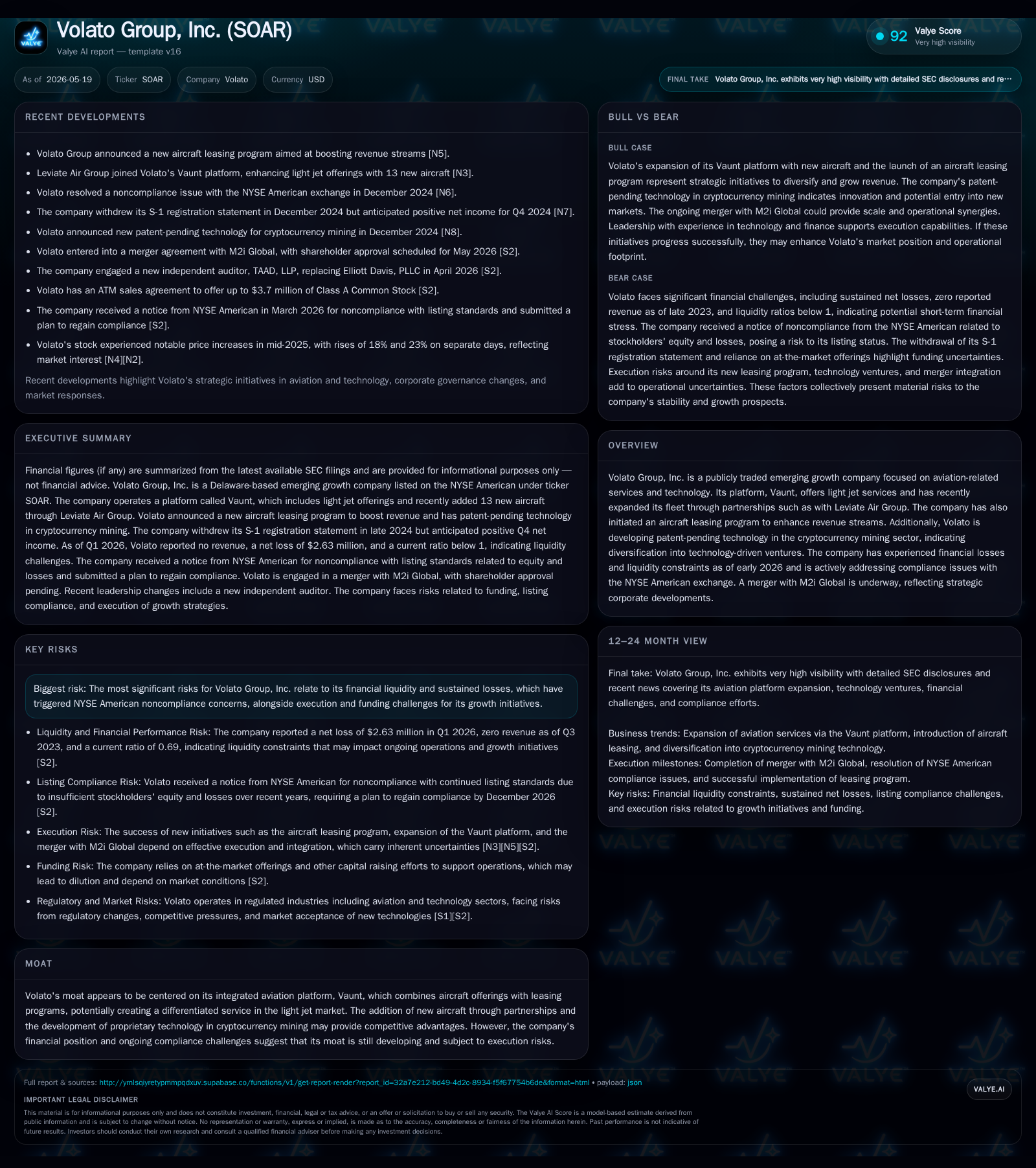

Volato Group's Growth Strategy and Operational Challenges at a Crossroads

Recent quarterly disclosures reveal Volato Group navigating expansion via fleet growth and tech ventures while managing liquidity and compliance pressures.

Volato Group, Inc. continues to advance its integrated aviation platform, Vaunt, through strategic partnerships that expand its light jet fleet and initiate leasing programs. Simultaneously, it is exploring diversification into cryptocurrency mining technology. However, its latest quarterly filing highlights critical challenges including liquidity deficits, operating losses, and regulatory noncompliance risks on the NYSE American exchange. The ongoing merger with M2i Global further adds complexity to its corporate trajectory, positioning the company at a pivotal juncture where execution and funding are decisive for future progress.

Latest Quarterly Update: Strategic Moves Amid Financial Pressure

Volato Group’s 10-Q filed May 15, 2026, provides a clear window into a company simultaneously expanding its operational footprint while confronting pressing financial constraints [S2]. Notably, Volato reports having zero cash and equivalents as of March 31, 2026, coupled with current assets of approximately $5.7 million against current liabilities near $8.3 million—yielding a current ratio of only 0.69, indicative of strained short-term liquidity [F1].

Operationally, the quarter highlights key strategic moves including the expansion of the Vaunt light jet fleet via partnership agreements such as with Leviate Air Group. This move supports scaling capacity aiming at better fleet utilization rates—a crucial factor in driving revenue in the highly competitive light jet services segment where fixed costs are substantial [S2]. In parallel, Volato launched an aircraft leasing program intended to unlock recurring lease income streams complementing its core flight services platform.

On the corporate front, significant progress towards merging with M2i Global has been disclosed: evidence from proxy statements and special meeting outcomes shows shareholder approval of merger proposals with certain closing conditions still pending fulfillment [S3][S25]. However, this transaction adds layers of integration risk given M2i’s differing operational profile.

Lastly, regulatory tension persists; Volato received notification from NYSE American in March 2026 reflecting noncompliance due to deficient stockholders’ equity amid repeated losses [S28][S2]. While it has submitted a plan to regain compliance by December 2026, the risk of delisting remains a looming operational hazard that could materially affect access to capital markets and investor sentiment

Business Model Overview: Integrated Aviation Services and Tech Diversification

At its core, Volato monetizes through the Vaunt platform—a light jet services aggregator providing private aviation options supported by both direct aircraft operations and an asset leasing business line [S1]. Customers primarily pay for aircraft usage either via charter or through long-term leases structured to optimize fleet deployment economics.

The introduction of the leasing program suggests a strategic tilt towards stabilizing revenue streams beyond variable flight activity fluctuating with demand cycles. By owning or controlling aircraft assets leased out to operators or end-customers under contractually recurring payments, Volato can enhance gross margin predictability while spreading fixed asset costs over longer periods.

Complementing this aviation focus is Volato’s investment into patent-pending technology targeting cryptocurrency mining operations [N1][S1]. This initiative signals deliberate diversification into technology sectors that may provide alternate revenue channels leveraging intellectual property assets—albeit at an embryonic stage lacking revenue impact within current filings.

This hybridized model underscores management's attempt to build a synergistic ecosystem blending tangible aviation service offerings with innovative tech ventures potentially boosting enterprise value if successfully commercialized.

Industry Context: Light Jet Market Dynamics and Technology Venturing

Volato operates within the light private jet market—a segment characterized by capital-intensive fleet requirements alongside highly variable demand influenced by economic cycles and disposable income trends among high-net-worth clients. Customer payment models typically pivot between ad hoc charter pricing versus contract-based subscriptions or leases which afford steadier cash flow profiles.

Pricing power hinges on brand reputation, fleet modernity, network connectivity offered through platforms like Vaunt, and operational reliability. Capacity constraints arise largely from limited availability of modern light jets combined with pilot workforce shortages—factors driving barriers to entry but also causing supply-side volatility.

In parallel, Volato’s crypto mining technology venture intersects two fast-evolving sectors: aviation and blockchain-based computing infrastructure. Crypto mining profitability depends heavily on energy efficiency of proprietary hardware/software solutions alongside prevailing cryptocurrency market prices—a domain presenting rapid innovation cycles but also regulatory scrutiny.

This cross-sector approach could create differentiated capabilities if integration synergies arise; however, regulatory regimes governing aircraft operations differ greatly from those applying to digital asset ecosystems posing multifaceted compliance challenges.

Competitive Positioning: The Vaunt Platform’s Advantages and Limitations

Volato’s Vaunt platform embodying combined aircraft operations plus leasing programs offers competitive differentiation in several respects. The partnership-enabled fleet expansion grants access to diversified aircraft types increasing service reach without proportional capital outlays.

Leasing programs embed customer lock-in features by fostering longer contractual relationships improving utilization visibility which is critical in capital-heavy aviation asset management. Pricing power may benefit from this integration via bundled service offerings enhancing customer switching costs compared to spot charter competitors or standalone lessors.

Nonetheless, competitive risks remain given fragmented nature of private aviation markets populated by established charter operators (e.g., NetJets), leasing firms specializing in various jet classes, as well as emerging digital brokerage platforms offering convenience-focused booking experiences. Execution risks persist especially around scaling Vaunt offerings profitably amidst volatile operating cost trends (fuel/prices) and labor dynamics affecting availability.

Proprietary crypto mining initiatives could serve as a moat if patent claims lead to sustainable advantages; yet these ventures require substantial R&D investments with uncertain timelines before meaningful monetization.

Growth Drivers: Fleet Expansion, Aircraft Leasing, and Crypto Mining Initiatives

Key vectors fueling Volato’s growth stem from ramping up fleet size through partnerships such as Leviate Air Group—enabling enhanced route/network density raising potential flight hour volumes [S2][N1]. Higher utilization can drive incremental top-line while diluting fixed overheads improving margin profiles.

Aircraft leasing launches add new streams generating recurring leasing yields which reduce dependency on spot flight bookings exposing results to cyclical downturns. Effectiveness depends strongly on lease contract lengths/terms secured encompassing maintenance responsibilities influencing net returns.

The technology arm focused on crypto mining patents represents diversification aiming for asymmetric growth opportunities unrelated directly to cyclical aviation demand fluctuations offering optionality if scalable deployments materialize [N1][S3].

Near-term milestones tracked include merger completion potentially unlocking synergies/resources enabling accelerated rollout; progression toward NYSE American compliance resolution underpinning capital access stability; along with demonstration projects or pilot commercial applications validating crypto mining tech efficacy.

Risks and Constraints: Liquidity Challenges, Compliance Risks, and Execution Hurdles

Liquidity stands out as the most pressing concern—zero reported cash balance against current liabilities exceeding assets implies limited buffer for operational delays or capital expenditures absent additional financing or equity injections [F1]. Operating losses evident historically amplify funding urgency challenging sustained runway extension.

NYSE American exchange noncompliance notices underscore regulatory vulnerabilities threatening public listing continuity—a cornerstone for broader investor confidence access. Although remedial plans have been submitted for review aiming at year-end resolution windows remain tight with no guarantees mitigating delisting risks [S28][S2].

Execution complexities multiply given concurrent multi-pronged strategies spanning fleet scaling, lease program development plus pioneering blockchain-based technologies demanding distinct expertise domains elevating managerial bandwidth strains.

Market cyclicality inherent in private jet demand combined with nascent stage tech investments limit near-term profitability prospects; reliance on favorable capital markets conditions for growth funding further compounds risks should market sentiment deteriorate.

Key Milestones Ahead: Merger Progress, Regulatory Compliance, and Capital Raising

Volato’s imminent attention centers around completing its merger with M2i Global following shareholder approvals granted at special meetings earlier in May 2026—the deal remains subject to typical closing conditions including SEC clearance and financing arrangements finalized [S3][S25]

Successfully executing a NYSE American compliance plan before December deadline will be crucial for maintaining listing status facilitating ongoing capital infusion opportunities vital given zero cash positions reported recently.

Monitoring early indicators such as initial lease contract signings ramp-up metrics post-fleet addition as well as crypto mining patent commercialization developments will provide tangible progress signals supporting underlying growth thesis.

Capital raising efforts or strategic partnerships executed timely could alleviate liquidity stress permitting more aggressive investment phases required for scaling operations sustainably.

Financial Snapshot: Liquidity Position and Operating Performance

As per the most recent quarter ending March 31, 2026, Volato carries no cash reserves while its current assets stand at approximately $5.7 million overshadowed by nearly $8.3 million of current liabilities leaving a current ratio at 0.69—significantly below typical healthy operating thresholds indicating financial tightness [F1]

Although past annual filings reported operating income gains around $3.96 million and net income approximately $5.17 million for full year 2025 reflecting some profitable ventures prior to Q1 2026 liquidity deterioration indicates recent operational spending outpacing incoming cash flow severely constrains runway length absent fresh capital resources [F1]

This financial profile reinforces analytical perspectives highlighting execution leverage points heavily dependent on closing mergers timely successfully implementing leasing programs alongside securing compliant exchange status critical for credible financing avenues ahead.

Disclaimer: This analysis is based solely on information publicly available as of May 19, 2026. It does not constitute investment advice or research views but aims to provide an informed industry perspective on Volato Group's operational context.

Financial position in context

As of 2026-03-31, companyfacts shows 0 USD in cash and equivalents [F1]. Current assets of $6mm and current liabilities of $8mm imply a current ratio near 0.69x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments