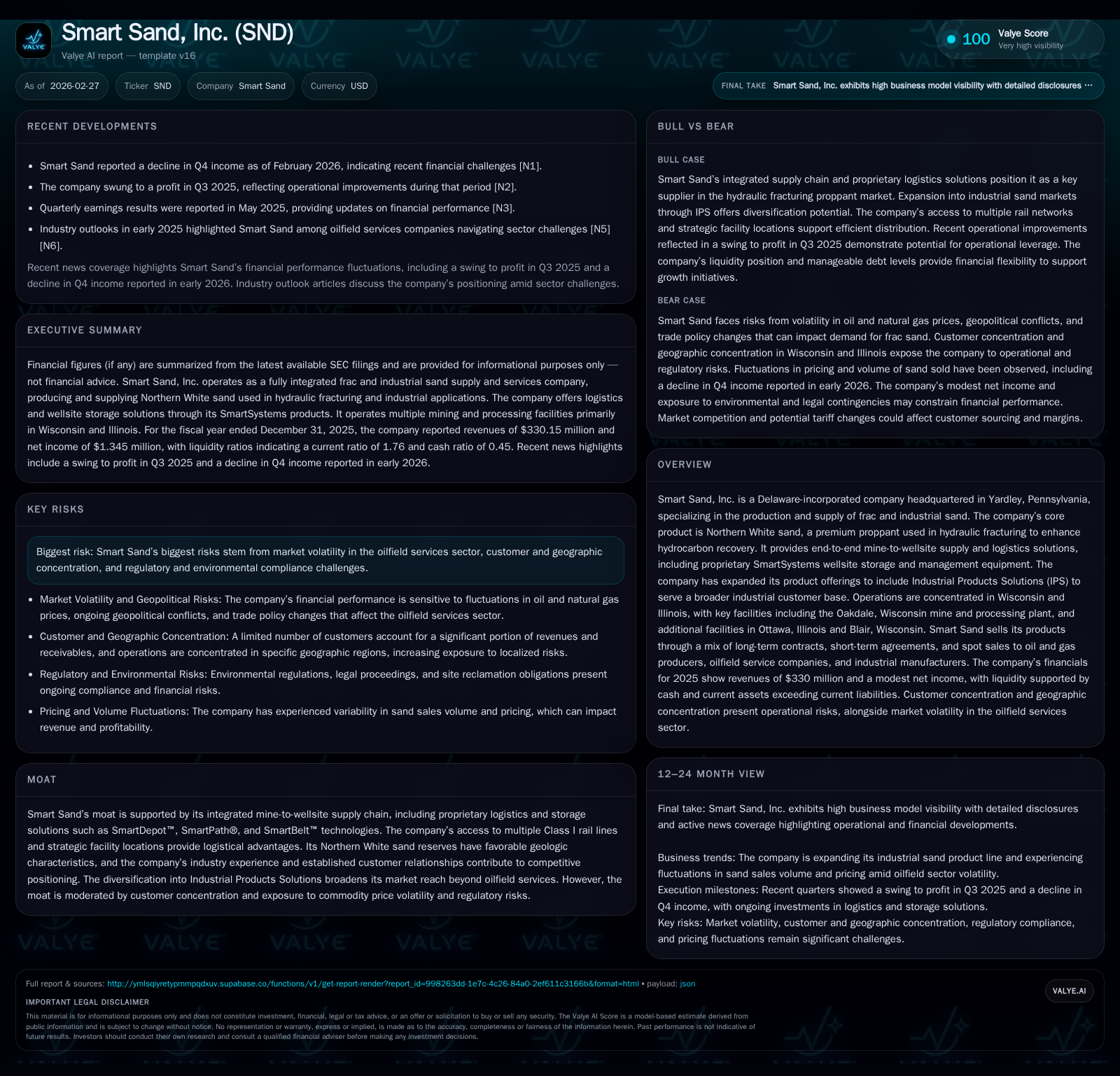

Smart Sand Balances Expansion and Fragmented Earnings Amid Market Volatility

After years of top-line growth, Smart Sand faces profitability pressures in 2025, reflecting operational costs and market uncertainties.

Smart Sand, Inc. continued its historical revenue growth trajectory into 2025, driven by increasing sand volumes and expanding product diversification into Industrial Products Solutions (IPS). However, this growth masked a sharp deterioration in operating income due to rising logistics and production costs amid oilfield sector headwinds. The company's integrated mine-to-wellsite supply chain and proprietary SmartSystems equipment provide competitive advantages but face limits amid customer concentration and tariff risks. Smart Sand increased capital expenditures to support capacity expansions while maintaining prudent debt management and modest shareholder returns. Going forward, monitoring margin recovery, IPS expansion progress, and tariff developments will be critical to assessing Smart Sand’s financial trajectory.

Record of Revenue Growth and Evolving Operational Drivers

Smart Sand maintained steady top-line momentum in the fiscal year ended December 31, 2025, reporting revenues of approximately $330.2 million — a 6% increase over $311.4 million recorded in 2024 [F1]. This growth reflects sustained increases in sand volumes sold, driven primarily by industry-wide trends such as increasing lateral well lengths and greater proppant loading per linear foot of lateral well bore [S7]. These factors inherently raise demand for high-quality Northern White frac sand, the company's core offering.

Additionally, Smart Sand's strategic diversification into Industrial Products Solutions (IPS) has broadened its addressable market beyond traditional oilfield services. The IPS segment taps industrial sectors including glass manufacturing, foundries, filtration systems, renewables, ceramics, turf & landscape products, as well as retail and recreation markets [S7][S14]. Although IPS currently comprises a small portion of overall sales, investments like blending and cooling facilities at the Ottawa Illinois plant signal management’s intent to expand this business line.

The company's vertically integrated model — from sand excavation through processing to wellsite delivery — enables control over end-to-end supply chain operations. Key facilities such as the Oakdale Wisconsin mine (capacity 5.5 million tons annually), Ottawa Illinois facility (1.6 million tons capacity), and Blair Wisconsin site (~2.9 million tons capacity) contribute substantially to overall volume capability [S21][S23]. These assets’ geographic positions also confer logistical advantages given their direct access to multiple Class I railroads including Canadian Pacific, Union Pacific, Burlington Northern Santa Fe (BNSF), and Canadian National [S20][S23].

Annual Financial Overview

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 330 | 1 | 44 | -4 | +6.0% | -55.0% |

| 2024 | 311 | 3 | 18 | 3 | +5.2% | -35.6% |

| 2023 | 296 | 5 | 31 | -2 | +15.7% | +761.3% |

| 2022 | 256 | -1 | 5 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 1 | 33 |

| 2024 | 4 | 0 | 11 |

| 2023 | 5 | 8 | |

| 2022 | 1 | -7 |

Source: SEC companyfacts cache [F1].

Source: [F1]

Profitability Under Pressure: Causes Behind Operating Income Decline

Despite this positive revenue trend, Smart Sand experienced a sharp decline in operating income in calendar year 2025 — slipping into an operating loss of approximately $4.46 million versus an operating profit of $3 million the year prior [F1]. This dramatic swing reflects growing margin pressures attributed largely to escalating logistics costs and operational inefficiencies.

Cost breakdowns detailed within quarterly filings reveal that logistics expenses climbed notably throughout the year due to shifts in delivery locations, resulting in lost transportation efficiencies amidst fluctuating demand patterns [S9]. Higher mining production costs similarly contributed as unit economics were stretched by volume volatility following a slowdown during Q1 which subsequently recovered later in the year [S7][N1].

Moreover, utilization rates for the SmartSystems product line — encompassing patented portable wellsite proppant storage technologies such as SmartDepot™, SmartPath®, and SmartBelt™ — declined earlier in the year causing revenue erosion within that segment [S27]. Although these systems integrate tightly with the company’s logistics solutions offering competitive differentiation, their early-2025 dip highlights sensitivity to end-customer activity swings within oilfield services.

Further exacerbating profit pressures were modest price fluctuations across frac sand commodities consistent with sector volatility driven by global macroeconomic uncertainties including geopolitical tensions impacting crude oil markets [S7]. Notably, contract renegotiations with large customers — which account for a significant proportion of sales volume — introduce additional complexity into pricing stability given high customer concentration risks [S16][S17].

The Strategic Role of Integrated Logistics and Product Diversification

Smart Sand's competitive positioning hinges on its integrated mine-to-wellsite supply chain supported by proprietary logistics innovations embedded in the SmartSystems suite [S20]. The combination of on-site processing capabilities with direct rail access permits nimble transportation planning leveraging all major Class I rail networks on different regional fronts.

Beyond physical infrastructure advantages, the company’s software-enabled proppant management systems facilitate efficient unloading, storage, blending and delivery at drilling sites which not only enhance customer operational uptime but also lock in contractual relationships through equipment rentals under flexible terms [S20]. This technology-led approach is increasingly critical as field operators seek reliable solutions capable of adapting to more complex fracture designs requiring higher proppant volumes per lateral length.

However, customer concentration remains a structural challenge: four customers accounted for over sixty percent of accounts receivable as of September 30, 2025 [S16][S24]. Regulatory risk also looms related to environmental compliance demands imposed on mining operations primarily situated in Wisconsin and Illinois; potential changes could restrict output or increase operational costs [S17].

On diversification frontiers, Industrial Products Solutions represents a strategic hedge against cyclical oilfield demand shocks by targeting industrial markets that utilize silica sand for applications ranging from glassmaking to filtration media [S7][S14]. While still nascent relative to core frac sand sales volumes, recent capacity expansions such as blending enhancements at Ottawa underscore management’s prioritization of this segment’s long-term growth potential.

Financial Structure, Capital Allocation, and Shareholder Returns

Smart Sand strengthened financial flexibility with a revolving credit facility signed September 3, 2024 providing up to $30 million subject to borrowing bases inclusive of accounts receivable and inventory collateralization [S4][S8]. This facility was undrawn at September 30, 2025 with availability supporting liquidity needs amid sector cyclicality.

Capital expenditures in FY2025 totaled approximately $11.6 million — up roughly +65% versus prior-year levels — directed toward expanding processing capacities at key facilities including Oakdale along with terminal upgrades such as Dennison Ohio expansion projects underway [F1][S29].

Robust operating cash flow generation ($44 million) combined with capex outlays resulted in estimated free cash flow near $32.5 million supporting shareholder returns including dividends totaling about $6 million (up from nearly $3.9 million prior year) alongside modest share repurchases approximating $628 thousand continuing return-of-capital programs despite profitability challenges [F1][N1][S3].

Long-term debt stood manageable near $17.6 million at year-end comprising equipment financing arrangements underpinning proprietary SmartSystems assets via sale-leaseback financing expiring mid-2028 at fixed interest rates around ~8.56%, illustrating prudent asset-backed financing consistent with industrial equipment investment norms [S4][S8][S12].

Economic and Sector Headwinds Impacting Demand and Pricing Dynamics

Externally sourced risks weigh on demand stability notably including oil price fluctuations influenced by geopolitical events such as conflicts affecting global energy supplies and OPEC production decisions that ripple into hydraulic fracturing activity levels across North American basins [S7][N1].

Trade policy evolutions have alleviated tariffs formerly imposed on Canadian sand imports after Surtax Remission Orders eliminated duties; however future adjustments remain possible injecting ambiguity into cross-border cost structures potentially prompting shifting sourcing strategies among clientele seeking cost efficiency [S7][S17].

Regulatory compliance presents ongoing operational risk especially related to environmental standards governing mining activities within Wisconsin/Illinois mines constituting majority reserves; any tightening could escalate compliance costs or force curtailed extraction volumes limiting supply-side flexibility amid evolving demand patterns [S17].

These macro factors engender pricing variability typical within commodity-linked industrial supply chains prompting more conservative contract structures emphasizing variable pricing tied closely to input costs alongside volume commitments coupled with penalty provisions complicating revenue predictability.

Outlook: What to Monitor on the Path Ahead for Smart Sand

While formal guidance is limited post-FY25 filings several indicators warrant attention:

- Early-2026 quarterly results will reveal if margin compression can be arrested through efficiency gains or favorable market conditions.

- Progress expanding Industrial Products Solutions customer penetration will test diversification efforts smoothing cyclicality exposure.

- Completion milestones for terminal expansions such as Dennison Ohio should augment throughput enhancing logistics value propositions.

- Tariff environment evolution remains pivotal; vigilance around trade policy shifts affecting Mexico or U.S export/import regulations is necessary.

- Recovery in SmartSystems equipment utilization would bolster revenue streams reaffirming strategic value within integrated offerings.

- Capital allocation balancing reinvestment against shareholder returns will continue shaping company profile amid fragmented profitability evidenced by recent quarterly results showing Q4 income decline alongside new repurchase program approvals highlighting commitment toward shareholder value preservation despite volatility ([N1],[S3]).

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments