Titan Acquisition: Analyzing the Latest SPAC Financial Snapshot and Operational Trajectory

Titan Acquisition's recent quarterly filing reveals near-term liquidity challenges and underscores a critical juncture in its pursuit of a business combination.

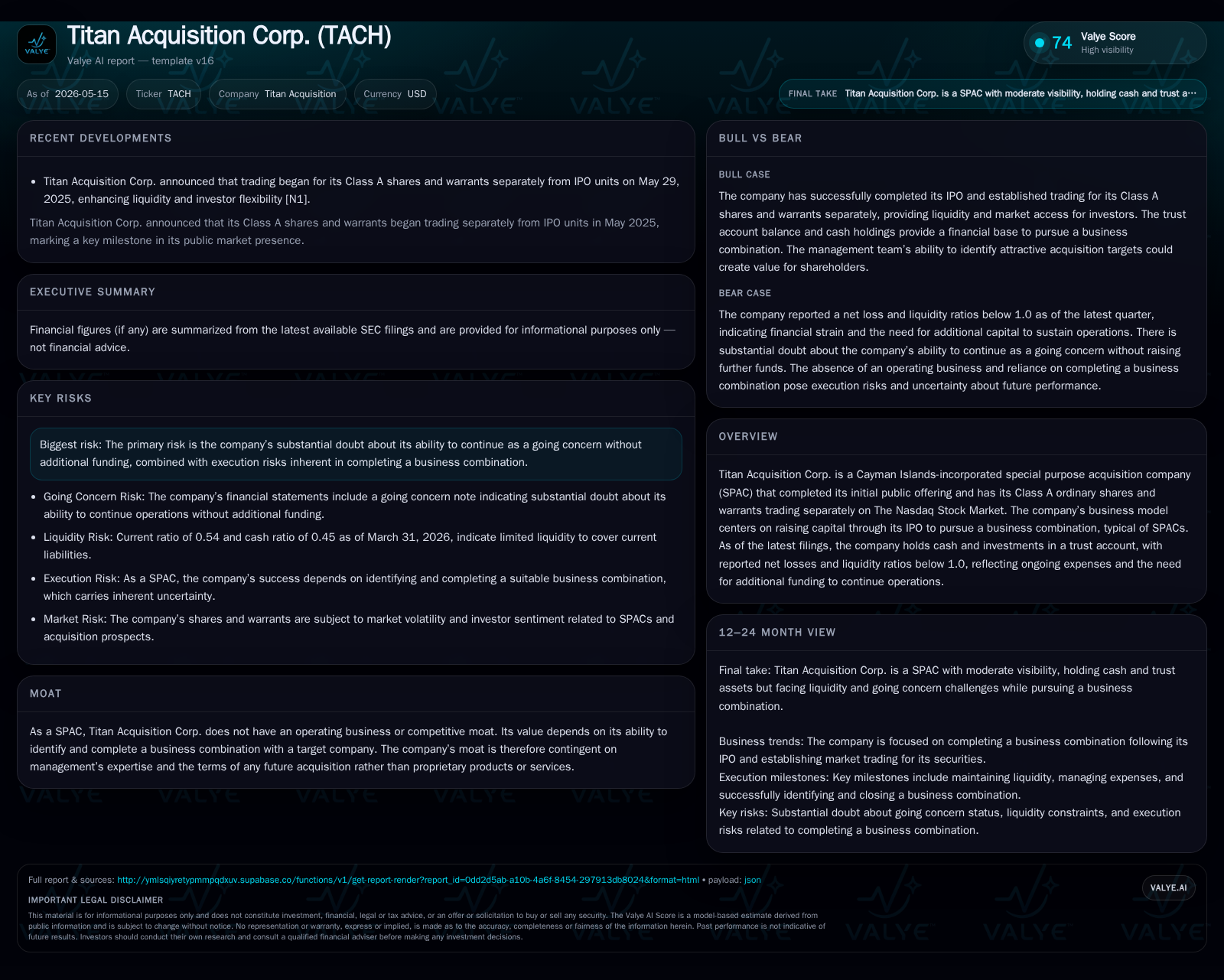

Titan Acquisition Corp., a Cayman Islands-based SPAC, reported its Q1 2026 results showing continued net losses and a current ratio of 0.54, signaling liquidity pressures. The company holds cash and investments in a trust account but faces substantial uncertainty regarding its ability to sustain operations without additional funding or completing a merger. Its value depends largely on management’s ability to identify and close a transformative business combination amid an increasingly competitive and scrutinized SPAC market. Key milestones ahead include target announcement, PIPE financing, and shareholder approvals that will determine its operational trajectory.

Latest Quarterly Operating Update Highlights

Titan Acquisition Corp.’s latest Form 10-Q filed on May 14, 2026 [S2] provides the most immediate insight into its operational footing entering mid-2026. The quarter ended March 31 reveals no material progress toward consummating a business combination — the core purpose of the SPAC structure. The current ratio stands at a concerning 0.54 [F1], indicating that current liabilities ($1.13 million) notably exceed current assets ($613 thousand). Cash and cash equivalents are reported at just over half a million dollars [F1], reflecting tight liquidity.

The company continues to incur net losses aligned with professional fees, administrative costs, and other operating expenses typical for SPACs pre-merger execution. The pattern of net losses without any operating revenue — unsurprising given the absence of an acquired operating business — underscores reliance on capital raised through initial public offerings and subsequent financings. Critically, there is no disclosed new acquisition or merger progress update within this filing period, maintaining the spotlight on Titan’s urgent need for capital infusion or completion of its intended combination to sustain operations.

Overview of Titan’s SPAC Business Model and Value Proposition

Titan Acquisition functions as a special purpose acquisition company (SPAC) incorporated in the Cayman Islands [S1]. Its business model is archetypal: it raises capital through an initial public offering (IPO), deposits these proceeds into a trust account segregated from general corporate funds, and seeks to identify a suitable private company for merger or acquisition within prescribed timeframes.

Class A ordinary shares and warrants trade separately on Nasdaq, providing investors exposure both to potential upside post-business combination and to dilution risks inherent in warrant exercise mechanics [S1]. The company does not generate operating revenues; instead, value creation depends entirely on management's ability to complete a value-accretive business combination under terms favorable enough to justify continued investor support.

The trust account acts as a financial backstop for redemption rights exercised by shareholders if they do not support the announced merger proposal. This mechanism ensures partial capital preservation but also imposes deadline pressures typically embedded within SPAC charters—pressures that loom large given Titan’s disclosed liquidity constraints.

Industry Context: SPAC Market Dynamics and Competitive Considerations

The broader SPAC ecosystem has undergone heightened scrutiny and increasing competition since the surge of IPOs several years prior [S1]. Thousands of SPAC vehicles currently compete to secure attractive targets amidst tighter regulatory oversight by the SEC focused on disclosure accuracy regarding projected PIPE financing commitments (private investment in public equity) tied to merger transactions.

Market skepticism toward speculative valuations post-merger has fueled increasing due diligence rigor, longer negotiation cycles, and elevated risk premiums demanded by investors participating in PIPE rounds or post-deal equity placements. These factors collectively compress pricing power for sponsors like Titan who offer no proprietary product or service platform but depend solely on their deal-sourcing skillset and sponsor reputation.

In this overcrowded field, differentiation is difficult; sponsors must rely on strategic relationships or sector focus to compete effectively. Absent such advantages—none clearly articulated by Titan—the entity’s survival hinges materially on speed and execution quality rather than structural competitive moats.

Key Growth Catalysts in the Business Combination Process

Titan’s growth prospects unfold almost exclusively through discrete transactional milestones. The first catalyst is the announcement of a definitive merger target, which can trigger share price appreciation by shifting speculative investor sentiment toward valuation based on underlying assets or ongoing operations post-combination.

Subsequent catalysts include securing PIPE financing commitments essential for deal funding beyond IPO proceeds held in trust. Successful placement often signals institutional investor confidence and reduces transaction uncertainty.

Finally, shareholder vote outcomes required to approve any proposed business combination constitute pivotal gating events dictating the company’s fate: approval leads into operational runway extension with new combined entity prospects; rejection risks liquidation or sponsor buyback maneuvers.

Monitoring proxy filings, investor presentations, and regulatory communications will provide clarity around Titan’s progress against these benchmarks.

Risks and Operational Constraints Facing Titan Now

The dominant risk emanates from cash flow insufficiency evidenced by the low current ratio (0.54) [F1] coupled with explicit management disclosures casting "substantial doubt" on the company’s ability to continue as a going concern absent successful financing or transaction completion [S1][S2]. Such phrasing signals material uncertainty about operational sustainability beyond short term horizons.

Time pressure inherent in SPAC governance structures compounds this risk; typically set deadlines require consummation of business combinations within one to two years post-IPO after which liquidation proceeds are distributed less sponsor incentives remain minimal or none at all. Failure to meet these deadlines may force unfavorable deal terms or dissolve investor value entirely.

Additionally, competition among numerous active SPACs dilutes access to quality targets while escalating bidding costs raises hurdles for accretive acquisitions. Regulatory intensity continues rising post-high profile failures impacting market receptivity toward new deals potentially imposing additional compliance costs or delaying approvals.

Investors should also note that fluctuating public market sentiment toward de-SPAC transactions could amplify volatility around Titan’s share price independent of fundamentals.

What Investors Should Monitor Next

Immediate areas warranting close attention include any announcements concerning new acquisition targets featured in upcoming quarterly reports or dedicated event filings ([S2]). Furthermore, updates on PIPE financing negotiations or finalizations provide critical visibility into deal viability.

Given that management reported no material changes in risk factors year-to-date [S2], investors must track whether evolving macroeconomic conditions or capital market environments prompt revisions alongside actual merger progress disclosures. Proxy statements ahead of any shareholder votes will deliver further directional cues regarding investor appetite and transaction structure.

Additionally, monitoring insider communications such as analyst calls or official presentations may reveal shifts in strategic posture—either fund-raising initiatives like convertible debt issuance or amended deal timelines—that influence short-term corporate sustainability prospects.

Current Financial Profile and Liquidity Assessment

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $504157 | |

| 2026-03-31 | ||

| Current assets | $613063 | |

| 2026-03-31 | ||

| Current liabilities | $1131685 | |

| 2026-03-31 | ||

| Current ratio | 0.54x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

A concise snapshot drawn from the March 31, 2026 balance sheet data summarizes Titan Acquisition’s liquidity status:

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 504,157 |

| Current Assets | 613,063 |

| Current Liabilities | 1,131,685 |

| Current Ratio | 0.54 |

These figures emphasize significant mismatch between liabilities due within one year versus readily available assets including cash reserves [F1]. Such structural liquidity inadequacy elevates refinancing risk absent imminent capital injections either through equity raises tied to announced mergers or alternative financing mechanisms documented in subsequent filings.

Disclaimer: This analysis is based strictly on publicly available SEC filings as cited up to May 15, 2026. It does not constitute investment advice but aims to provide an informed perspective on Titan Acquisition Corp.'s recent operating condition and strategic context within the SPAC sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments