Silgan Holdings Strengthens Market Leadership Despite Custom Containers Headwinds

Q1 2026 results highlight a sales decline in custom containers amid continued strength in other segments, underscoring the company’s diversified packaging platform.

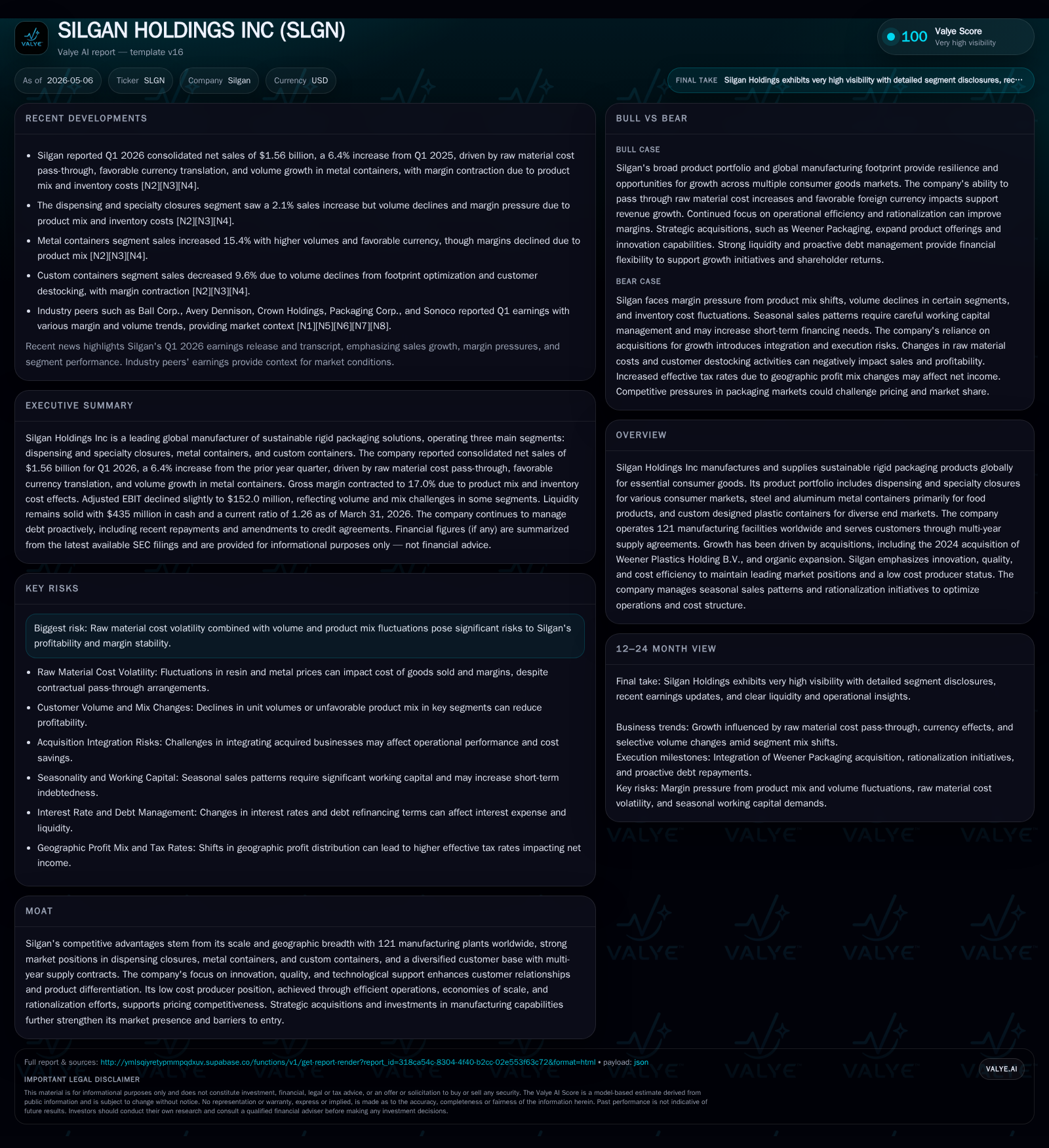

Silgan Holdings reported mixed first-quarter 2026 results with a 9.6% sales drop in its custom containers segment, primarily due to volume declines and customer destocking, while consolidated revenue grew 6.4% driven by gains in metal containers and dispensing closures. EBIT margins remained stable despite volume headwinds, supported by operational efficiency and cost rationalization efforts. The company's competitive advantages lie in its scale, diverse product portfolio, multi-year supply agreements, and recent acquisitions such as Weener Plastics, which bolster its innovation and market reach. Risks include raw material cost volatility and product mix fluctuations. Upcoming milestones include monitoring management guidance on volume recovery and execution of rationalization initiatives.

Q1 2026 Operating Update: Segment-Level Trends and Margins

Silgan Holdings’ latest quarterly filing for Q1 2026 reveals important dynamics shaping its near-term performance [S2]. Consolidated net sales climbed 6.4% year-over-year to $1.56 billion, primarily due to stronger revenues from the metal containers and dispensing specialty closures segments. However, the custom containers segment encountered a notable contraction with net sales falling by $16.1 million or approximately 9.6% compared to Q1 2025.

This decline in custom containers was attributable mainly to an estimated volume reduction of about 11%, reflecting the impact of the company’s prior footprint optimization initiatives which included exiting lower-margin business lines. Additionally, customer destocking activity during the quarter further pressured shipped volumes. Favorable foreign currency translation partly offset these volume headwinds by roughly $1 million [S2].

Despite this volume weakness, Silgan managed to preserve the EBIT margin for the custom container segment at 13.2%, with adjusted EBIT margin slightly compressing from 14.7% to 14.4%. The resilience is explained by strong cost controls and operational efficiencies realized through ongoing rationalization plans implemented over prior years [S2], [S1]. Adjusted EBIT fell modestly by $2.9 million due mainly to reduced volumes rather than deteriorating unit economics.

The other segments presented contrasting trends: metal containers grew robustly — net sales rose by approximately 15.4% driven by organic volume increases in pet food markets despite some softness in fruit and vegetable pack markets stemming from prior quarter prebuy activity; adjusted EBIT remained essentially flat but saw a margin decline from ~7.9% to ~6.9% due to a less favorable product mix [S2]. Dispensing closure sales also increased moderately with stable profitability levels [S1], [N4].

Overall consolidated EBIT margin softened slightly from prior year’s Q1 level (8.9% to about 8.1%), attributable largely to mix effects and raw material pass-through dynamics described later.

Silgan’s Business Model: Diverse Packaging Solutions Driving De-risked Revenues

Silgan Holdings specializes in manufacturing sustainable rigid packaging solutions that serve essential consumer goods markets globally [S1],[S2]. Its product segments include:

- Dispensing & Specialty Closures: Serving fragrance, beauty, food/beverage, personal care, home care, lawn/garden sectors.

- Metal Containers: Steel and aluminum cans primarily for pet/human food applications across North America and Europe.

- Custom Containers: Plastic containers designed for diverse end-markets including pharmaceuticals, consumer health, pet food, automotive components.

This multi-product portfolio delivers revenue diversification across multiple industries supported by long-term customer supply contracts enhancing stability [S1]. Product quality combined with focused technological innovation—both in mold design for closures and specialized container engineering—drive customer loyalty.

Revenue mechanics vary by segment:

- Dispensing closures rely on high unit volumes with value-driven upgrades in functional features supporting steady pricing power.

- Metal container revenues depend on raw material-linked pricing mechanisms with periodic adjustments tied to commodity input costs passed through to customers.

- Custom containers exhibit sensitivity to customer project pipelines as volumes can be lumpy; prices reflect complexity and customization premiums.

A hallmark of Silgan’s profitability is its status as a low-cost producer attained through economies of scale across an expansive manufacturing base of over 120 plants worldwide [S1]. Rationalization initiatives have improved fixed cost absorption rates without sacrificing flexibility critical for handling diverse product runs [S14].

Industry Dynamics: Competitive Footprint, Scale Advantages, and Regulatory Context

Within global rigid packaging markets—characterized by fragmentation especially in custom plastic containers—Silgan stands out due to its breadth of operations spanning multiple continents coupled with deep penetration in core categories [S1],[N5],[N6],[N7]. The scale positions it uniquely against both regional specialty players and multinational conglomerates.

Barriers to entry remain high given capital intensity of manufacturing equipment (e.g., injection molding machines for plastics or specialized stamping/lining presses for metal cans) combined with stringent hygiene/quality standards demanded by food/pharmaceutical customers.

Supply chain pressures are acute on raw materials like resins for plastics and steel/aluminum commodities—volatility remains pronounced impacting gross margins unless efficiently pass-through mechanisms function effectively [S9],[N9]. Sustainability trends are reshaping industry expectations; Silgan's focus on sustainable packaging innovations addresses growing regulatory demands and consumer preferences favoring recyclability or biobased materials.

Customer switching costs derive from tooling investments tied to tailor-made closures or shaped containers along with qualification processes that mitigate risks of site changes [S10]. This supports pricing durability where innovation meets client-specific requirements.

Growth Drivers: Strategic Acquisitions, Innovation Focus, and Market Penetration

Silgan’s growth trajectory combines organic expansion with targeted acquisitions that complement its core competencies [S1],[N11]. Most notably:

- The October 2024 acquisition of Weener Plastics Holding B.V., a European leader in dispensing systems extended Silgan’s custom container portfolio significantly enhancing technological capabilities and European market access.

- Ongoing investments in operational footprint rationalization optimize capacity utilization while enabling cost savings ranging from mold standardization programs to plant consolidations completed recently that saved tens of millions annually [S14].

- Innovation pipeline developments include advanced dispensing closures integrating safety features aligned with evolving regulatory requirements along with lightweighting metal cans lowering raw material usage without sacrificing structural integrity.

- Geographic expansion targets emerging markets where rising consumer incomes fuel demand for packaged personal care or processed foods requiring sophisticated rigid packaging solutions.

These drivers underpin mid-single-digit compound annual growth potential while sustaining industry-leading adjusted EBIT margins supported by continuous manufacturing productivity enhancements.

Risks and Watchpoints: Raw Material Volatility, Volume Pressure, and Mix Challenges

Key risks identified include:

- Raw Material Price Fluctuations: Inputs such as aluminum, steel, polyethylene resins have historically volatile prices influencing gross margins; although strategic pass-through contracts mitigate some exposure [S2],[S9].

- Volume Uncertainty: The external demand environment especially impacts custom container volumes which dropped nearly 10% this quarter due partly to prior footprint exit decisions plus current customer inventory drawdowns [S2]. Sustained softness could pressure fixed costs spreading.

- Product Mix Effects: Less favorable product mix within metal containers segment led to EBIT margin compression despite higher unit volumes; similar mix shifts could limit margin expansion ahead if premium products face demand moderation [S2],[N9].

- Currency Exchange Fluctuations: Favorable FX helped offset some downside in Q1 yet remains a variable impacting reported results given global footprint.

- Operational Risks: Facility closures inherent in rationalization programs entail short-term charges with uncertain timing of full benefits realization; failure to execute efficiently may impede margin improvement plans [S14].

These risks require continued focus on procurement strategies balancing hedging efforts alongside flexible supply arrangements plus proactive new product introduction addressing changing market needs.

What Investors Should Monitor Next: Guidance and Execution Milestones

Upcoming factors warranting close attention include:

- Management commentary on expected trajectory for custom container volumes post-destocking quarters;

- Updates on cost savings progress related to facility rationalizations particularly within European metal closure operations;

- Seasonal patterns typical of fruit/vegetable packaging impacting metal container demand entering summer peak periods;

- Pricing actions or raw material cost recovery effectiveness amidst global commodity price volatility;

- Any announcements regarding further acquisition opportunities or disposition actions affecting portfolio mix;

- Quarterly earnings releases providing insights into adjusted EBIT margins' sustainability across all segments.

Tracking these indicators will provide useful directional cues on Silgan’s ability to leverage its competitive strengths amid business cycle fluctuations.

Financial Profile: Capital Structure, Liquidity, and Profitability Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $435mm | |

| 2026-03-31 | ||

| Current assets | $3.0bn | |

| 2026-03-31 | ||

| Current liabilities | $2.4bn | |

| 2026-03-31 | ||

| Current ratio | 1.26x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

At March 31, 2026 Silgan held cash and cash equivalents at approximately $435 million. Segmental profitability showed adjusted EBIT margins around:

- Dispensing & Specialty Closures: ~11%

- Metal Containers: ~7%

- Custom Containers: ~14% Total consolidated EBIT margin moderated modestly due mainly to mix effects but remains robust relative to peers [S2],[S7].

This financial sturdiness underpins Silgan's continued capacity for acquisition pursuit alongside shareholder return activities balanced against external market challenges.

This analysis is based on publicly available data up to May 6, 2026 ([S2], [S3], [S1], [F1]) without offering investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments