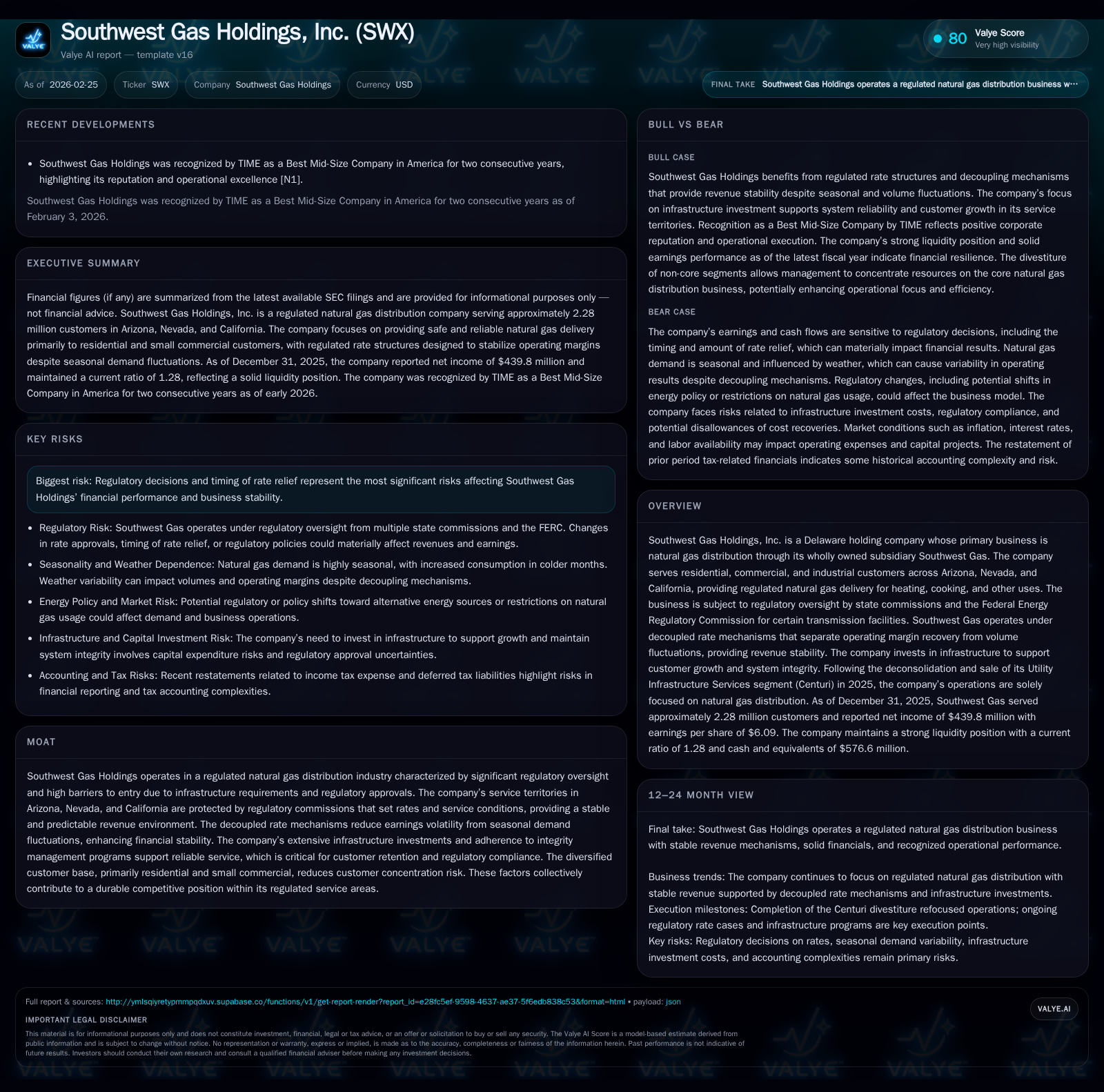

Southwest Gas Holdings’ Transition After Centuri Sale: Stability and Growth in Regulated Natural Gas

After divesting its utility infrastructure services segment, Southwest Gas Holdings has refocused on regulated natural gas distribution, leveraging robust regulatory frameworks and strategic capital management for sustained growth.

Southwest Gas Holdings finalized its strategic pivot in 2025 by divesting Centuri, streamlining operations exclusively into natural gas distribution across Arizona, Nevada, and California. Historical growth has been driven by steady customer additions, stable regulatory environments governed by decoupled rate mechanisms, and proactive infrastructure investments. Despite a short-term dip in free cash flow due to high capex, the company maintains strong operating cash flow and an approximate 11.1% ROE. Going forward, regulatory timing remains a key risk, but ongoing meter set additions and infrastructure programs underpin growth potential.

Historic Performance and Key Growth Drivers Through 2025

Southwest Gas Holdings witnessed substantial revenue expansion from FY2024 to FY2025, growing roughly by 9.6% to $4.83 billion [F1]. This uptick owes largely to the addition of some 37,000 new meter sets during the year—an indicator of underlying customer base expansion concentrated across Arizona, Nevada, and California [S4][S5]. Operating income remained strong despite settling slightly down by around 2% to $474 million in FY2025, reflecting both efficiency gains and regulatory influences [F1]. The company’s net income rebounded notably from a loss position in FY2022 ($-203 million) to positive territory at $440 million by FY2025 [F1], underscoring operational recovery.

Seasonality inherent to natural gas demand patterns—higher consumption during colder months—is largely mitigated by decoupled rate mechanisms embedded within the three states’ regulatory frameworks, stabilizing revenues against volume fluctuations [S4]. Moreover, the state commissions' oversight ensures that rates reflect cost of service alongside reasonable returns on invested capital via test years that incorporate adjustments for inflation and market variables.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 440 | 556 | 474 | +121.2% | ||

| 2024 | 199 | 1356 | 484 | +31.8% | ||

| 2023 | 5.4 | 151 | 509 | 418 | +9.6% | +174.2% |

| 2022 | 5.0 | -203 | 407 | -24 | +34.8% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 179 | -252 | 11.1 |

| 2024 | 178 | 410 | 5.7 |

| 2023 | 175 | -363 | 4.6 |

| 2022 | 161 | -452 | -6.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue for FY2024 & FY2025 explicitly referenced as 'not disclosed' in the latest XBRL snapshot but referenced in textual sources; percentage changes are approximate per reported trends.

Impact of the Centuri Divestiture: Focus Shift and Financial Recalibration

In August 2025, Southwest Gas completed the corporate deconsolidation of Centuri, its previously held Utility Infrastructure Services segment [S7]. This divestiture resulted in a strategic sharpening of focus exclusively on natural gas distribution operations across its core states—Arizona, Nevada, and California [N4]. The separation permitted streamlined financial reporting confined to regulated utilities metrics and allowed management to reallocate capital toward core infrastructure spending rather than diversified infrastructure services.

The simplification has implications for capital deployment priorities favoring upgrades and maintenance of gas pipelines supporting residential heating and commercial demand amid population growth trends characteristic of the Southwest U.S. region [S7]. Importantly, this move reduces exposure to non-regulated business risks associated with construction services previously under Centuri's umbrella.

Regulatory Frameworks and Decoupled Rates Enhancing Revenue Stability

Southwest Gas operates under a tightly regulated environment supervised by the Arizona Corporation Commission (ACC), Public Utilities Commission of Nevada (PUCN), California Public Utilities Commission (CPUC), with Federal Energy Regulatory Commission (FERC) oversight over certain transmission elements [S4][S13][S21]. Rates charged are established primarily via general rate cases employing cost-of-service models grounded in historic or projected test years.

Key to mitigating traditional utility revenue volatility is SWX's adoption of decoupling mechanisms prevalent in all three states but tailored per jurisdictional rules [S19]. These alternative revenue programs delink operating margin recovery from actual customer consumption volumes month-to-month by applying fixed margin allowances or customer-based amortizations varying seasonally. This arrangement cushions earnings from weather-driven consumption swings—a critical benefit given heightened domestic temperatures affect heating demand substantially.

The company also files Purchased Gas Adjustment (PGA) mechanisms reflecting pass-through commodity cost expenses subject to commission audit but excluded from margin calculations [S19]. Together, these tariff methods ensure stable regulation-aligned cash flows conducive for capital planning.

Customer Base Composition and Infrastructure Investment Trends

Approximately 85% of Southwest Gas’s operating margin derives from residential and small commercial customers—a diverse base minimizing single-customer revenue concentration risk [S4]. The remaining margin stems principally from transportation services (~11%) where large customers procure and transport third-party gas but contribute less proportionately to margins [S4]. In totality, SWX served roughly over two million customers as of end-2025 across its tri-state boundary with additions signifying organic expansion driven by regional economic development [S4][F1].

Infrastructure investment remains a linchpin supporting both customer growth accommodation and system reliability amidst aging assets typical of utility networks. Capital expenditures totaled approximately $808 million for FY2025—a decline versus prior year indicative of disciplined spending yet still substantial given sustained upgrades aligned with integrity management programs mandated by federal pipeline safety regulations [F1][S5]. Notably, capex reduction of about 14.6% YoY suggests optimization without compromising capacity extension or compliance requirements.

The consumption scale measure often tracked via dekatherms usage echoed stability with minor fluctuations commensurate with climate impacts yet did not disproportionately influence financial outcomes due to decoupled regulation [S4].

Capital Allocation Priorities: Balancing Capex, Cash Flows, and Dividends

Southwest Gas generates robust cash flow from operations exceeding $550 million as reported for FY2025 despite a notable decline relative to FY2024’s fiscal peak above $1.35 billion—likely attributable to working capital swings connected with purchased gas cost timing differences amidst volatile commodities pricing [F1].[N6][N7] Capex outlays absorb significant liquidity weight leading to negative free cash flow approximating -$252 million when subtracting capital spend from operating cash flow for FY2025.

Nonetheless, dividend payments maintained consistency totaling near $179 million distributed during the year supporting an attractive dividend yield near approximately 2.82%, confirming commitment to shareholder returns even amid capex investment cycles [F1][N6][N7]. No publicized share repurchase activity appeared within filings or disclosures suggesting current capital retention targeted toward infrastructure reinvestment rather than buybacks.

Estimated return on equity hovered at approximately 11.1%, signaling that equity invested into regulated rate base assets delivers satisfactory profit relative to industry expectations for utilities engaged in essential service provision combined with regulated cost recovery mechanisms [F1].

Financial Health: Debt Structure, Liquidity Metrics, and ROE Analysis

At December-end 2025 Southwest Gas exhibited sound liquidity indicated by a current ratio close to 1.28 derived from current assets around $1.19 billion against current liabilities near $930 million providing cushion against short-term obligations [F1][S6][S8][S9][S10]. The firm’s debt portfolio comprises multiple bond series extending through maturity dates spanning several years into the late-2030s–2050s timeframe featuring fixed-rate indebtedness consistent with long-dated utility financing enabling predictable interest expense management [S6][S8][S9][S10]. Revolving credit facilities provide additional flexible funding access aiding working capital requirements if needed.

Equity capital exceeded $3.96 billion as FY-end providing ample capitalization buffer while supporting credit metrics attractive for maintaining investment-grade status crucial in regulated utility sectors sensitive to borrowing costs given infrastructure cap intensity and regulatory cost recovery dynamics [F1][S8].

The approximate ROE near double-digit levels reinforces competent deployment of equity capital underpinning shareholder value generation within controlled risk parameters endorsed by regulators demanding reasonable returns for utility investors.

Future Outlook: Regulatory Risks and Growth Opportunities in Core Territories

Looking ahead, Southwest Gas’s financial trajectory remains anchored on regulatory developments particularly the timing and quantum of general rate relief awards managed under ACC, PUCN, CPUC frameworks [N9][S13][S17]. Delays or unfavorable rulings could constrict margin realization impacting short-term profitability despite underlying volume growth potential.

Conversely, demographic trends continue favoring geographic regions serviced especially Arizona’s expanding metro areas alongside Nevada's urbanizing sectors providing steady opportunities for incremental meter installations driving organic revenue gains supported by infrastructure expansion initiatives documented internally [N9]. Regulatory mechanisms designed explicitly maintain long-term earnings predictability mitigating commodity price pass-through challenges common elsewhere.

Prudent capital allocation complemented by effective tariff advocacy will remain critical focal points determining realized value creation balanced against maintaining compliance standards enforced federally especially regarding pipeline safety and environmental regulations which could impose cost pressures or accelerate expenditure timing.

Monitoring Milestones: Rate Relief Timings and Infrastructure Expansion

Absent explicit forward guidance on future quarterly or annual financials within public disclosures or news releases, stakeholders should monitor scheduled general rate case filings outcomes across Arizona Corporation Commission sessions plus Nevada PUC audits announced periodically as principal milestones influencing earnings trajectory analysis . Subsequent approvals related to Great Basin expansion projects or system integrity program enhancements will also warrant close attention given their prospective impacts on rate base escalation enabling additional revenue recovery opportunities.

Tracking utility commission notices alongside quarterly updates published can offer early signals regarding shifts in approved returns on equity or changes in decoupling formulas facilitating adjustments traders routinely incorporate into valuation assumptions.

This analysis is intended solely for informational purposes based on publicly available data as of February 25th, 2026; it does not constitute investment advice or recommendations regarding Southwest Gas Holdings' securities or market transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments