Shoulder Innovations Advances Surgical Ecosystem While Managing Growth Challenges

The latest quarterly update highlights strategic investments in product innovation and surgeon support that underpin market adoption amid elevated operating costs.

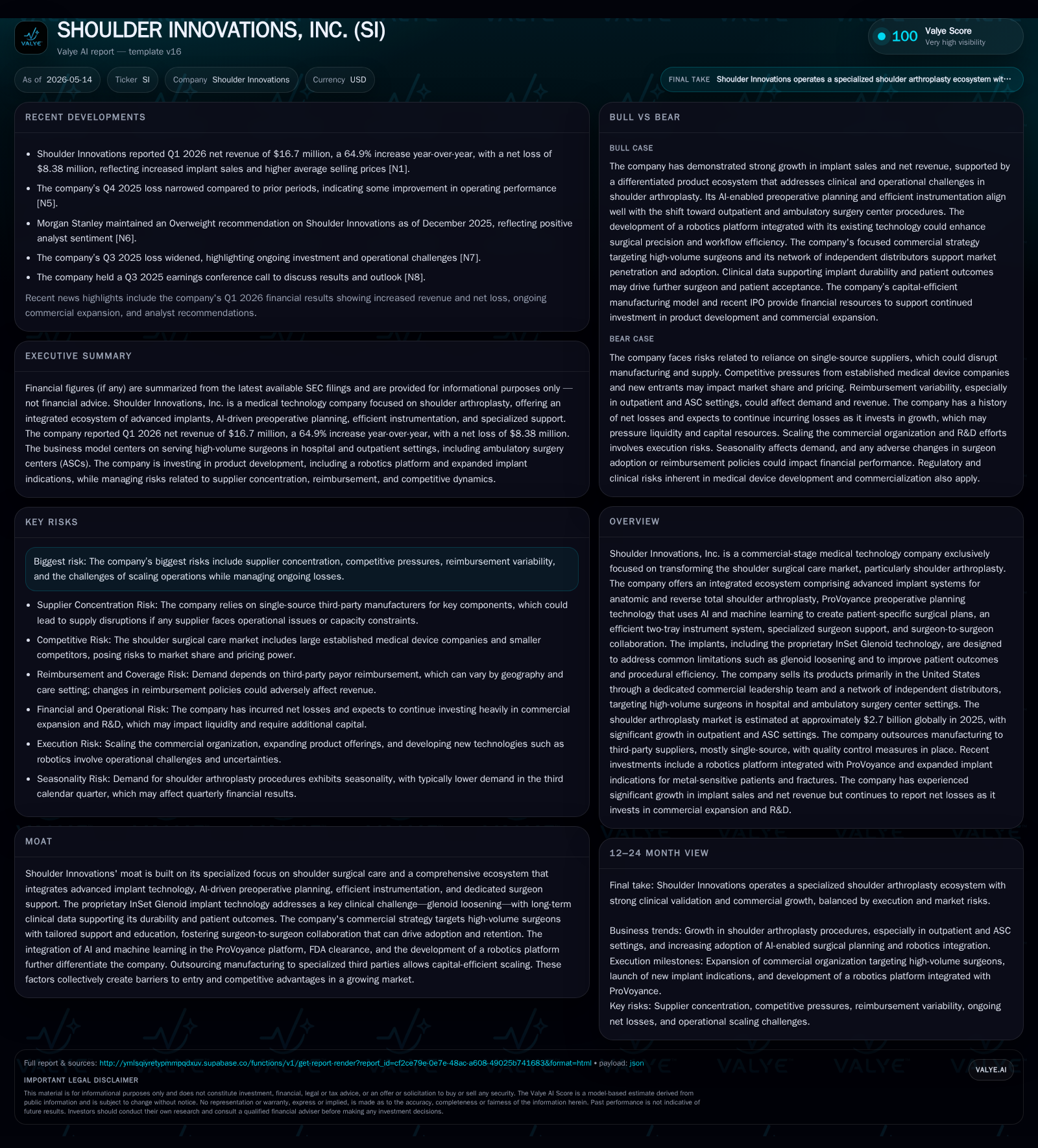

Shoulder Innovations, Inc. reported continued growth in implant system sales, supported by its advanced shoulder arthroplasty ecosystem integrating AI-driven planning and proprietary implant technologies. The May 2026 quarterly filing details rising operational expenses driven by expanded R&D and commercialization efforts, which weigh on near-term profitability but are viewed as critical for long-term success. The company’s outsourcing manufacturing model aids capital-efficient scaling, while its focused commercial strategy targets high-volume surgeons in hospitals and ASCs. Going forward, the company faces risks from supplier concentration, reimbursement dynamics, and operational scale-up complexities amid ongoing losses.

Latest Quarterly Operating Update: Progress Amid Elevated Costs

In the first quarter of 2026 ended March 31, Shoulder Innovations reinforced its strategic commitment to expanding its shoulder surgical ecosystem even as near-term operating results reflect mounting costs. The company reported ongoing research and development expenditures intended to extend its platform capabilities and advance new product offerings. While these activities increased expenses notably compared to prior periods — with R&D spending rising to support new implants and software features — gross margins remained stable despite scaled revenues and associated cost of goods sold increases [S2].

Operating expenses grew primarily in selling, general & administrative (SG&A) categories reflecting expanded marketing initiatives, personnel costs including commissions and bonuses, medical education programs targeting surgeons, and public company compliance costs. Management emphasized that although these elevated expenses depress short-term profitability metrics — net loss widened alongside a roughly 90% increase in cash use from operations year over year — they are viewed as necessary investments to secure longer-term market penetration through surgeon adoption and a robust commercial presence [S2,N1].

Recent event disclosures reiterate the foundational role of clinical data dissemination and surgeon education within their commercial approach along with iterative product improvements aimed at both clinical efficacy and procedural efficiency gains [S3]. This thematic continuity aligns with management’s intent to progressively drive ecosystem adoption across hospital and ambulatory surgery center (ASC) venues.

Integrated Business Model and Product Ecosystem

Shoulder Innovations pursues a highly specialized business model concentrating exclusively on shoulder arthroplasty solutions within the broader orthopedics landscape. Its integrated ecosystem comprises several interdependent components designed around addressing core surgical challenges — such as glenoid loosening — while enhancing surgeon workflow.

At the center are advanced implant systems for anatomic total shoulder arthroplasty (aTSA) and reverse total shoulder arthroplasty (rTSA), featuring proprietary components like the InSet Glenoid implant technology which is clinically validated to improve fixation stability and longevity. Complementing implants is the ProVoyance preoperative planning platform that leverages artificial intelligence (AI) and machine learning to generate patient-specific surgical plans that optimize implant positioning prior to surgery.

To facilitate procedural efficiency, the company developed an efficient two-tray instrument system simplifying logistics in the operating room. Additionally, Shoulder Innovations supports surgeons through dedicated commercial leadership teams coupled with a Customer Experience and Medical Education (CEME) group fostering continuous surgeon-to-surgeon collaboration — effectively creating a feedback loop that accelerates adoption velocity.

Manufacturing is outsourced to specialized third-party providers enabling flexible scaling aligned with demand without heavy capital expenditure commitments in production infrastructure. This ensures capital efficiency amidst volume expansion efforts.

Competitive Dynamics and Industry Structure

The U.S. shoulder arthroplasty market is sizeable—estimated at approximately $1.7 billion in 2025—with an annualized growth rate projection of around 11% through 2029 driven largely by demographic demand for joint reconstruction therapies [S1]. Around 250,000 procedures were performed domestically in 2025.

Key industry players range from large diversified orthopedic device manufacturers offering multi-joint portfolios to focused innovators like Shoulder Innovations specializing solely in shoulder solutions. The company’s moat centers on clinical differentiation through proprietary implant designs supported by long-term outcome data addressing frequent failure modes such as glenoid component loosening.

Clinically relevant innovation combined with efficient user workflow enhancement tools creates switching costs for high-volume shoulder surgeons who represent the primary customer segment targeted by a mix of direct sales teams and independent distributor channels.

An important structural shift influencing competitive positioning is the rise of ambulatory surgery centers (ASCs), which have emerged as cost-effective care settings relative to hospitals traditionally burdened by capacity constraints. Shoulder Innovations has strategically aligned its commercial efforts towards this trend by tailoring support resources for surgeons practicing across both hospital-based ORs and ASCs.

Price sensitivity remains moderated somewhat by strong clinical validation; however reimbursement variability inherent in U.S. healthcare poses ongoing challenges impacting realized pricing power.

Drivers of Growth: Adoption, Innovation, and ASC Surge

Several measurable factors underpin Shoulder Innovations’ growth trajectory:

- A reported >50% increase in procedure volume from calendar year 2024 through 2025 evidences rapid adoption momentum fueled by expanding commercial reach [S1].

- The proliferation of ASCs due to hospital capacity limitations catalyzes demand migration benefiting the company’s specialized ecosystem optimized for such outpatient settings.

- Clinical evidence supporting implant durability coupled with real-world surgeon testimonials promotes confidence driving broader trials among late adopters.

- Advances in AI-driven preoperative planning via ProVoyance enhance case predictability reducing intraoperative uncertainty which improves surgeon experience.

- Product enhancements such as streamlined instrumentation reduce OR time burden—a key concern among surgical teams—further elevating technology appeal.

Together these elements create a commercial flywheel effect whereby increasing surgeon satisfaction drives repeat usage within existing customers while stimulating net new account penetration [S2,N1].

Potential Challenges and Risk Factors

Despite encouraging growth dynamics substantial risks merit continuous scrutiny:

- Reliance on third-party manufacturers concentrates supply chain exposure potentially affecting production timelines or cost structures if disruptions occur [S5].

- Macro health insurance policy changes or downward pressure on reimbursement rates may constrain pricing flexibility or procedure volumes adversely impacting revenue streams [S23].

- Competitive landscape includes large incumbents capable of leveraging broader portfolio advantages or aggressive pricing strategies presenting ongoing threats.

- Extensive regulatory compliance requirements impose operational burdens; failure to satisfy FDA quality regulations or health care fraud statutes could result in sanctions altering market access [S15,S22].

- Operational scale-up incurs elevated R&D spending plus onboarding costs within sales force increasing cash burn levels; execution risk exists if absorption rates do not meet forecasted trajectories leading to financing needs that might dilute equity holders or increase leverage [S2,S24].

Key Upcoming Catalysts and Monitoring Points

Investors should track several milestones indicative of future performance:

- Release of further clinical data reinforcing InSet Glenoid performance benchmarks that may widen competitive gaps.

- FDA clearances or approvals advancing robotics integration within their procedural platform expanding technological differentiation.

- Quarterly revenue releases versus consensus expectations signaling whether adoption trends continue accelerating particularly within ASC settings.

- Updates on commercial scaling initiatives including new hires or expanded distributor agreements reflecting go-to-market efficiency.

- Any potential capital raising activity that could impact financial structure or shareholder dilution metrics given ongoing investment demands [S2,S3,N1].

Financial Snapshot and Capital Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $11mm | |

| 2026-03-31 | ||

| Total debt | $15mm | |

| 2026-03-31 | ||

| Net debt | $3mm | |

| 2026-03-31 | ||

| Current assets | $146mm | |

| 2026-03-31 | ||

| Current liabilities | $12mm | |

| 2026-03-31 | ||

| Current ratio | 11.81x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

A review of financial metrics as of March 31, 2026 underscores the company's liquidity profile balanced against operating losses:

| Metric | Value (USD millions) |

|---|---|

| Cash & Equivalents | 11.49 |

| Total Debt | 14.96 |

| Net Debt | 3.47 |

| Current Assets | 145.78 |

| Current Liabilities | 12.34 |

| Current Ratio | 11.81 |

The company maintains approximately $11.5 million in cash equivalents alongside current assets totaling around $146 million against current liabilities near $12.3 million yielding a strong current ratio (~11.8), indicating ample near-term liquidity [F1]. Total debt stands at about $15 million with net debt after accounting for cash roughly $3.5 million.

Operating cash flow usage rose sharply—by over 90% year-over-year—to approximately $12.4 million during Q1 reflecting escalated operating expenses tied principally to R&D investments and expanded selling infrastructure consistent with stated strategic priorities [S2]. Financing activities contributed modest proceeds from common stock option exercises amounting to $0.1 million during Q1 contrasting with substantial convertible preferred stock issuances recorded in the prior year period reflecting less reliance currently on external equity capital raises.

This financial position provides runway for continued innovation investment; however sustained positive cash flows remain critical for long-term self-sufficiency without additional dilutive financing.

Shoulder Innovations exemplifies a focused medical technology innovator blending advanced shoulder implant engineering with digital surgical planning tools within an integrated ecosystem designed for procedure efficacy across care settings including rapidly growing ASCs. Its recent quarterly disclosures reveal a classic medtech growth balancing act between investing heavily in future-proofing platforms while managing near-term elevated costs that impact profitability metrics. Industry growth tailwinds are favorable but tempered by execution risks linked to scale-up demands plus inherent healthcare reimbursement uncertainties typical for specialty orthopedic devices.

Continued monitoring of surgical adoption patterns along with key regulatory milestones will provide essential insight into if—and how quickly—this promising ecosystem converts into sustainable long-term value creation amid competitive industry pressures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments