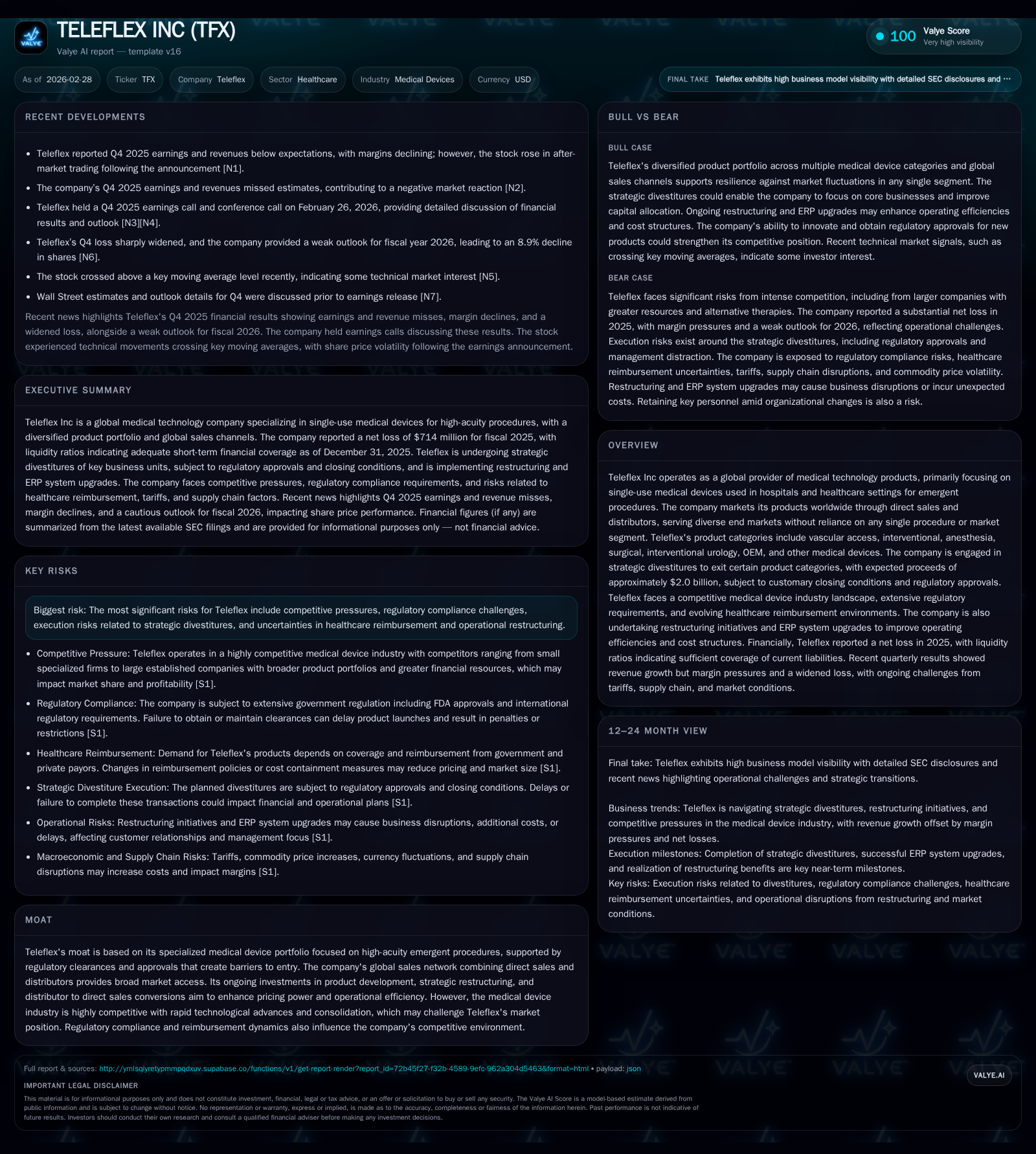

Teleflex’s Strategic Restructuring and Its Impact on Profitability and Growth

Teleflex's ambitious divestitures and operational shifts amid intense sector competition drove a stark earnings decline despite robust revenue gains in 2025.

In fiscal 2025, Teleflex experienced a pronounced disconnect between strong top-line growth and collapsing profitability, with revenue increasing 15.8% year-over-year yet net income plunging into a substantial loss. The company's ongoing strategic divestiture program aims to concentrate its portfolio on high-acuity single-use medical devices critical in emergent procedures but entails execution risks. Concurrently, margin compression from competitive pressures, regulatory costs, and reimbursement uncertainties challenges the operating model. Teleflex's capital structure remains solid with covenant compliance, sustained dividends, and significant share repurchases signaling management's commitment to shareholder returns despite free cash flow constraints. Investors should monitor the progress of divestitures and margin recovery as key indicators shaping fiscal 2026 prospects.

Revenue Growth and Earnings Volatility: FY2017 to FY2025

Teleflex’s historical trajectory reflects consistent revenue expansion over recent years, culminating in a significant acceleration to $1.99 billion in net revenues for fiscal 2025 — a step-up of approximately 15.8% year-over-year [F1]. This top-line momentum contrasts starkly with profitability metrics: operating income shrank over 90%, from roughly $151 million in 2024 down to just $13.9 million in 2025 [F1], while net income reversed dramatically from positive $69.7 million to a sizable loss of $714.3 million [F1]. The disproportionate decline indicates underlying cost pressures beyond mere sales fluctuations.

This divergence was influenced partly by the acquisition of the VI Business during the year, which contributed $202.4 million in revenues but also introduced integration complexities [N3][S3]. Additional contributory factors include margin contraction due to competitive pricing pressures, elevated compliance costs amid regulatory scrutiny, and costs linked to ongoing restructuring initiatives.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -714 | 97 | 14 | 95 | -1125.2% |

| 2024 | 70 | 638 | 151 | 126 | -80.4% |

| 2023 | 356 | 512 | 506 | 91 | -1.9% |

| 2022 | 363 | 343 | 500 | 79 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 60 | 300 | 1 |

| 2024 | 64 | 200 | 512 |

| 2023 | 64 | 420 | |

| 2022 | 64 | 264 |

Source: SEC companyfacts cache [F1].

Note: FY2017 revenue baseline is included for historical context; detailed operating incomes before FY2022 are limited.

Strategic Divestitures Reshaping Core Business Focus

The company has embarked on an extensive strategic restructuring to concentrate its efforts around core specialized product lines centered on single-use devices employed primarily in emergent medical procedures such as vascular access and anesthesia [S1][N3]. To that end, Teleflex announced plans for multi-billion dollar asset divestitures, targeting proceeds near $2 billion contingent upon customary closing conditions and regulatory approvals [S3]. This reduction in peripheral product categories is intended to sharpen focus on high-moat niches guarded by regulatory clearances, reducing exposure to commoditized markets.

However, this process introduces inherent execution risks including integration timing, potential customer attrition within divested segments, and temporary operational inefficiencies [N3]. Management acknowledged these challenges on the latest earnings call but underscored confidence that these moves would ultimately enhance pricing power by streamlining the sales channels—partly through shifting from distributor relationships toward direct selling models—fostering better control over market access [N3].

Operating Margins Pressured by Competitive and Regulatory Challenges

Margin compression remains acute amid intensifying competition both from legacy medical device firms and newer entrants leveraging advanced technologies [S1][N10]. Rapid innovation cycles necessitate ongoing R&D investments that stress cost structures without immediate revenue offset [S10]. Pricing power is further eroded by volatile healthcare reimbursement policies across geographies where government payors limit procedure volumes or impose stricter pricing regimes, directly impacting demand for devices used predominantly in emergent care settings [S10][N1].

Additionally, Teleflex faces increased costs related to compliance with evolving regulations such as the EU Medical Device Regulation (EU MDR) implemented recently, demanding more extensive product validation and post-market surveillance efforts that inflate overheads [S10][N2]. The company’s product mix sensitivity amplifies earnings volatility since higher-margin new products face longer development timelines under such scrutiny.

Capital Structure, Liquidity, and Compliance with Debt Covenants

At year-end 2025, Teleflex maintained a robust liquidity position with approximately $379 million in cash and equivalents globally held including significant non-U.S. balances [$208 million] [F1][S6]. The firm secured financing flexibility through a revolving credit facility capped at $1 billion alongside delayed draw term loan commitments totaling $700 million drawn mid-2025 to fund the VI Business acquisition [S4][S5][S6].

The company’s outstanding senior notes issued in prior years mature in late-2027 and late-2028 respectively totaling $1 billion principal amount with standard covenants limiting liens, asset sales, and indebtedness levels [S4][S11]. As of December 31, 2025, all debt covenants including maximum total net leverage ratio capped at 4.50x and minimum interest coverage ratio of 3.50x were met comfortably amid earnings pressure given conservative capital management strategies [S4][S11].

Accounts receivable securitization facilities provide additional short-term working capital agility up to $75 million; this capacity was fully utilized at year-end under terms free of covenant breaches or termination events [S8].

Cash Flow Trends versus Capital Expenditure Patterns

Operating cash flow plummeted nearly 85% year-over-year from $638 million in FY2024 down to approximately $97 million in FY2025 reflecting strained profitability and working capital usage dynamics [F1]. Capital expenditures declined moderately (-24.7%) signaling prudence on investments amid uncertain growth outlooks though still exceeding $95 million spent aimed partly at sustaining product innovation pipelines crucial for emergent procedure devices where technology differentiation can command premium pricing [F1].

This convergence resulted in negligible free cash flow generation estimated near $1.4 million for the year after deducting capex from CFO — raising questions about funding internal growth organically without increasing leverage or diluting returns through aggressive capital deployment [F1].

Dividend Policy and Share Buybacks: Balancing Returns and Resource Needs

Remarkably, Teleflex sustained dividend payments around $60 million annually despite recording substantial net losses — reflecting management’s resolve toward maintaining shareholder income streams during turbulent periods [F1][N8]. Parallelly, share repurchase activities intensified with $300 million deployed under accelerated share buybacks during the fiscal year compared with $200 million in the prior period supporting equity prices amid broader market uncertainty [F1][S22].

This dual approach underscores a delicate balancing act: preserving confidence through payouts while judiciously managing scarce cash resources owing to operational headwinds and restructuring costs.

Looking Ahead: What to Watch in Teleflex’s FY2026 Outlook

Going forward into FY2026, key performance barometers will hinge on the successful completion of planned divestitures enabling sharper concentration on higher-margin single-use emergent devices which constitute Teleflex’s competitive advantage bolstered by regulatory approvals forming entry barriers [N3][S3]. Monitoring margin trends amidst lingering reimbursement volatility is critical given past erosion.

Additionally, tracking operating cash flow recovery will indicate whether cost mitigation efforts paired with optimized sales channels translate into free cash flow growth necessary for sustainable capital returns absent incremental debt raising measures [N8][S22]. Regulatory developments especially post-EU MDR adjustments remain watchpoints due to their influence on product development cadence.

Overall, while strategic restructuring places Teleflex on firmer foundation focused around technological differentiation in urgent care segments resilient against commoditization risks, interim disruptions pose material operational challenges requiring attentive oversight.

This analysis presents factual information from publicly filed sources without offering investment advice or recommendations. Readers should consider multiple factors beyond those discussed herein when evaluating Teleflex’s business trajectory.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments