Third Coast Bancshares Boosts Profitability Through Strategic Texas Expansion

The company’s focused operations in Texas markets, combined with diversified lending and capital efficiency, underpinned strong financial performance in 2025.

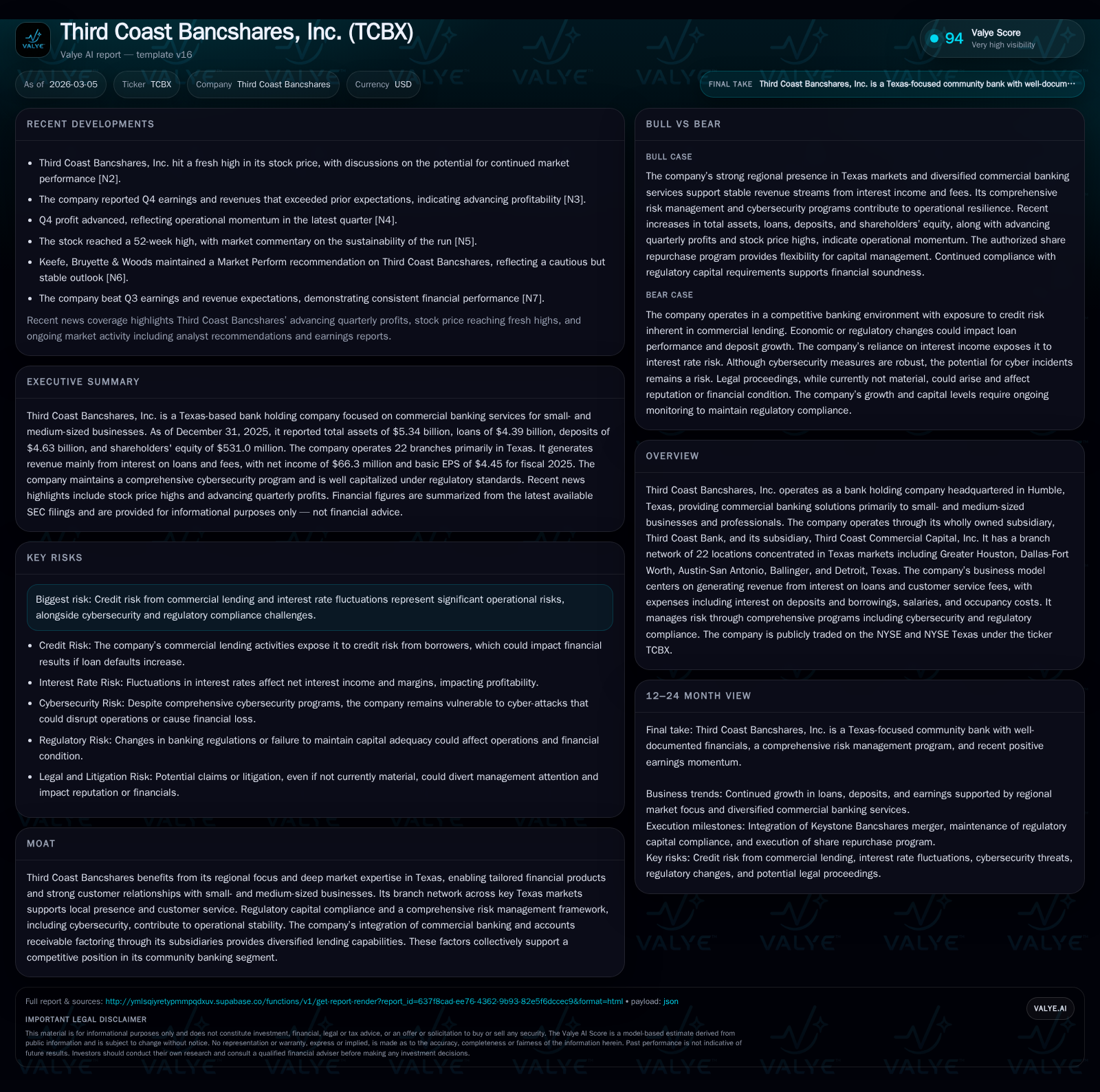

Third Coast Bancshares achieved a significant net income increase of 39.1% in 2025, driven by expansion in commercial and industrial loans and improved operating cash flow. Its deep Texas market expertise and integrated commercial banking with accounts receivable factoring support its competitive moat. The company's robust capital structure and disciplined capital allocation—including a new $30 million share repurchase authorization—are noteworthy as it manages credit risk and regulatory compliance. Stakeholders should closely watch loan growth trends, margin stability, and integration progress post the Keystone Bancshares merger as key growth drivers in 2026.

Financial Momentum: Historical Growth and Profit Drivers

Third Coast Bancshares delivered impressive financial results across fiscal 2025, underscoring its scalable business model concentrated on Texas regional markets. Net income rose from $47.7 million in 2024 to $66.3 million in 2025—a remarkable year-over-year increase of approximately 39.1% [F1]. This leap corresponds with improved operating cash flow that grew by close to 44.7% during the same period, from $35.1 million to over $50.8 million [F1]. Capex expenditures notably declined by almost half (-48.6%), suggesting prudent investment control or completion of major projects [F1].

Key drivers included robust loan portfolio expansions—especially commercial and industrial (C&I) loans—coupled with strategic fee income contributions from customer services and accounts receivable factoring offered through Third Coast Commercial Capital (TCCC) [S18]. Operating costs remained stable relative to revenue gains, benefiting from consistent salary management and occupancy efficiencies.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 66 | 51 | +39.1% | |

| 2024 | 48 | 35 | 2 | +392.0% |

| 2023 | 10 | 39 | 3 | +28.8% |

| 2022 | 8 | 22 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 12.5 | |

| 2024 | 33 | 10.3 |

| 2023 | 36 | 2.4 |

| 2022 | 10 | 2.0 |

Source: SEC companyfacts cache [F1].

*Note: The disproportionate net income jump in FY2024 was due to base effect from prior years' smaller scale.

The underlying asset quality improved concurrently with increases in total loans growing to approximately $4.35 billion by end-2025 from around $3.93 billion one year prior primarily driven by C&I loans which expanded by roughly 27.3% during the year—a testament to the bank's effective underwriting frameworks targeting retail trade and manufacturing small- to medium-sized enterprises [S8][S18]. Alongside growth initiatives was ongoing management of allowances for credit losses calibrated thoughtfully given sector exposures.

Leveraging Texas Markets: Business Model and Competitive Edge

Third Coast Bancshares commands a distinctive position through an intensely localized approach anchored within Texas’s key economic corridors—Greater Houston hosts nearly half its branches at ten locations—and expanding Dallas-Fort Worth plus Austin-San Antonio each contribute meaningful regional presence for focused outreach to small- and medium-sized businesses (SMBs) that require customized financial solutions [S17][S19].

This branch network synergy fosters deep client relationship management critical when assessing commercial real estate concentration risks inherent in business clientele loan books typical for community banks operating within localized ecosystems [S17]. Equally telling is the firm’s integrated lending platform combining traditional commercial banking lines of credit with factored receivables financing products deployed nationwide via its subsidiary TCCC—particularly servicing transportation-energy service customers who benefit from flexible working capital options anchored in invoice factoring—a niche seldom fully exploited by regional competitors [S18].

Capital discipline complements this strategy; regulatory capital ratios remain solidly compliant—Tier 1 leverage capital increased slightly to around 9.65% at year-end while common equity tier-1 ratio held firm at approximately 8.85%, comfortably exceeding Basel III standards associated with 'well-capitalized' status [S21][S26]. This balance suggests effective risk-weighted asset management alongside asset-liability structuring optimized for net interest margin preservation across varied interest rate cycles.

Recent merger activity also bolsters market positioning: the completed acquisition of Keystone Bancshares doubled branch density within key Texas metros providing synergistic scale advantages although integration complexity looms as a near-term challenge requiring focused management execution along loan portfolio harmonization lines as disclosed in early February filings [S3].

Assessing 2026 Outlook: Growth Catalysts and Headwinds

Looking ahead into calendar year 2026 discussions captured via earnings commentary articulate cautiously optimistic revenue growth prospects driven largely by organic loan demand overlaid with measured deposit growth efforts sustained through core deposit retention programs prioritized within fiduciary institutional relationships regionally based yet supplementing wholesale liquidity needs nationally [N3][N4][S3].

However potential caps emerge from macroeconomic uncertainties affecting energy sector clients predominant among factored receivables users plus general marketplace liquidity tightening reflected by rising cost of funds pressure inclusive of Federal Reserve rate hikes fueling higher deposit beta sensitivity impacting net interest margins.

Moreover regulatory vigilance persists around credit quality intensification risks especially as commercial real estate exposures remain sizable despite geographic diversification strategies coupled with increased competition from fintech lenders targeting similar SMB segments necessitating continued innovation around credit underwriting standards incorporating predictive analytics alongside prudent loss given default controls [S12].[N4]

The company reiterates no material changes in allowance policies or credit loss projections even amid these tensions but flags monitoring efforts amid evolving economic indicators within the Texas economy as paramount development areas influencing trajectory beyond current fiscal timelines.

Capital Efficiency: Balance Sheet Structure and Funding Sources

The Company's funding mix reveals sound structural elements supporting balance sheet expansion while preserving liquidity cushions requisite for uncertain periods typical of regional banks staffed modestly yet leveraging scalable funding stacks.

Deposits dominate at roughly $4.63 billion at end-2025 reflective of persistently high core deposits (~89% interest bearing), supplemented by brokered deposits held selectively above regulatory thresholds to optimize cost curves without materially increasing liquidity risk profiles—a sign of thoughtful asset-liability management sophistication often seen among top-tier community banks focusing on 'sticky' deposit franchises [S7][S23][S29].

Borrowings include a senior revolving line of credit capped at $55 million subject to prime-rate floors (currently yielding near-effective all-in costs ~6%) expiring March 2026 plus subordinated debt issuance via fixed-to-floating notes maturing mid-next decade (2032) carrying coupons around mid-single digits establishing stable long-dated funding allowing flexible capital treatment under Basel risk-based metrics enhancing Tier 2 qualifying buffers[S4][S5][S7].[S11]

Notably the company's Borrower-in-Custody arrangement approved by the Dallas Fed enables pledging commercial loan collateral for contingency Discount Window access up to ~$1.5 billion—a strategic liquidity backstop rarely leveraged yet critical for episodic stress test readiness fostering confidence among institutional investors respecting prudent contingency planning frameworks [S4][S10].[S27]

Distribution Strategy: Dividends versus Share Repurchase Plans

Third Coast Bancshares maintains a conservative yet shareholder-friendly capital allocation policy balancing dividend stability against reinvestment imperatives arising from ongoing credit extension ambitions.

Preferred stock dividends approximate $4.8 million annually reflecting steady payout commitments without compromising retained earnings growth essential for organic expansion; conversely common dividends remain modest calibrated against current ROE estimated near 12.5% derived via latest net income over shareholders’ equity data reinforcing sustainable payout levels cognizant of cyclical headwinds present across banking sectors nationally ([F1], S6).

Significantly a freshly authorized share repurchase program granting up to $30 million allowance was announced mid-2025 although no buybacks consummated during fiscal year end signaling selective opportunism aligned with valuation considerations or prevailing regulation guidance anticipations rather than immediate aggressive buyback tactics typical among larger counterparties [N1],[S9],[S13].

This disciplined capital return framework underscores prioritization of balanced financial flexibility catered toward absorptive capacity enhancement for future organic or acquisitive initiatives delivering shareholder value accretion sustainably.

Risk Oversight: Credit Exposure, Cybersecurity, and Compliance Framework

Robust risk governance permeates Third Coast Bancshares’ operational ethos evidenced by layered controls established atop conservative underwriting principles particularly given concentration exposure inherent in commercial real estate-heavy portfolios amplified inside regional community banking circles.

Credit risk mitigation reflects thorough borrower cash flow analysis centered on repayment capacity assessments complemented by collateral securing predominantly tied assets including inventories or accounts receivable subject often to personal guarantees enhancing loss mitigation reliability levels reducing potential LGD impacts under deteriorating scenarios encountered historically across localized downturns [S8],[S12],[S16],[S18].

On cybersecurity front the firm integrates a comprehensive NIST Cybersecurity Framework aligned program overseen directly by Chief Information Security Officer reporting upward through Risk Committee elevation ensuring board-level awareness aligning technology defenses against evolving threats while managing third-party vendor security via continual assessments minimizing extrinsic breach exposure pathways relative to operational stability mandates laid out transparently in annual SEC disclosures [S1],[S12].

Concurrent regulatory compliance adheres stringently throughout evolving federal oversight regimes reinforcing internal audit cycles plus rapid incident response protocols standing as pillars underpinning durable reputational safeguards critical amid intensifying digital transformation trends impacting banking.[S12]

What Investors Should Monitor: Strategic Milestones and Performance Metrics

Investors will find value tracking several pivotal indicators shaping Third Coast Bancshares’ near-term trajectory: loan portfolio growth rates particularly within C&I facilitating net interest margin sustenance; deposit mix evolution primarily noninterest vs interest-bearing proportions illustrating funding cost recalibration capabilities; progress seamlessly integrating Keystone Bancshares merger expanding branch network footprint; adherence to regulatory capital buffer maintenance amidst organic growth pressures; dynamic responses encapsulating continued share repurchase program deployment alongside dividend adjustments reflecting earnings momentum; finally shifts within credit risk parameters responding agilely to Texas market economic pulse including energy sector outlooks impacting factored receivables reliability [N3],[N4],[S3],[S21],[F1].

In sum Third Coast Bancshares stands poised leveraging regional expertise combined with coherent strategic execution demonstrating profitable scaling capabilities balanced carefully against measured risk tolerance environments typical among best practices community banks currently confronting multifaceted externalities alongside opportunity sets within vibrant Texas commercial landscapes.

This analysis is based entirely on disclosed company filings and publicly available data as of March 2026 without any forward-looking investment recommendations or speculative forecasts beyond stated reports.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments