Texas Capital Bancshares Expands Capital Return Amid Rising Interest Rates

Strong Q1 earnings and fresh dividend declaration highlight TCBI’s expanding capital returns and disciplined credit approach.

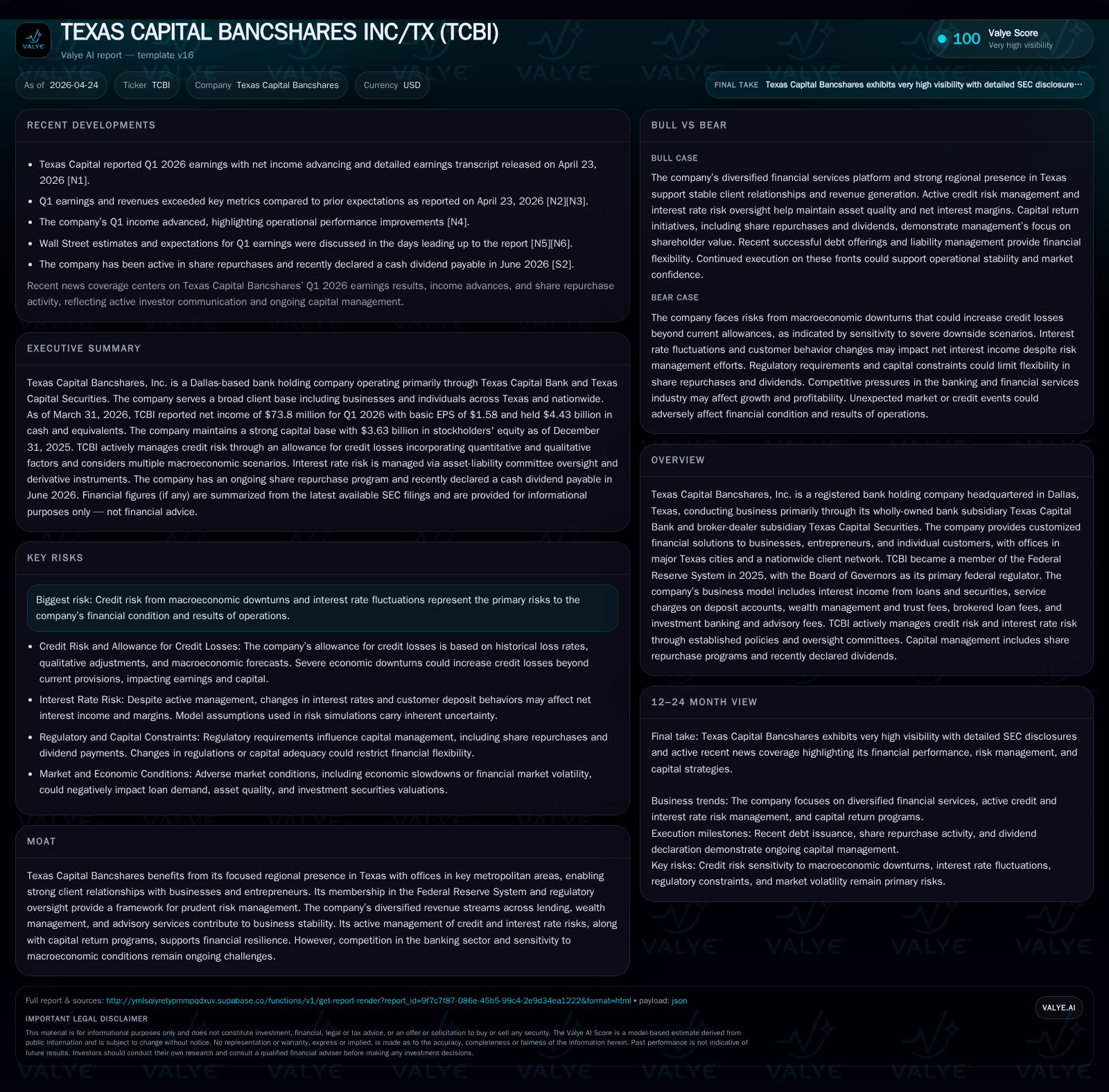

Texas Capital Bancshares, Inc. reported robust first-quarter 2026 results with net income gains supporting a new quarterly cash dividend and active share repurchase program. The company’s business model centers on customized lending to Texas-based businesses combined with diversified fee income from wealth management and advisory services. Regulatory developments, including Federal Reserve membership since late 2025, have tightened oversight but also underscore the firm’s prudential risk management. Growth continues to be driven by tailored loan offerings and expanding wealth management fees, although macroeconomic conditions and credit risk remain key constraints. Investors should watch for dividend payouts, buyback pace, and evolving credit metrics in upcoming quarters.

Latest Quarterly Operating Highlights and Capital Actions

Texas Capital Bancshares, Inc. (ticker: TCBI) released its first-quarter 2026 Form 10-Q on April 23, 2026 [S2]. The filing reveals meaningful progress in the company’s capital base with average shareholders' equity rising to approximately $3.7 billion from $3.4 billion in the same period last year. Reflecting improved profitability and confidence in cash flow stability, TCBI’s board declared a quarterly cash dividend of $0.20 per common share payable June 15, 2026 [S2], reversing the longstanding policy of no dividend payments since inception.

Complementing the dividend announcement, TCBI executed share repurchases under its refreshed authorization approved December 12, 2025. The company bought back around 770,000 shares for $75.1 million at an average price near $96.82 per share during Q1 [S2]. This activity is part of an overall repurchase program capped at $200 million through year-end 2026 that superseded prior repurchase authorizations [S2]. These capital return initiatives indicate a shift toward balancing growth investments against shareholder distributions.

Investor communications in related earnings calls corroborate these moves as supportive of earnings per share accretion while maintaining strong regulatory capital coverage [N1][N3]. Importantly, equity growth is fueled by operational performance rather than equity issuance dilution.

Business Model: Tailored Financial Services for Texas Entrepreneurs and Businesses

TCBI operates primarily through its wholly owned subsidiary Texas Capital Bank alongside its broker-dealer arm Texas Capital Securities [S1]. Its core revenue streams combine net interest income generated chiefly from commercial lending portfolios concentrated on small- to mid-sized enterprises across Texas metro markets with fee income from deposit servicing charges, wealth management trusts, loan brokerage fees, investment banking advisory services, and securities brokerage commissions.

The company’s business strategy emphasizes highly customized financial products designed to meet unique client needs particularly within key cities such as Dallas, Houston, Austin, San Antonio, and Fort Worth [S1]. This specialization has created durable client relationships facilitated by high-touch service models that increase switching costs relative to commoditized regional banks.

Supplemental digital banking platforms enable expanding reach beyond Texas borders for certain services while preserving the bank’s locally rooted identity [S1]. This diversity across interest-dependent income and fee-based revenue cushions earnings volatility against interest rate cycles.

Industry Positioning in Regional Banking and Regulatory Context

TCBI competes in a crowded Texas banking landscape featuring prominent challengers including other regional banks with substantial local footprints. Being Fed-regulated signals maturity in operational scale but also obliges more substantial governance frameworks and reporting standards [S1][S2]. TCBI balances these burdens effectively due to its existing conservative credit risk practices.

Pricing discipline remains critical given intense competition that pressures both loan yields and deposit costs; however, TCBI leverages its client intimacy to justify premium pricing on specialized lending products. Local economic health strongly influences performance due to concentrated geographical exposure.

Growth Drivers: Customized Loan Portfolio, Wealth Management, and Advisory Fees

Economic expansion in Texas metropolitan areas bolsters demand for tailored commercial loans targeting entrepreneurs and growing businesses—TCBI’s bread-and-butter market segment [S1][N1]. Customized credits often include complex structures that create sticky relationships fostering long-term client engagement.

Parallel growth ensues in wealth management as affluent clients increasingly seek trust administration and estate planning services delivered via Texas Capital Securities brokerage subsidiary. Fee income generated here provides stable margin contributions less sensitive to interest rate cycles [S1][F1].

Additionally, transactional advisory services related to mergers & acquisitions or debt structuring represent incremental revenue sources diversifying overall income streams [S1]. These fee revenues have gradually expanded alongside loan book growth contributing to steady top-line expansion despite periods of margin compression.

Constraints: Macroeconomic Sensitivities and Credit Risk Management

Despite solid fundamentals, TCBI faces ongoing risks tied to cyclical variations in borrower repayment capacity amid shifting economic conditions particularly affecting Texas sectors like energy or real estate development [S2][S10]. The company actively manages these risks with comprehensive credit policies incorporating extensive allowances for credit losses aligned with Accounting Standards Codification (ASC) Topic 326 requirements.

Management employs scenario analysis adjusting allowances materially if downside economic forecasts realize; recent disclosures suggest potential increases around $90 million under severe conditions absent qualitative overlays [S9][S10]. Such provisioning conservatism is crucial given the concentrated commercial real estate exposure embedded within the loan portfolio.

Interest rate fluctuations impose margin pressure as repricing mismatches between assets and liabilities moderate net interest margin expansion potential despite nominally rising short-term benchmark rates. The competitive environment further restrains pricing flexibility on deposits.

Regulatory capital buffers mandate deliberate retention of earnings limiting overly aggressive payout strategies during uncertain periods [S2][S13]. These elements collectively contour growth ceilings without compromising balance sheet strength.

What to Watch Next: Dividend Payouts, Share Repurchase Activity, and Credit Trends

Critical near-term milestones include observing successful execution of the newly declared cash dividend commencing June 15th which serves as a proxy for stable operating cash flows enabling shareholder distributions [S2][N1].

Similarly, measuring the pace of ongoing buybacks relative to the remaining authorized amount will reveal management’s appetite for capital return versus deploying funds into organic loan growth or acquisitions [S2][N3].

On the credit front, tracking changes in allowance for loan losses alongside quarterly net charge-off trends will provide early indicators of portfolio health amidst evolving economic headwinds particularly if stress manifests within targeted commercial real estate exposures [S2][S10].

Additionally, shifts in net interest margin during subsequent quarters will illuminate impacts from rate environments combined with competitive repricing dynamics.

Management commentary during forthcoming earnings calls may also shed light on strategic priorities such as geographic expansion or technology investment balancing growth with cost discipline initiatives.

Financial Overview: Capital Structure, Liquidity, and Operating Metrics

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 330 | 360 | 13 | +326.1% |

| 2024 | 78 | 481 | 65 | -59.0% |

| 2023 | 189 | 374 | 16 | -12.9% |

| 2022 | 217 | 148 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 186 | 348 | 9.1 |

| 2024 | 82 | 416 | 2.3 |

| 2023 | 105 | 357 | 5.9 |

| 2022 | 115 | 137 | 7.1 |

Source: SEC companyfacts cache [F1].

At quarter end March 31, 2026, total debt stood at approximately $878 million while shareholders’ equity averaged around $3.7 billion—up from $3.4 billion a year prior—illustrating solid capital base growth grounded primarily in retained earnings supported by profitable operations [S2][F1]. Net debt approximates a negative $3.55 billion given significant cash & equivalents holdings indicating robust liquidity [F1].

Net income surged notably to over $330 million for full-year 2025 compared to $77 million in prior year reflecting strong operational leverage though operating cash flow retracting by roughly a quarter warrants monitoring spending patterns outside core lending activities [F1].

Capital expenditures declined sharply in recent years pointing toward controlled reinvestment allowing free cash flow generation exceeding $347 million last fiscal year [F1], supporting aggressive buybacks totaling approximately $186 million in calendar 2025 alone underlining shareholder-friendly allocation policy [F1][S2].

Long term debt profile includes fixed-rate subordinated notes maturing through early-to-mid-2030s with refinancing optionality embedded especially notable after February 2026 issuance of nearly $400 million senior notes which helps extend maturity ladder and reduce near-term refinancing risk [S27][S28].

In summary, financial discipline enables simultaneous capital distribution via dividends/repurchases while maintaining excess regulatory buffers that fortify resilience against potential macroeconomic shocks.

This analysis is intended purely for informational purposes without any investment recommendation or advice. It reflects details incorporated from recent SEC filings and public disclosures alongside sector-informed assessment respecting disclosure boundaries.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments