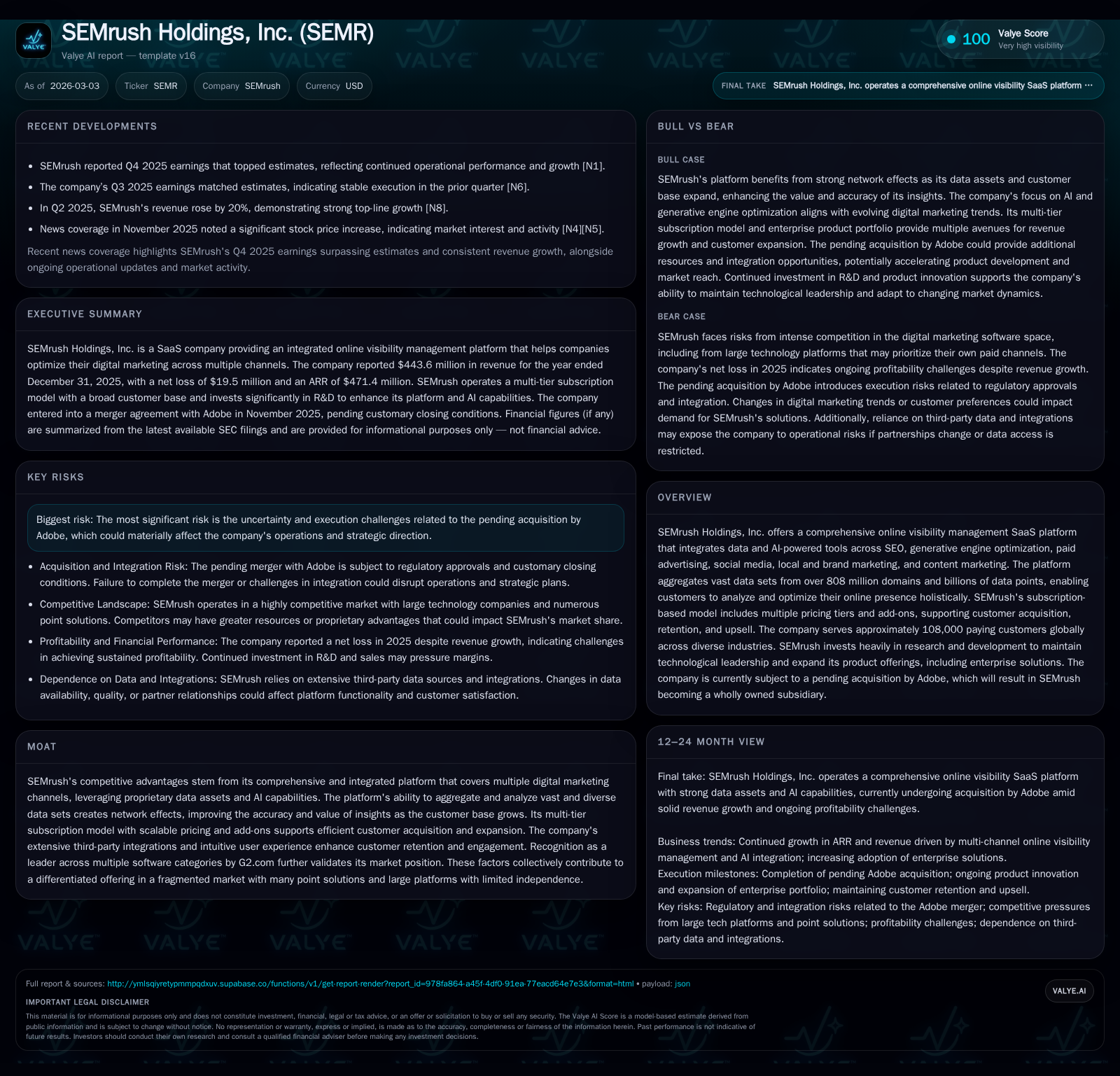

SEMrush Holdings’ Renewed Growth and Acquisition Outlook for 2026

Evaluating SEMrush's financial rebound in 2025, platform evolution, and strategic trajectory as it approaches acquisition by Adobe.

SEMrush Holdings returned to robust operating cash flow in 2025 despite reporting net losses driven by elevated R&D and stock compensation expenses. The company's multi-tier SaaS platform, integrating SEO, AI-driven generative engine optimization, and multi-channel marketing tools, supports a diverse global customer base of approximately 108,000 paying users. Its go-to-market approach effectively balances product-led growth with sales-assisted and sales-led motions tailored to varied buyer segments. The pending all-cash acquisition by Adobe at $12 per share introduces execution risks but underscores SEMrush’s strategic value. Key milestones to monitor include regulatory approvals, integration progress, and post-merger platform positioning amid intensifying competition.

Financial Rebound and Operating Performance in 2025

SEMrush Holdings posted a marked improvement in its operating activities in fiscal year 2025 while continuing to navigate profitability challenges reflecting heavy reinvestment into its business. Full-year revenue reached approximately $443.6 million — an 18% increase over the $376.8 million generated in 2024 — underscoring robust subscription growth across its SaaS offerings [F1][S1]. Despite this top-line expansion, operating income swung sharply negative to a loss of $22.8 million compared to an $8.3 million profit a year earlier [F1]. This reversal was largely driven by a substantial increase in non-cash stock-based compensation expenses totaling $52.6 million alongside elevated R&D spending aimed at accelerating innovation [S1][F1].

Net income mirrored this trend, declining from a positive $7.4 million in 2024 to a negative $19.0 million in 2025 [F1]. However, the operating cash flow (CFO) generation vividly illustrated underlying business strength; SEMrush produced $59.6 million of CFO during the year — up nearly 27% year-over-year — fueled by improved collection cycles, deferred revenue growth (+$21.9 million), and operational efficiencies [F1][S1]. Capital expenditures fell sharply year-over-year (down ~53%) to just under $1.8 million as the company optimized capital usage amid piling investments in software development capitalized as intangible assets [F1][S14].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | 60 | -23 | 2 | -330.2% |

| 2024 | 8 | 47 | 8 | 4 | +766.9% |

| 2023 | 1 | 8 | -8 | 2 | +102.8% |

| 2022 | -34 | -10 | -36 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 58 | -6.6 |

| 2024 | 43 | 3.2 |

| 2023 | 6 | 0.4 |

| 2022 | -14 | -16.9 |

Source: SEC companyfacts cache [F1].

Note: All figures represent consolidated amounts for SEMrush Holdings, Inc.

These data illustrate that while SEMrush continues to invest aggressively—particularly in R&D—it has established a solid free cash flow foundation that supports ongoing product development without immediate reliance on external capital.

Subscription Tiers and Multi-Channel SaaS Platform as Core Growth Engines

SEMrush has evolved its online visibility management offering into a comprehensive SaaS platform integrating distinct hubs focused on SEO, generative engine optimization (GEO), paid advertising management, social media marketing (SMM), local marketing, brand development, and content marketing—all powered by extensive proprietary datasets and AI analytics [S4][S6]. This breadth enables customers to analyze cross-channel interplay often absent from siloed digital tools.

Commercially, the company employs sophisticated tiered subscription models tailored both vertically and horizontally:

- Starter / Pro+ / Advanced tiers under the flagship Semrush One umbrella optimize accessibility by offering escalating limits on website counts, keywords tracked including AI prompt tracking for conversational engines like ChatGPT or Gemini, technical site reporting features, historical SEO data access, device/location tracking expansions and content workflow integrations [S20].

- Legacy SEO-focused tiers (Pro, Guru, Business) remain available with granular feature add-ons such as keyword tracking extensions or brand insights modules.

- The Enterprise SEO portfolio features multi-level Bronze through Platinum options complemented by specialized products like Enterprise AIO for deep LLM brand analysis and Enterprise Site Intelligence focusing on technical health metrics [S8][S20]. These solutions emphasize annual contractual commitments suited for larger customers with high license volume demands.

Leveraging these structures supports scalable pricing outcomes while enabling tailored client experiences that underpin unit-level economics like customer lifetime value (LTV). On this front SEMrush reported a notable increase in average ARR per paying customer from $3,522 at end-2024 to $4,369 by end-2025—a direct reflection of effective upsell strategies around new artificial intelligence modules and threading disparate marketing channels into unified workflows [S11][S13].

Underlying the technological advantage is an extensive proprietary data ecosystem consisting of more than 808 million domains crawled daily, billions of keywords tracked globally along with trillions of backlinks processed continuously alongside emerging large language model interaction datasets (~200 million prompts) sourced both algorithmically via crawlers and from third-party APIs covering Google Ads through TikTok ads as well as Salesforce CRM integration [S12][S17]. Such scale underpins discernible network effects yielding increasingly precise insights as the customer base expands.

Customer Segmentation and Go-To-Market Strategies Driving Expansion

SEMrush’s go-to-market (GTM) approach deftly blends three core motions designed for efficiency across diverse segments ([S5][S9]):

Product-Led Growth (PLG): A foundational low-touch motion focused on automated self-service adoption supported through broad organic visibility generated by content marketing efforts plus educational initiatives like Semrush Academy which boasts over 1.4 million enrollees with roughly 600k certifications issued—an organic funnel feeder enhancing brand credibility at scale [S5]. This motion benefits from low customer acquisition costs (CAC) enabled by freemium trials transitioning seamlessly into paid subscriptions.

Sales-Assisted Motion: Targets mid-market SMBs with more complex needs by layering personalized outreach post-adoption leveraging account managers who drive feature adoption and upsell against add-ons or higher tiers while ensuring onboarding success via dedicated customer success teams providing training which boosts net dollar retention rates (~106%) through churn mitigation tactics [S9].

Sales-Led Motion: Reserved for sophisticated enterprise customers requiring tailored demonstrations involving discovery phases to diagnose business pains followed by technical deep dives before contract negotiation focusing on bespoke pricing models often anchored around master subscription agreements facilitating streamlined renewals plus expansive cross-sell [S9]. This segment saw departmental headcount expand roughly 8% year-over-year signaling strategic emphasis.

Additionally introduced channel-led initiatives engaging select agency partners broaden reach through referrals creating multiplier effects further reducing CAC [S5]. Collectively these motions harmonize efficiency scalable growth with tailored service levels consistent with customer sophistication profiles.

Capital Allocation, Cash Flow Generation, and Return on Equity Analysis

Capital discipline remains evident even amid pronounced reinvestment rhythms targeting long-term platform leadership:

- Operating cash flows delivered solidly positive free cash flow approximating $57.8 million for FY25 after minimal capex ($1.79 million), demonstrating scalable economics despite reported accounting net losses primarily influenced by non-cash equity comp charges [$59.6M CFO minus $1.79M capex = ~$57.8M FCF] [F1][S26][S14].

- Return on equity stands modestly negative at approximately -6.6%, reflecting net losses relative to expanded shareholders’ equity which rose from approximately $256.6 million at end-2024 to about $288.6 million by end-2025 sustained through retained investment accruals rather than dividends or buybacks given dividend absence confirmed in disclosures [F1][S26][S15].

- Liquidity remains healthy with more than two times current assets over current liabilities ($324M/$154M), bolstered principally by cash reserves exceeding $264 million—a strong balance sheet buffer ahead of merger closure [F1][S23].

Notably stock-based compensation expenses weigh heavily but align closely with talent retention tradeoffs critical for sustaining innovation capacity particularly across multinational R&D hubs situated predominantly across Europe (Prague, Limassol Cyprus among others) where salaries blend favorable cost structures combined with required skills sets important for advanced AI algorithm development initiatives [S14][S21].

Risks and Uncertainties Surrounding the Adobe Acquisition

The pending Adobe acquisition approved between parties on November 18th, 2025 represents a pivotal near-term event embedding both transformative upside potential alongside execution risks [S1][S3]:

- At the effective time of merger anticipated post requisite regulatory approvals the transaction contemplates each SEMrush share converting into an all-cash payment of $12 without interest — an attractive premium vis-à-vis recent trading but locking shareholders out of any future standalone upside [S1][N1]. Equity awards are bifurcated whereby vested options are cashed out while unvested ones morph into Adobe RSU equivalents maintaining retention incentives aligned with post-close corporate objectives.

- Legal contingencies arise from class action lawsuits linked to SEMrush’s recently completed repurchase program which injects uncertainty around contingent liabilities although management currently views these risks as immaterial relative to overall financial condition [S24].

- Integration complexity looms large considering SEMrush’s independent brand positioning juxtaposed against Adobe’s broader enterprise marketing cloud ecosystem; potential strategic shifts could alter existing product roadmaps or channel strategies which hitherto drove efficient CAC/LTV dynamics [S3][N1].

- Maintaining momentum behind AI-driven enhancements while transitioning organizational cultural attributes will be essential to preserve competitive differentiation during ownership transition.

What to Watch: Post-Acquisition Integration and Market Positioning

Investors should closely monitor early developments surrounding:

- Receipt of antitrust clearances from relevant jurisdictions permitting deal close; intricacies here could affect timing materially.

- Arduino signals around roadmap realignment including how Semrush One's integrated visibility intelligence is positioned against Adobe Experience Cloud offerings—synergies may unlock deeper cross-selling or risk overlap prompting rationalization.

- Customer retention rates post-merger especially within enterprise tiers sensitive to changes in support models or pricing frameworks; any material churn uptick would undermine core recurring revenue bases.

- Continued R&D funding commitment given that SEMrush historically invested heavily ($97+ million annually on research & development) enabling ongoing feature launches central to competitive moat upkeep amid rapid digital marketing technology evolution [S14].[N1]

- Competitive positioning vis-à-vis large incumbents such as Google’s Marketing Platform or Meta’s suite where independence traditionally allowed unbiased channel-neutral insights but scale limitations constrain breadth relative to fully integrated platforms.

- Litigation developments associated with repurchase-related claims; legal outcomes could influence both reputational risk profiles and contingent payout obligations influencing net income trajectory beyond merger consummation date.

This analysis synthesizes information extracted principally from SEC filings dated March 2nd, 2026 ([F1],[S1]-[S29]) supplemented by recent Nasdaq reportage ([N1]). It distills key evidentiary facts without speculative extrapolations or investment recommendations consistent with Valye News standards.

All financial figures are presented in US dollars unless otherwise noted.

--- Disclaimer --- This memorandum is prepared solely for informational purposes based on publicly available information as of early March 2026 pertaining to Semrush Holdings, Inc., its industry context, recent performance metrics, pending acquisition events and operational details disclosed therein; no investment advice or price forecasts are offered herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments