Tectonic Therapeutic Advances Clinical Pipeline Amid Growing Losses Supported by Strong Liquidity

Clinical-stage biopharma Tectonic Therapeutic progresses pulmonary hypertension therapies with expanded R&D investment balanced by robust financial resources.

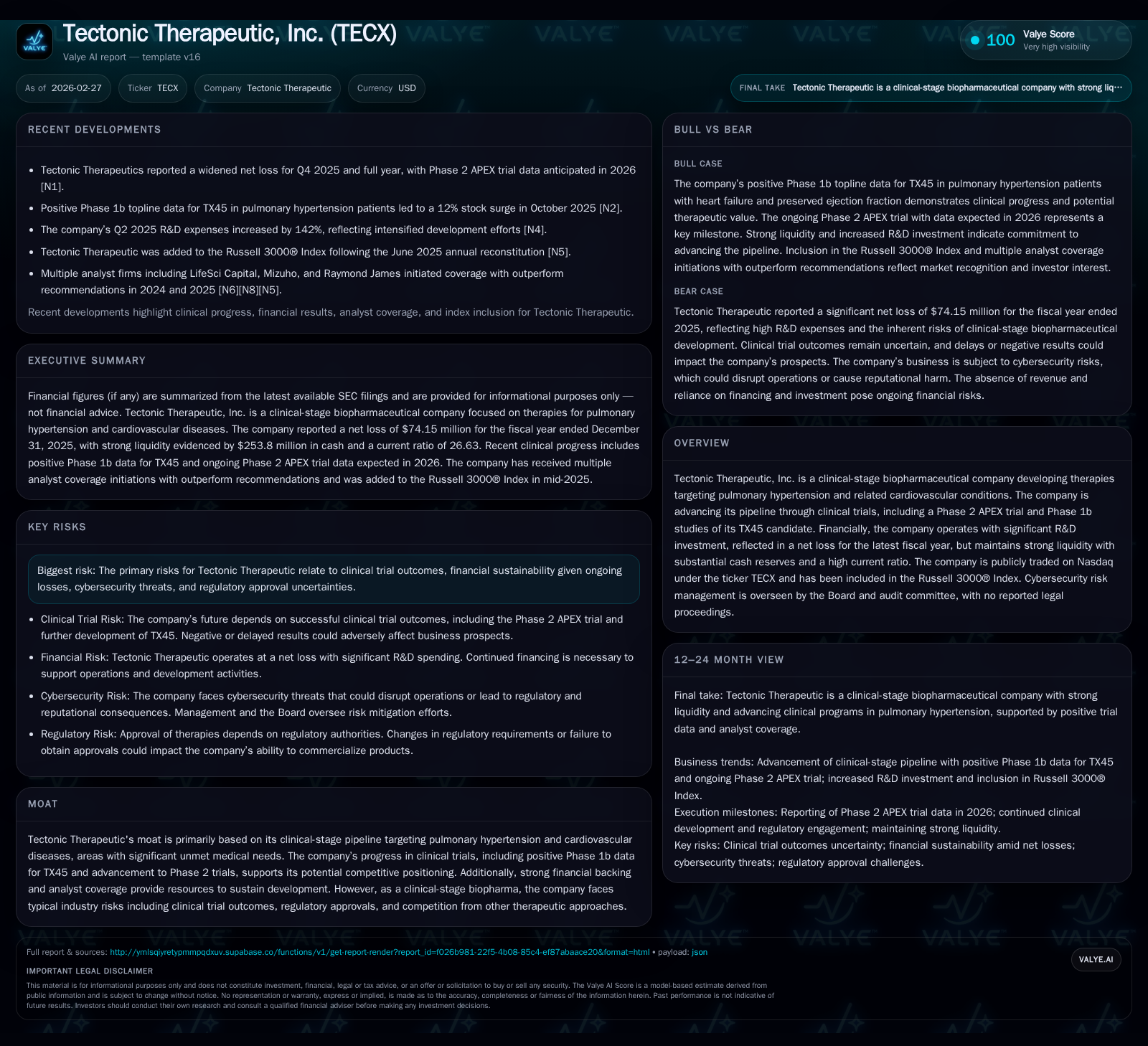

Tectonic Therapeutic, Inc. is a clinical-stage biopharmaceutical company focused on developing treatments for pulmonary hypertension and related cardiovascular diseases. The company's lead candidate, TX45, is advancing through a pivotal Phase 2 APEX trial with data expected in 2026. Financial results reveal widening net losses driven by increased R&D expenses, with FY2025 net loss of $74.15 million and operating loss of $84.04 million, reflecting deeper investment in clinical programs [F1]. Despite ongoing cash burn, the company maintains a strong liquidity position with cash and equivalents of $253.8 million and a current ratio above 26x at year-end 2025, providing a solid runway for continued development. Capital allocation prioritizes pipeline advancement without dividends or share repurchases reported [S21][S22][S23]. Governance enhancements include board expansion and appointment of an independent Chair to oversee strategic execution and risk management [S21][S22][S23].

Company Overview

Tectonic Therapeutic, Inc. is a clinical-stage biopharmaceutical company developing novel therapies for pulmonary hypertension (PH) and related cardiovascular diseases characterized by significant unmet medical needs. The company's lead asset, TX45, has advanced through early-phase studies into a pivotal Phase 2 APEX trial designed to assess efficacy endpoints critical for regulatory progression [N1][S3].

Operating within a competitive cardiovascular therapeutics landscape, Tectonic focuses on innovative mechanisms addressing vascular remodeling and hemodynamics without currently generating commercial revenues.

Historical Financial Performance

The company exhibits financial metrics typical of clinical-stage biotechs reliant on R&D investments:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -74 | -60 | -84 | 208000 | -27.9% |

| 2024 | -58 | -59 | -58 | 156000 | -576.9% |

| 2023 | 12 | -63 | 10 | 8000 | +111.5% |

| 2022 | -106 | -97 | -105 | 267000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -60 | -29.5 |

| 2024 | -59 | -41.2 |

| 2023 | -63 | 12.8 |

| 2022 | -97 | -140.5 |

Source: SEC companyfacts cache [F1].

[F1]

The positive operating income in FY2023 likely reflects unique accounting factors or timing differences during fluctuating clinical activity intensity.

Growth Drivers and Pipeline Progress

TX45's development underpins Tectonic's growth trajectory:

- Positive Phase 1b Part B data demonstrated hemodynamic improvements in patients with Group 2 PH associated with heart failure with reduced ejection fraction (HFrEF), validating the therapeutic approach [S18].

- The ongoing Phase 2 APEX trial aims to provide pivotal efficacy data during calendar year 2026 — a key inflection point for potential regulatory submissions and partnership discussions [N1][S3].

- Additional smaller-scale Phase 1b studies explore safety and tolerability across PH patient subsets.

Financial Outlook and Key Milestones

While explicit financial guidance is not detailed, important upcoming developments include:

- Timing and outcomes of the Phase 2 APEX trial data release.

- Monitoring operational burn rate relative to cash reserves given intensive late-stage clinical activities.

- Board changes including the appointment of Dr. François Nader as independent Chair may influence governance focus and capital strategy [S21][S22][S23].

Capital Allocation and Returns Analysis

Tectonic Therapeutic's capital deployment prioritizes pipeline advancement over shareholder returns:

- Return on equity approximates -29.5%, consistent with its pre-commercial status incurring high developmental costs [F1].

- Operating cash flows remain negative at around $60 million annually; capital expenditures are minimal compared to overall spend, highlighting investment emphasis on trials rather than fixed assets [F1].

- Cash & equivalents totaled $253.8 million at fiscal year-end with current liabilities below $10 million, resulting in an exceptionally strong current ratio above 26x, demonstrating ample liquidity for near-term operations [F1].

- No dividends or share repurchase programs have been announced or implemented [S21][S22][S23].

Governance and Risk Factors

Key risks typical of clinical-stage biopharma include:

- Uncertainties in clinical trial outcomes impacting regulatory approvals.

- Funding requirements dependent on successful capital raises before achieving revenue generation.

- Cybersecurity risks managed under Board audit committee oversight due to reliance on external CROs, CDMOs, and partners whose IT systems could affect operations or compliance [S1][S9].

- No material litigation reported reducing legal risk exposure currently [S4].

Recent governance updates saw the Board increase from six to seven members with the appointment of Dr. François Nader as independent Chair effective April 2026, potentially strengthening oversight amid growing organizational complexity [S21][S22][S23].

This report synthesizes factual financial data and disclosures concerning Tectonic Therapeutic as available through February 27, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments