Stellantis N.V. Confronts Severe Profitability Challenges Despite Global Scale

A comprehensive analysis reveals how Stellantis's broad global footprint could not shield it from significant losses driven by warranty and legal cost inflation in 2025.

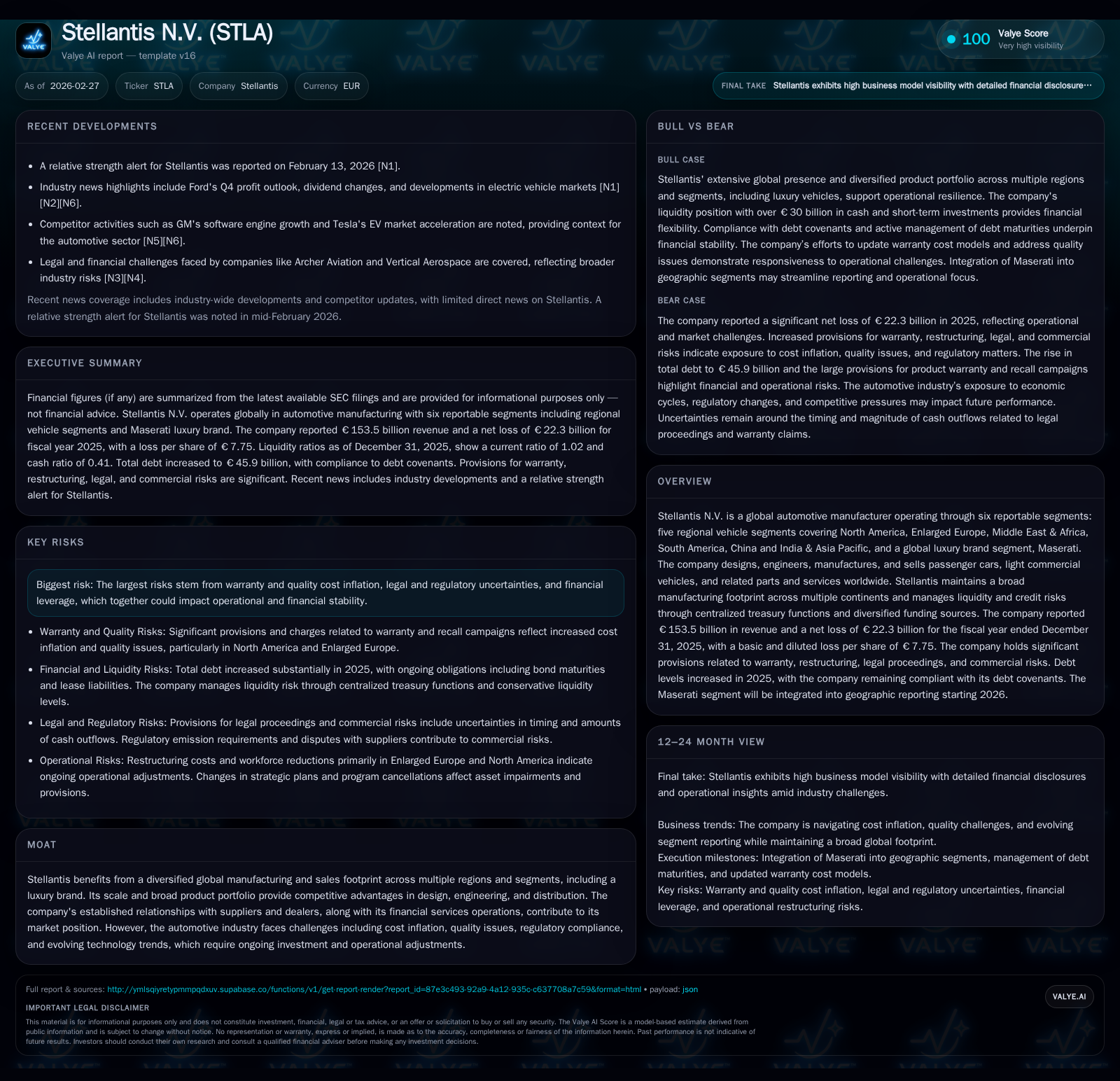

Stellantis reported €153.5 billion in revenue for 2025, marking a slight 2.1% decline from the prior year, yet faced a staggering net loss of €22.3 billion largely due to escalated warranty provisions and legal expenses. Despite its extensive geographic diversity and product portfolio spanning North America to Asia, legacy quality issues and litigation costs severely impaired profitability. The company maintained liquidity with €30.1 billion in cash and a near-unity current ratio but saw returns collapse with an approximate −41.4% ROE, prompting a dividend suspension. Going forward, margin recovery faces hurdles from cost inflation and regulatory pressures, with investor focus expected on provision roll-offs, capital structure optimization, and the pace of EV strategy implementation.

Revenue Decline Amid Broad Geographic Reach: Dissecting 2025 Results

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 153.5 | -22.3 | -2.1% | -504.6% |

| 2024 | 156.9 | 5.5 | -17.2% | -70.4% |

| 2023 | 189.5 | 18.6 | +5.5% | +11.0% |

| 2022 | 179.6 | 16.8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -41.4 |

| 2024 | 6.7 |

| 2023 | 22.7 |

| 2022 | 23.2 |

Source: SEC companyfacts cache [F1].

Despite Stellantis’s expansive global footprint spanning six reportable segments—including North America, Enlarged Europe, China, and India & Asia Pacific—the company saw its consolidated revenues slip to €153.5 billion in fiscal year 2025 from €156.9 billion in 2024, a year-over-year decline of approximately 2.1% [F1], [S10]. This contraction reflects persistent pressures across diverse regional markets compounded by shifting consumer preferences and product portfolio mix shifts that weighed on top-line growth.

The company's broad sales geography underscores its market reach; however, no single region provided sufficient growth momentum to offset softness elsewhere or cushion against macroeconomic challenges.[S10] Particularly pronounced was subdued performance in key segments like enlarged Europe and China where competitive intensity and regulatory changes have begun altering demand dynamics.

Escalating Provisions and Warranty Costs: Legacy Drag on Profitability

Profitability took a dramatic hit as Stellantis recorded a net loss attributable to owners of the parent of €22.3 billion for FY2025 [F1]. This severe downturn was predominantly due to an unprecedented surge in total provisions reaching €32.9 billion at year-end—comprising warranties, restructuring charges, legal disputes, commercial risks, and other contingencies [S1]. The product warranty and recall campaigns alone accounted for a significant portion (€14.1 billion), reflecting accelerated warranty cost inflation driven by legacy quality issues within the fleet.

Such warranty expense escalation directly undermines operating leverage benefits normally afforded by the group's scale and diversified model lineup. The legacy quality challenges not only inflate costs but also necessitate sustained capital outlays for remediation campaigns across multiple vehicle lines [S1]. This phenomenon resonates industry-wide where legacy defects continue to surface as significant profit headwinds despite high fixed-cost absorptions.

Legal Risks Amplify Financial Uncertainty: Scope and Materiality

The Company’s exposure to ongoing litigation added further strain on its financial profile with near €1 billion recognized in legal provisions alone [S1]. These litigation contingency reserves reflect uncertainties around various disputes ranging from intellectual property claims to product liabilities that remain unresolved at fiscal close.

Elevated legal risk amplifies volatility in earnings forecasts and constrains free cash flow generation capacity due to potential settlement outflows or protracted defense expenditures. Such risks necessitate robust risk management practices centered around conservative provisioning and scenario planning [S1].

Capital Structure Analysis: Liquidity Standing and Debt Composition

Notwithstanding massive losses, Stellantis retained solid liquidity buffers ending 2025 with cash and equivalents of about €30.1 billion ensuring operational continuity amidst capital stresses [F1], [S4], [S5]. A current ratio standing near unity at 1.02 underscores balanced short-term asset-liability alignment [F1].

The company’s financing structure reflected increased borrowing totaling approximately €45.9 billion—an €8.7 billion rise year-over-year driven mainly by new bond issuances (€5.1 billion) along with expansions in financial services funding [S9], [S25]. About one-third comprises asset-backed financing instruments securing loan receivables from retail customers and dealers—a common industry mechanism to diversify liquidity sources while isolating credit risk pools [S7], [S17].

Importantly, Stellantis remains compliant with all financial covenants associated with these debt facilities including cross-default clauses that could accelerate liabilities – mitigating near-term refinancing risk though underscoring leverage vigilance needs [S4], [S7], [S16]. Syndicated revolving credit facilities totaling up to €12 billion remain undrawn as strategic liquidity cushions with maturities extended post mid-2025 accords [S11].

Dividend Suspension and Shareholder Returns in a Loss Year

Reflecting the scale of earnings erosion resulting in a roughly −41.4% return on equity (calculated as net loss divided by equity of €54 billion) for the full year 2025, Stellantis’s Board opted to suspend dividends for the fiscal year 2026 following the prior special dividend payment of €0.68 per share distributed in May 2025 [F1], [S6].

This payout suspension aligns with prudent capital preservation imperatives given negative profitability trends amid elevated risk exposures.

The erosion of ROE starkly illustrates shareholder return challenges amid the conjuncture where losses dramatically exceed equity cushions.[F1]

The company's capital allocation philosophy emphasizes balancing strategic investments against sustaining financial equilibrium under adverse earnings scenarios alongside protecting credit ratings via measured buyback or capital distribution policies.[S6]

Future Growth Outlook and Operational Headwinds

Looking ahead, growth prospects appear constrained as Stellantis confronts multifaceted challenges including persistent cost inflation impacting raw materials—particularly platinum group metals used in catalytic converters—and labor costs tied to complex union negotiations primarily within European regions.[S1],[N12]

Additional regulatory headwinds stem from evolving emission standards requiring concerted investment into electrification technology platforms—mandating capex-intensive rollouts while compressing margins temporarily.[N12]

While broad product diversification has historically provided resilience through cyclical shifts, near-term recovery is tempered by supply chain constraints impacting component availability alongside legacy warranty remediation costs that divert resources.[S1],[N12]

Electrification efforts form a strategic lever but their gestation periods defer positive margin impacts into later years barring accelerated adoption or subsidy tailwinds.[N12]

Watching for Recovery Triggers: Milestones and Investors’ Focus

Absent explicit forward guidance post-2025 filings,[N12] investors should closely monitor several key performance indicators signaling structural operational improvements:

- Sustained reduction in warranty provisions indicating resolution of legacy quality burdens,

- Free cash flow generation consistent with deleveraging targets,

- Segment-level profitability improvements especially across North America and Enlarged Europe,

- Execution pace of new electric vehicle launches underpinning future growth,

- Refinancing activities maintaining supportive capital structure without covenant breaches,

- Portfolio optimization maneuvers balancing model mix toward higher-margin vehicles.

These KPIs embody sector-native valuation drivers where margin improvement combined with disciplined capital allocation often predicates valuation recoveries beyond transient earnings troughs.

This analysis synthesizes Stellantis N.V.’s fiscal year 2025 disclosures capturing the complex interplay between scale-driven advantages offset by significant cost inflation dynamics within warranties, legal realms, and restructuring actions that collectively depressed profitability sharply. The firm maintains robust liquidity though faces substantial capital return restraints amid market headwinds linked notably to technological transformation pressures facing automotive OEMs globally.

Future performance trajectories will hinge on effective containment of legacy cost pools alongside successful execution of electrification strategies within an intensely competitive environment subject to regulatory fluxes.

This report exclusively relies on data from official filings dated February 26, 2026 ([F1],[S#]) supplemented by select recent market commentary ([N12]). No investment recommendations are provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments