Trulieve Cannabis Corp.’s Expansion and Financial Recovery Amid Regulatory Uncertainties

Trulieve solidifies its leading U.S. cannabis retail position through operational scale and strategic capital management while navigating a complex legal landscape.

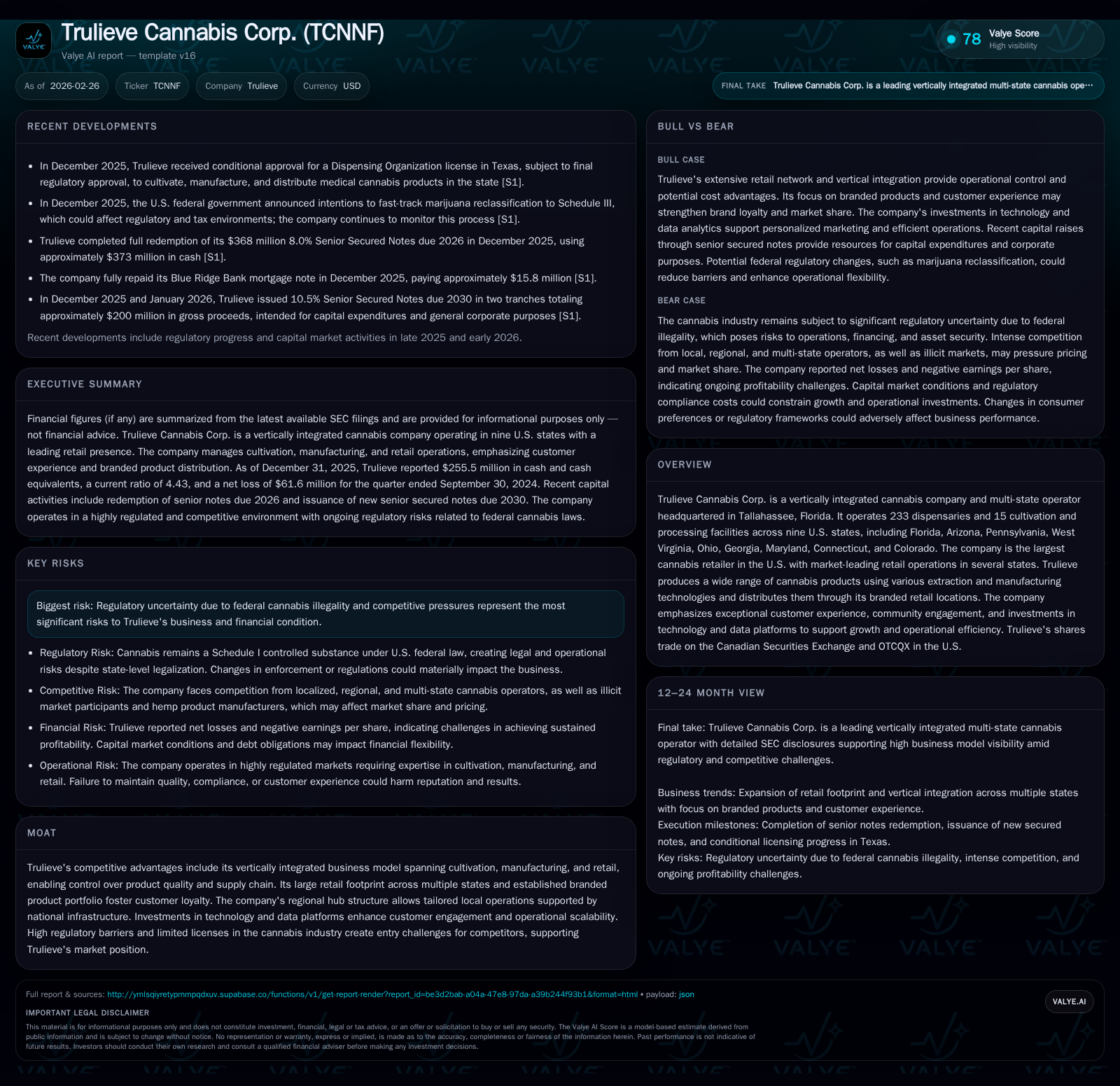

Trulieve Cannabis Corp. operates as the largest U.S. cannabis retailer with a vertically integrated, multi-state footprint spanning retail, cultivation, and manufacturing across nine states. After years of volatility, it posted significant operating income growth in 2025 driven by retail sales stability and operational efficiencies. The company’s prudent capital allocation included repaying high-cost debt and securing longer-term financing to support growth initiatives. Notwithstanding federal illegality risks, Trulieve leverages regulatory expertise, technology investments, and customer engagement to bolster competitive moats. Ongoing state-level legalization and potential Schedule III federal rescheduling underpin long-term prospects though competitive and compliance pressures remain salient.

Company Overview

Trulieve Cannabis Corp., headquartered in Tallahassee, Florida, has positioned itself as the largest cannabis retailer in the United States by operating over 230 dispensaries and 15 cultivation/processing facilities distributed mainly across nine states: Florida, Arizona, Pennsylvania, West Virginia, Ohio, Georgia, Maryland, Connecticut, and Colorado [S1][F1]. Its business model leverages vertical integration combining cultivation, extraction/manufacturing technologies (including supercritical ethanol, CO2 and hydrocarbon extraction), and branded retail distribution under a multi-state operator framework [S4][S9].

The company maintains regional hubs—in Southeast (anchored by Florida), Northeast (centered on Pennsylvania), and Southwest (anchored by Arizona)—to balance national infrastructure with tailored local operations accounting for diverse market regulations [S1][S9].

Historical Financial Performance

Trulieve's financial evolution reflects a transition from volatile results with net losses into growing profitability driven by retail dominance and operational efficiencies. Operating income reached $143.5 million in FY2025 representing a sharp 46.8% increase over FY2024 ($97.8 million) after an operating loss of $221.6 million in FY2023 [F1]. This turnaround underscores effective cost management alongside strong revenue generation primarily via retail sales approximately $1.11 billion in 2025 [S5].

Operating cash flow remained steady at about $272.8 million in FY2025 versus $271.5 million prior year despite capex dropping significantly from $121.5 million (FY2024) to $44.2 million (FY2025), indicating disciplined capital investment aligned with growth priorities [F1]. Net income remains challenged due to previous impairments and tax positions but is less negative than prior years.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | 273 | 143 | 44 |

| 2024 | 271 | 98 | 122 |

| 2023 | 202 | -222 | 40 |

| 2022 | 23 | 32 | 165 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 229 |

| 2024 | 150 |

| 2023 | 161 |

| 2022 | -142 |

Source: SEC companyfacts cache [F1].

Total revenue figures approximated from segment disclosures [S5]

Growth Drivers and Prospects

Trulieve’s growth depends on continuing expansion of its retail footprint within existing licensed states as well as new licenses under regulatory approvals (e.g., conditional approval received for Texas licensing in late 2025) [S15]. The normalization of regulated markets combined with broader adult-use legalization drives an expanding consumer base.

Investment in technology platforms facilitates customer acquisition and retention through sophisticated data analytics enabling personalized marketing campaigns and streamlined product availability across channels [S14][S21]. Their branded product portfolio spans premium brands such as Avenue and Muse down to value lines like Co2lors and Roll One enhancing market segmentation capabilities.

Potential federal reclassification to Schedule III status could be transformative—enabling banking access improvements, easing interstate commerce prohibitions in time, reducing tax burdens related to IRC Section 280E barriers thus improving margins indirectly [S6][S8][S11]. However, this remains uncertain pending regulatory processes now paused but active legislative interest continues.

Competitive pressures are mounting from both licensed operators scaling rapidly with deep pockets as well as illicit market alternatives still capturing non-traditional customers [S15]. Trulieve’s emphasis on community engagement including veteran and senior programs coupled with restorative justice initiatives aims to deepen loyal customer bases.

Capital Allocation and Financial Health

The company exhibits conservative liquidity metrics with over $255 million in cash and equivalents complemented by a current ratio exceeding 4x at year-end 2025 evidencing strong short-term financial flexibility [F1]. Operating cash flows consistently cover capital expenditures leaving robust free cash flow approximating $228 million post-capital spending for fiscal year ended December 31, 2025.

Notably, Trulieve redeemed its entire outstanding principal amount of its prior unsecured senior secured notes due in April 2026 with aggregate face value of $368 million during December 2025 at a total cash cost near $373 million reflecting accrued interest paid out early; such deleveraging enhances balance sheet stability though cost of borrowing increased with new issuance totaling roughly $200 million senior secured notes due in December 2030 bearing a coupon rate of approximately 10.5% per annum payable semi-annually [S11][F1].

This refinancing provides extended maturity horizons supporting ongoing capital expenditure plans mainly focusing on facility upgrades rather than heavy expansion seen previously given capex declined sharply year over year from over $120 million to about $44 million [F1][S27].

Dividend or buyback activity was not disclosed suggesting priority remains on reinvestment into the business and debt management rather than shareholder returns currently.

Regulatory Context & Risk Factors

Federal cannabis illegality persists as the predominant systemic risk shadowing Trulieve’s enterprise operations resulting in complex compliance regimes enforced at different jurisdictional levels; this includes limitations on interstate transport of products which necessitate localized vertical integration strategies per state hub system [S6][S20].

The company actively monitors changes including recent federal executive orders promoting cannabis research expansion aiming toward Schedule III reclassification; however procedural delays have stalled formal DEA rulemaking hearings indefinitely since early-2025 pending appeals though political momentum exists supported by bipartisan congressional acts such as the SAFER Banking Act yet to fully pass Senate floor votes [S7][S8][S16].

Trulieve’s governance includes mature cybersecurity oversight involving senior executives alongside board Audit Committees designed to minimize material operational risks including product safety recalls or data breaches impacting reputation or continuity [S1].

The extensive regulatory framework requires persistent attention to anti-money laundering statutes compliance given financial transactions involving cannabis proceeds face elevated scrutiny; hence banking relationships are limited primarily to state-chartered banks compliant with FinCEN guidance rather than traditional federal banking until legislative changes occur [S12][S24].

Legal contingencies include unresolved tax positions with potential liabilities totaling tens of millions noted without recognition thresholds met yet management anticipates contesting these penalties vigorously maintaining their tax standing assertions intact for now [S28]. Litigation exposure is moderate without material pending lawsuits affecting fundamental operations or licensing status but remains an inherent business risk given industry characteristics.

Industry Considerations & Competitive Moat Insight (Analysis)

The U.S.-cannabis industry remains fragmented due to state-by-state legalization creating barriers for nationwide scale which favors established multi-state operators like Trulieve possessing diversified geographic footprints paired with vertically integrated models controlling cultivation-to-retail supply chains tight quality standards as well as margin optimization levers uncommon among smaller players.

High entry barriers stem from restricted licensing caps limiting new competitors combined with regulatory scrutiny which raises the costs of compliance—delivering intrinsic protection for incumbents able to navigate complex systems effectively.

Moreover, evolving consumer preferences demand branded experiences that combine product consistency with educational outreach—a domain where Trulieve’s community engagement pillars centered around veterans/seniors coupled with digital loyalty platforms confer advantages supporting repeat customer monetization beyond raw product sales alone.

Seasonal promotional events anchored around cannabis culture dates provide lift opportunities but also require calibrated inventory planning which is enabled through investments into enterprise resource planning systems referenced internally facilitating allocation efficiency.

Milestones & What To Watch (Analysis)

Close monitoring will be warranted on three fronts: First, progress regarding FDA/DEA rescheduling directives impacting federal policy which would materially alter market dynamics including banking access expansions; second, successful license acquisitions such as final approval around Texas which opens a major new medical program; thirdly continued improvements in profitability metrics driven by scale benefits balanced against competitive pricing pressures especially if adult-use markets widen aggressively.

Furthermore, investor attention should track any shifts in debt terms or capital structure adjustments signaling financial flexibility adaptations amid macroeconomic cost-of-capital fluctuations given recently raised higher-coupon long-dated notes.

Last but not least are regulatory enforcement patterns particularly any narrowing of state or federal law tolerance that might necessitate rapid contingency planning or operational recalibrations especially considering long-standing ambiguity inherent within federally illegal activities even when compliant locally.

Conclusion

Trulieve Cannabis Corp has solidified its position as the dominant multi-state cannabis retailer integrating cultivation/processing capabilities enabling control over product quality whilst harnessing technology platforms supporting enhanced customer engagement yielding improved operating leverage visible in recent profitability gains. While substantial risks remain from federal illegality compounded by legislative uncertainties and intensifying competition within legalized markets—management’s focus on disciplined capital deployment alongside broadening geographic footprint underpinned by extensive regulatory governance frameworks appear well-placed to navigate ongoing challenges.

Investors should appraise Trulieve within this context prioritizing developments around policy evolutions, scaling capability progressions within newly accessible markets plus continued enhancement of operational cash flow generation capacity relative to cost structure management.

This analysis is intended for informational purposes only based on publicly available documents filed by Trulieve Cannabis Corp. It does not represent investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments