Soleno Therapeutics’ Profitability Turnaround Driven by VYKAT XR Commercial Launch and Debt Restructuring

Following FDA approval in early 2025, Soleno Therapeutics began commercializing its first product, generating positive operating income and net income for the year.

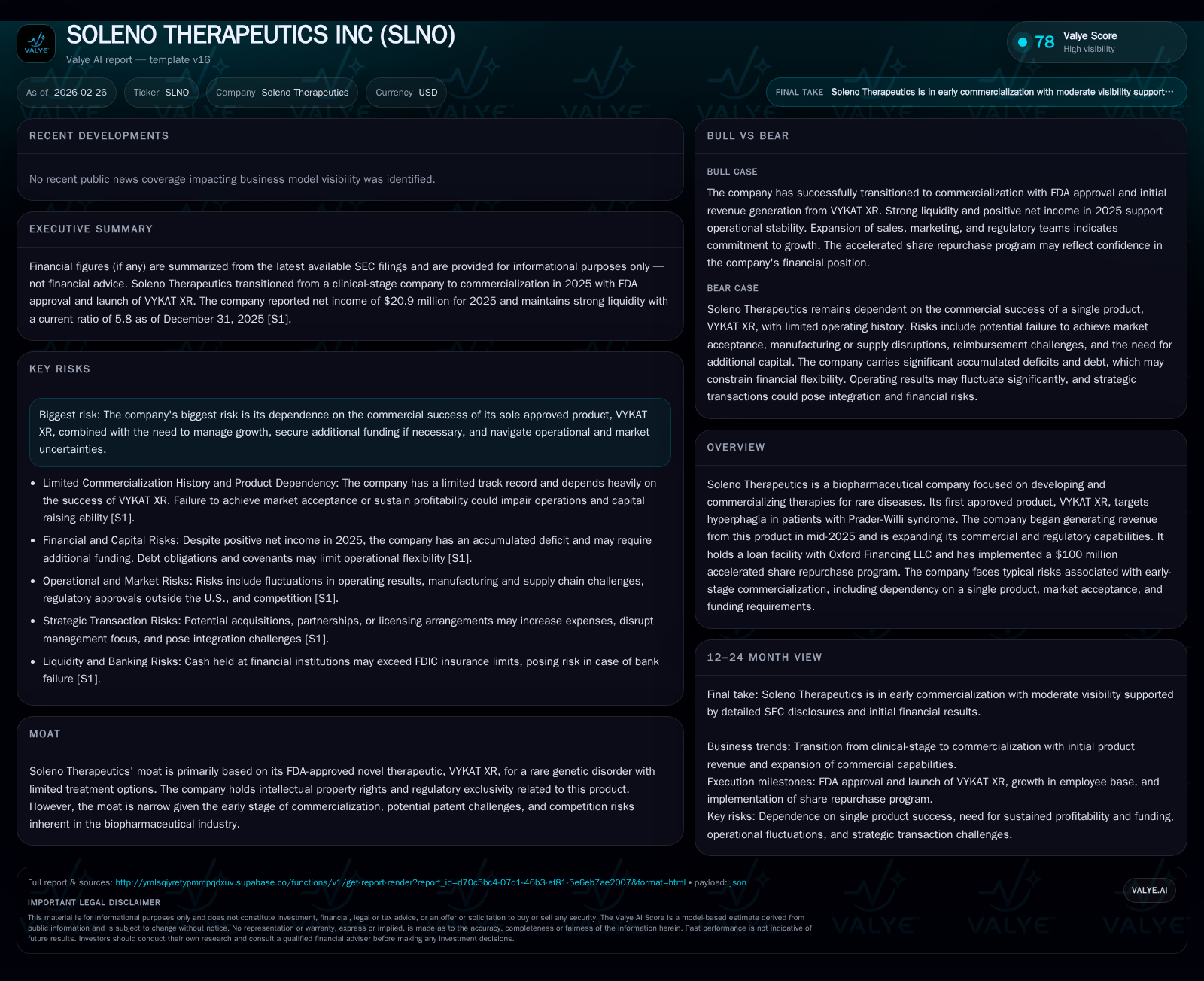

Soleno Therapeutics transitioned from a clinical-stage company with persistent losses into profitability in 2025, driven by revenue from its FDA-approved orphan drug VYKAT XR for Prader-Willi syndrome. The company manages considerable risks linked to dependence on a single product, early-stage commercialization challenges, and ongoing patent and regulatory uncertainties. Despite substantial debt, improved cash flows reflect operational leverage gains and cautious capital spending. Monitoring future EMA approval outcomes and commercialization execution remain critical milestones.

Historical Performance: From Development Losses to Profitability

Soleno Therapeutics operated as a clinical-stage biopharma company until early 2025 with sustained operating losses due to R&D investments and limited revenues. Revenue grew modestly before 2025, reaching approximately $1.45 million in 2016 [F1]. The significant inflection came following the FDA’s approval of VYKAT XR (diazoxide choline prolonged-release tablets) in March 2025 for treating hyperphagia in patients with Prader-Willi syndrome (PWS), a rare genetic disorder characterized by insatiable appetite.

The commercialization launch starting mid-2025 propelled revenues upward alongside more disciplined cost management. For FY 2025, Soleno reported:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 21 | 47 | 9 | 73000 | +111.9% |

| 2024 | -176 | -69 | -188 | 218000 | -351.0% |

| 2023 | -39 | -25 | -41 | 0 | -62.0% |

| 2022 | -24 | -21 | -24 | 13000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 47 | 4.6 |

| 2024 | -69 | -71.7 |

| 2023 | -25 | -24.8 |

| 2022 | -21 | -232.6 |

Source: SEC companyfacts cache [F1].

Revenue prior to the commercial launch was negligible or absent [F1], [S1]. This represents a substantial turnaround from multi-year heavy operating losses exceeding $180 million in prior years to positive profitability within the last fiscal year [F1]. The net income significantly outpaced operating income in FY25 likely reflecting non-operating items such as debt modifications or tax impacts yet to be fully detailed.

Operating cash flow improvement to nearly $47 million highlights successful transition from cash burn to solid positive cash conversion from operations [F1]. Capital expenditures remained minimal at just $73 thousand in FY25 indicating emphasis on commercial scaling over asset-heavy expansion.

Growth Drivers and Commercialization Progress

VYKAT XR addresses an unmet medical need in PWS patients suffering from severe hyperphagia—a symptom with no widely effective treatments prior to this approval [S1]. This orphan drug status confers regulatory exclusivity privileges but entails a small market size dictated by patient prevalence.

Sales commenced mid-2025 marking the start of meaningful top-line recognition after years without product revenue [S1]. The company is actively investing in expanding sales force and marketing infrastructure while pursuing regulatory filings internationally— notably submitting a Marketing Authorization Application (MAA) with the European Medicines Agency (EMA), currently under review [S1], [S14].

Key growth factors include:

- Market acceptance by physicians, caregivers, and healthcare payers.

- Expansion into pediatric populations age four and above.

- Potential approvals in additional geographies including EU markets.

- Sustained post-marketing safety profile supporting wider adoption.

Commercialization remains nascent with sales scale subject to uncertainties around payer reimbursement amid healthcare cost containment pressures [S14], potential EMA approval outcomes [S1], possible competition post-patent expiry [S24], and general orphan indication market constraints.

Milestones & What to Watch

No explicit forward guidance was disclosed for revenues or margins beyond acknowledging initial growth pacing contingent on successful commercial execution [N1], [S1]. Important upcoming milestones include:

- EMA decision on MAA approval expected following current response cycles [S1].

- Continued ramp-up of commercial infrastructure including salesforce expansion and patient support programs.

- Monitoring uptake metrics among targeted PWS patient groups in U.S.

- Managing patent defense outcomes against potential generic challenges due to drug listing in FDA Orange Book [S24].

- FY26 full-year results will be pivotal to assess sustainability of profits.

Future performance will hinge critically on achieving sufficient penetration within this rare disease community while controlling costs as commercialization scales.

Returns & Capital Allocation Dynamics

The firm posted an approximate return on equity (ROE) of about 4.6% for FY25 calculated as net income relative to equity base ($20.89M / $450.12M), indicating modest profitability aligned with early commercial maturity [F1].

Free cash flow generation led by strong operating pre-cash earnings less modest capital investment resulted in about $46.7 million FCF for FY25 [(CFO - Capex)] [F1]. This positive free cash flow marks a fundamental shift enabling greater financial flexibility.

Soleno maintains a $50 million secured loan facility with Oxford Financing LLC carrying interest-only payments through an extended period post-FDA approval—providing manageable leverage albeit constraining strategic options given covenants limiting dividends or acquisitions until loan maturity [S6], [S10].

Alongside positive cash flows, the company initiated an accelerated share repurchase program targeting up to $100 million—signaling confidence in stock valuation and commitment to returning capital efficiently without compromising liquidity reserves [N1].

Balance sheet strength is evident with current assets exceeding $355 million against liabilities under $62 million yielding a current ratio near 5.8x—supporting operational agility during this growth phase [F1].

Risks: Concentration & Regulatory Uncertainty Remain Critical

Despite initial success, concentration risk is pronounced due to dependency on a single approved drug—VYKAT XR—which if fails adoption or faces competitive pressure could derail financial prospects [S1], [S4]. Intellectual property protection affords exclusivity primarily via orphan drug status but remains narrow given evolving regulatory interpretations and potential generic entry post-patent expiration [S24], [S25].

Other salient risks include:

- Early-stage commercialization challenges typical for biotech firms transitioning from development-focused models including scale-up risks of marketing/sales functions [S1].

- Reimbursement environment volatility particularly under evolving U.S healthcare reforms such as Inflation Reduction Act impacts on Medicare pricing strategies restricting pricing power [S14], [S20].

- Regulatory hurdles remain for foreign approvals with potential delays or denials at EMA or other jurisdictions impacting global revenue diversification ambitions [S14], [S21].

- Litigation risks related to intellectual property disputes and compliance with healthcare fraud/abuse laws can impose material costs and distract management focus [S26].

- Macroeconomic uncertainties affecting capital markets access despite recent profitability may still constrain funding alternatives if needed for pipeline or commercialization expansion initiatives [S6], though current liquidity appears ample.

Conclusion

Soleno Therapeutics’ transition from developmental losses into profitability underscores successful execution post-VYKAT XR approval during 2025—an uncommon inflection point that provides foundational momentum for building sustainable commercial operations within rare disease treatment space.

While financial metrics reflect promising early operational strength coupled with prudent capital deployment towards debt management and shareholder returns, meaningful uncertainties remain around broader market acceptance, patent cliff threats, international regulatory outcomes, and evolving reimbursement landscapes necessitating continued scrutiny.

The company’s focus now pivots towards strengthening its commercial infrastructure domestically while navigating European regulatory feedback cycles alongside vigilant risk management around intellectual property litigation exposure—factors that will critically shape next phase financial trajectories.

Disclaimer: This analysis is based solely on publicly available information as of February 26, 2026. It does not constitute investment advice but aims to provide an informed overview respecting documented facts only.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments