Spindletop Oil & Gas: Quarter-End Update Highlights Funding and Market Access Challenges

Q1 2026 reveals Spindletop's reliance on operating cash flow amid capital spending uncertainties and investor sentiment pressures.

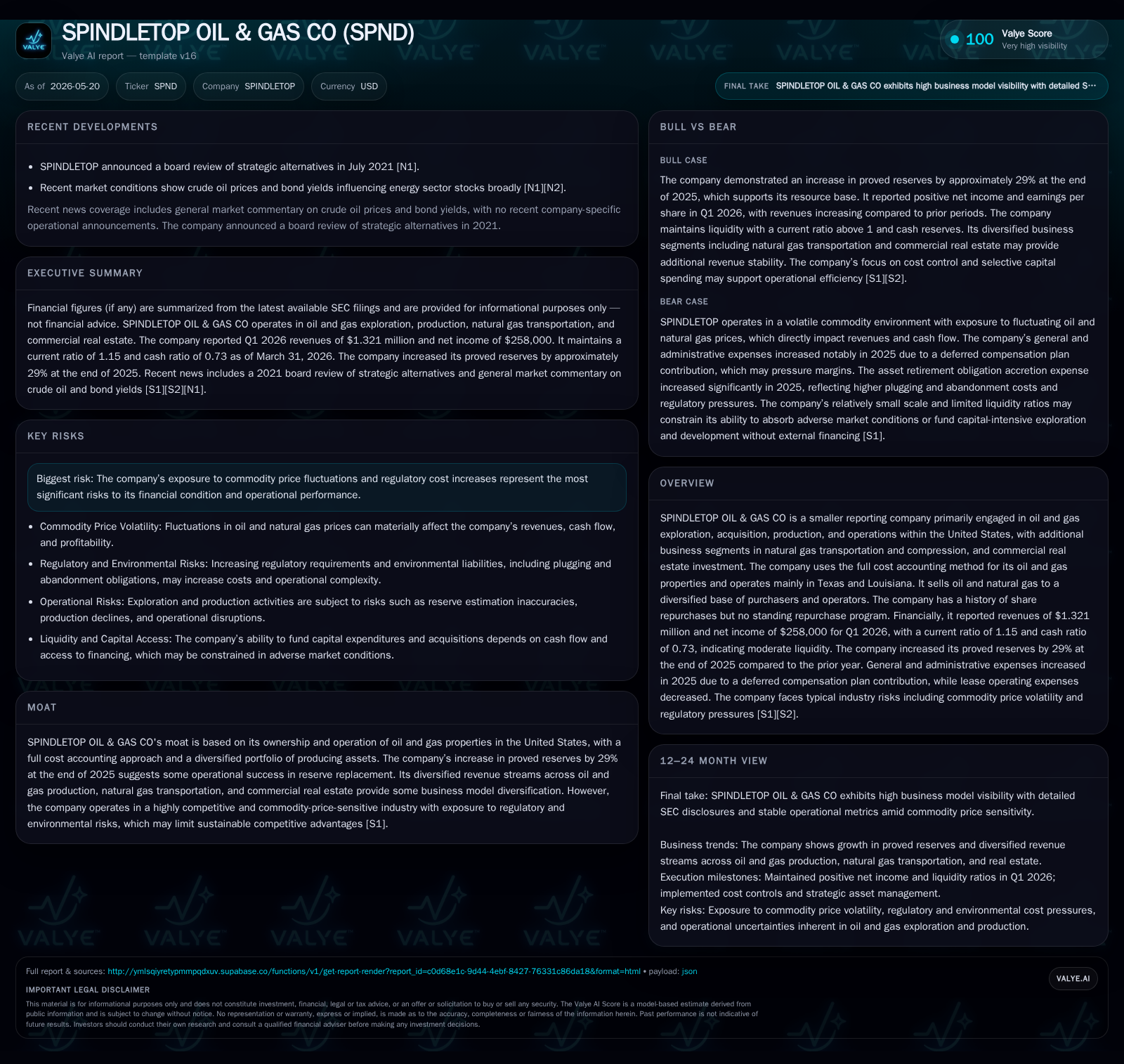

Spindletop Oil & Gas’s Q1 2026 filing underscores a funding model dependent primarily on internal cash flow, with no guarantees of sustaining capital spending levels without external financing. The company faces liquidity constraints compounded by its stock’s downgrade to OTC Pink Limited, curbing market access and shareholder trading liquidity. A notable 29% increase in proved reserves at year-end 2025 provides operational upside, but capital availability and shifting investor attitudes toward fossil fuels present significant risks to growth and financing pathways.

Q1 2026 Operational Update: Funding Model and Market Access Challenges

Spindletop Oil & Gas Co’s first-quarter 2026 SEC filing (Form 10-Q dated May 20) places emphasis on its operating capital needs being predominantly funded from cash flow generated by operations. However, it explicitly states that there is no assurance that this internally generated cash will suffice to maintain current capital spending levels due to variables such as production rates and commodity prices [S2]. This uncertainty opens the door for potential reliance on third-party financing through joint ventures or asset sales. Undertaking such external funding could lead to relinquishing operating interests or ceding operational control of some assets — a tradeoff that could impact strategic autonomy.

Complicating matters further is the downgrade of Spindletop’s stock to the OTC Markets Pink Limited tier effective July 2025. This status entails limited issuer involvement and triggers a prominent cautionary "Warning! Limited Information" designation on quotations, which has already inhibited trading liquidity for shareholders. The company recognizes that this reduced market presence likely adversely affects its ability to raise equity or debt capital, creating tangible challenges in accessing broader markets especially in an environment where the oil and gas sector faces growing investor skepticism due to ESG concerns [S2], [S10].

Together, these factors delineate a constrained capital picture entering mid-2026: the company must carefully balance sustaining its exploration and development program against tightening funding channels.

Spindletop’s Business Model and Asset Quality: Full Cost Accounting and Portfolio Diversity

Spindletop operates mainly in Texas and Louisiana focusing on oil and gas exploration, acquisition, production, alongside natural gas transportation and compression services [S1]. Additionally, it holds assets in commercial real estate investing — an uncommon diversification play within upstream-focused companies

Its revenue mechanics rely on selling produced hydrocarbons to a diversified base of purchasers, which helps mitigate customer concentration risks typical for smaller independents [S1]. The company's employment of the full cost accounting approach means all acquisition and development costs are capitalized into a single cost pool amortized over estimated reserves. While this method tends to smooth earnings volatility versus successful-efforts accounting by deferring impairments amid downturns, it can obscure sharp economic reversals when commodity price drops lead to ceiling tests impairments that require writedowns

This business mix provides moderate strategic strength through asset diversification; notably, the natural gas transportation segment benefits from fee-based revenues somewhat decoupled from commodity price swings. The commercial real estate holdings further cushion revenue cyclicality but remain a much smaller part of total operations.

Industry Competitive Framework: Commodity Sensitivity and Capital Market Dynamics

The broader oil and gas industry remains highly exposed to volatile commodity prices which cycle with global economic conditions, geopolitical events, and supply-demand imbalances. For a modest-sized independent like Spindletop with limited scale, this volatility translates directly into earnings swings given less operational hedging capacity or portfolio breadth compared to larger integrated peers.

Moreover, pervasive ESG activism has altered investment flows in recent years. Spindletop's filings candidly acknowledge how negative public attitudes toward fossil fuels have led some institutional investors—wealth funds, pension funds, university endowments—to divest from or avoid oil and gas sector exposure altogether. Lending institutions have similarly tightened credit availability or increased costs for E&P operators amid concerns over climate change policies and regulatory risks. These evolving dynamics compress both debt and equity capital access for smaller players lacking significant balance sheet strength or project scale to offset such headwinds effectively [S2], [S3].

Spindletop's downgraded OTC Pink trading status exacerbates these challenges by reducing visibility and liquidity among investors.

Growth Catalysts: Reserve Additions, Asset Optimization, and Segment Diversification

A material positive revealed in the most recent filings is Spindletop's reported increase of nearly 29% in proved reserves at December 31, 2025 relative to the prior year-end. This sizeable reserve replacement signals operational success in both appraisal/acquisition activities and efficient development execution — critical metrics anchoring future production visibility and mid-term cash flow potential [S1], [F1].

In addition to traditional upstream activities generating production revenue, the company's natural gas transportation/compression business offers fee-based income streams tied more directly to capacity agreements rather than commodity prices alone — potentially enhancing margin stability during episodic market downturns.

Further diversification stems from its commercial real estate investments providing non-cyclical rental income stream that lowers overall business risk profile despite being a smaller component.

These growth drivers collectively hinge on maintaining sufficient capital spending levels particularly for drilling/recompletion programs designed to convert proved reserves into production volumes.

Risks and Constraints: Capital Availability, Regulatory Pressures, and Investor Sentiment

Among key risks outlined are the tightening credit conditions affecting Spindletop’s ability to raise necessary third-party funds should operating cash flows fall short. The company admits the possibility of needing joint ventures or property sales that may dilute operating control — strategic compromises that could constrain future growth options [S2], [S3].

Additionally, ongoing litigation risks persist relating to pollution claims filed against subsidiaries operating Louisiana properties. Although one prior lawsuit was dismissed without prejudice early this year (February 2025), a newer suit filed December 2024 remains active with management anticipating vigorous defense but acknowledging potential contingencies requiring monitoring [S1], [S20].

Coupled with cyclical risk case from commodity price slumps exacerbated by geopolitical/economic uncertainties (including inflation-driven recession risks), these factors converge as material constraints limiting operational flexibility.

Investor sentiment trends influenced by ESG activism pose medium-term threats potentially reducing available equity injections required for sustaining capex programs critical for reserve development.

Near-Term Watchpoints: Financing Milestones, Production Stability, and Litigation Developments

Critical near-term indicators include whether Spindletop can secure alternative financing mechanisms—such as joint ventures or asset monetizations—on terms preserving adequate operating interests without unduly sacrificing control. Timely completion of such transactions would support ongoing exploration drilling programs imperative for production replenishment.

Monitoring quarterly production volumes alongside realized commodity pricing will reveal underlying cash flow trends determining internal funding sufficiency.

Developments in pending lawsuits related to pollution claims require close observation given any adverse outcomes could necessitate financial provision or remediation expenditure impacting profitability.

Finally, shifts in public perception or regulatory landscape influencing broader sector investor appetite must be tracked as these external factors shape capital markets access essential for growth continuity.

Financial Health Snapshot: Liquidity Position and Debt Exposure

As of March 31, 2026 balance sheet data show Spindletop holding $4.256 million in cash equivalents against current liabilities approximating $6.834 million yielding a current ratio near 1.15 reflecting modest working capital adequacy [F1]

Operating income was negative for the latest full year period ended December 31, 2025 at approximately -$3.281 million reflecting earnings pressure consistent with sector-wide earnings volatility faced by smaller independents lacking hedging scale or diversified upstream portfolios at large integrated peers’ level [F1]

Liquidity appeared stable through Q1 in supporting operations; however persistent negative sector sentiment coupled with limited financial scale underscore refinancing risks should operational cash generation decline materially through lower realized prices or production reductions.

This analysis integrates disclosures explicitly drawn from Spindletop Oil & Gas Company’s recent SEC filings as of May 20, 2026 ([S1], [S2], [F1]) without extrapolations beyond presented data points or speculative projections. It aims solely to provide an informed view frame around operational results, strategic positioning, industry context, risk factors, and financial health pertinent at current reporting periods.

Financial position in context

As of 2026-03-31, companyfacts shows $4mm in cash and equivalents [F1]. Current assets of $8mm and current liabilities of $7mm imply a current ratio near 1.15x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments