Talen Energy’s Shift to Carbon-Free Generation Strains Financials Amid Operational and Regulatory Challenges

Talen Energy balances growth from clean energy assets with heavy indebtedness and operational setbacks in 2025.

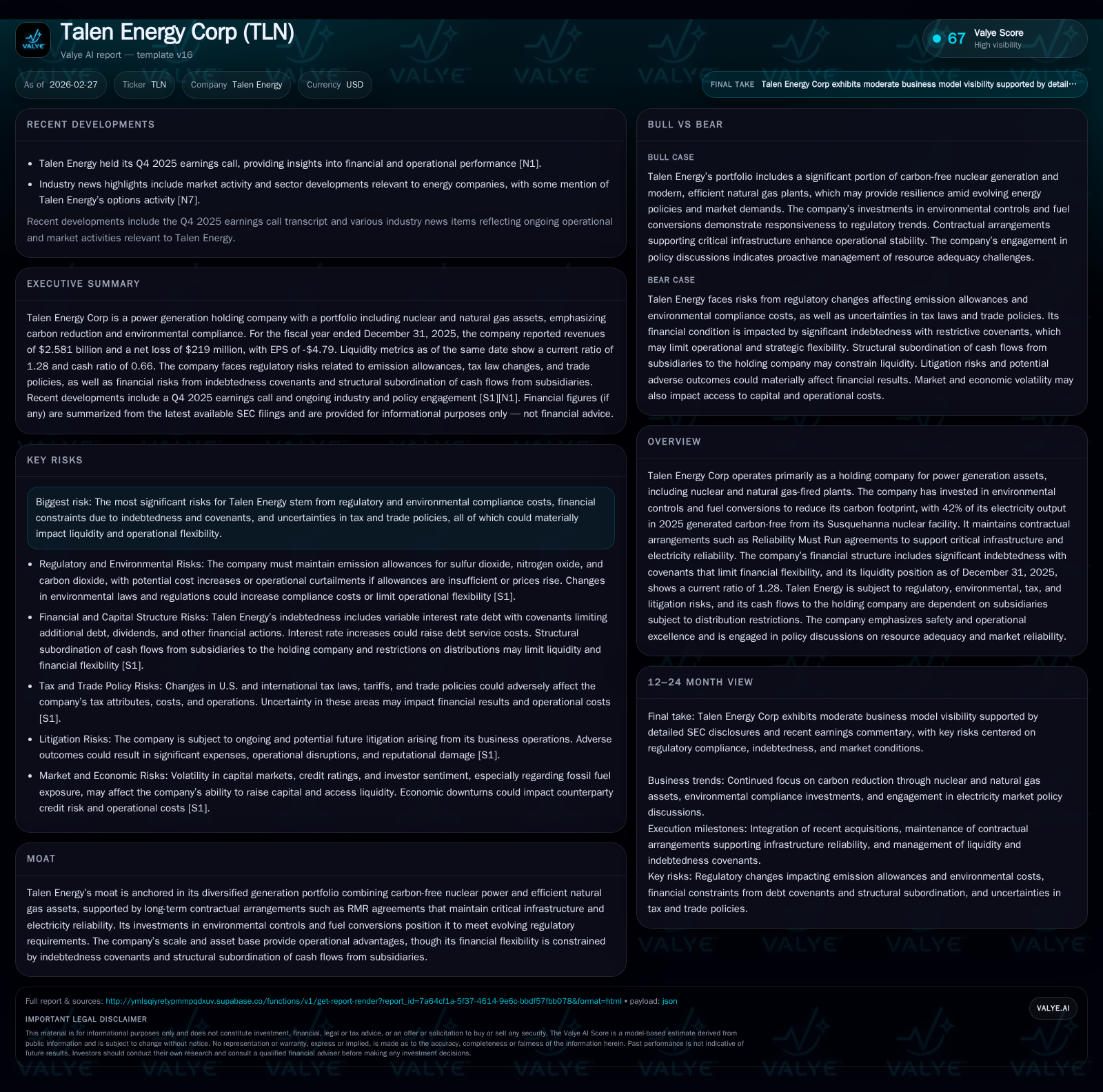

In 2025, Talen Energy Corp expanded its carbon-free electricity output to 42%, leveraging its Susquehanna nuclear facility and natural gas portfolio while navigating complex environmental regulations. The company grew revenues by 22% year-over-year but saw a sharp downturn in operating and net income due primarily to higher costs and negative operating performance. Its financial structure remains burdened by substantial debt and restrictive covenants that limit flexibility, with dividend payments and buybacks correspondingly reduced. Future growth depends on successful integration of recent acquisitions, regulatory outcomes, and the company’s ability to sustain cash flow generation under tightening compliance demands.

Historical Performance

Talen Energy Corp reported revenue of approximately $2.58 billion for fiscal year 2025, marking a robust year-over-year growth of about 22% from $2.12 billion in 2024 [F1]. This revenue expansion aligns with the company's strategic augmentation of its generation portfolio through acquisitions such as the Freedom and Guernsey plants, adding roughly 2.8 GW of modern natural gas-fired capacity that complements existing nuclear assets.

However, the topline strength masked operational challenges: operating income deteriorated sharply from a positive $226 million in 2024 to a loss of $90 million in 2025 [F1]. This represents a nearly 140% decline year-over-year—largely attributed to increased regulatory compliance costs, elevated emissions allowance expenses particularly for coal-fired operations like Colstrip, and heightened operational risks outlined in regulatory filings [S1][S27]. Net income followed suit with a steep swing to a net loss of $219 million in 2025 from profitable prior periods [F1].

Despite the profitability setbacks, Talen’s operating cash flow more than doubled compared with the prior year to $704 million [F1], underscoring improved cash generation likely stemming from contractual arrangements such as Reliability Must Run (RMR) agreements which provide steady revenue streams under grid reliability mandates [S1]. Capital expenditures remained disciplined at $98 million—modest against previous years which saw significantly higher spending—indicating a focus on maintaining existing assets and selective environmental upgrades rather than large-scale new buildout [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 2.6 | -219 | 704 | -90 | +22.0% |

| 2024 | 2.1 | 256 | 226 | ||

| 2015 | -62 | 768 | 94 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 103 | 606 | -20.0 |

| 2024 | 1958 | 171 | |

| 2015 | 317 | -1.4 |

Source: SEC companyfacts cache [F1].

Note: Dividend payments are limited due to debt covenants; buybacks sharply reduced compared to prior year.

Portfolio Composition and Growth Drivers

Talen’s asset base blends nuclear power — chiefly its Susquehanna facility — generating approximately 42% of the company's electricity output carbon-free as of 2025 [S1][S20]. This positions Talen well within evolving market trends favoring decarbonization while retaining baseload reliability. The addition of efficient combined cycle gas plants through recent acquisitions further complements this trajectory by enhancing operational flexibility and mitigating coal reliance.

Significant investments have been made in environmental controls and fuel conversions at existing fossil-fuel plants including Brunner Island, Montour, and H.A. Wagner to lower carbon intensity [S20], aligning with stringent EPA regulatory demands like the revised greenhouse gas rules instituted in recent years. Nonetheless, coal-fired operations remain challenged by potentially costly compliance regimes such as the Clean Air Act's emission allowances for nitrogen oxides and sulfur dioxide [S27].

Contractual arrangements such as RMR agreements insulate portions of Talen's revenue streams by securing payment for essential grid reliability capacity unaffected by market price volatility or generation outages [S1]. Additionally, amended Power Purchase Agreements (PPAs) with major consumers reflect strategic repositioning against regulatory scrutiny on behind- vs front-of-meter power supply constructs [S1].

Financial Structure and Capital Allocation

Talen operates principally as a holding company dependent on distributions from subsidiaries engaged in power generation operations. These subsidiaries carry significant indebtedness secured through credit facilities containing strict covenants restricting TEC’s financial flexibility [S4][S6][S9]. Such covenants limit additional borrowing, asset sales, dividend payments, share repurchases (which declined from nearly $2 billion in 2024 to about $103 million in 2025), mergers, or other corporate activities without lender approval.

At fiscal year-end 2025, Talen held approximately $689 million in cash equivalents with current assets totaling about $1.35 billion against current liabilities near $1.05 billion—yielding a current ratio around 1.28 [F1], reflecting reasonable near-term liquidity but limited cushion given obligations.

Free cash flow (operating cash flow less capex) was substantial at approximately $606 million in 2025, supporting internal funding capacity despite negative profitability results [F1]. However, distribution restrictions linked to subsidiary debt agreements constrain dividend payments; these are contingent on EBITDA performance ratios or fixed charge coverage tests [S13][S16][S17], resulting in minimal or no common stock dividends recently.

The company faces refinancing risks exacerbated by variable-rate borrowings under Credit Facilities sensitive to rising interest rates [S4][S6]. Collateral requirements tied to derivative hedging can also pressure liquidity during volatile market conditions [S15].

Regulatory, Environmental & Legal Risks

Talen faces numerous risks from federal and state environmental regulations covering emission allowances for sulfur dioxide, nitrogen oxides, carbon dioxide; water discharge limits under EPA ELG Rule; waste management statutes including CERCLA; and emerging climate policies [S1][S27][S29]. Ongoing legal challenges against some EPA rules introduce uncertainty regarding compliance costs and potential premature unit retirements or operational curtailments.

Coal facilities such as Colstrip are under heightened scrutiny due to revised greenhouse gas standards potentially affecting economic viability absent mitigation measures [S27]. Tariff or trade policy changes may elevate fuel or material costs impacting plant economics [S23].

Legal proceedings also involve disputes over interconnection agreements influencing power delivery contracts with major customers like AWS [S1]. Unfavorable rulings could materially affect contracted revenues.

Operational vigilance is required for hazardous materials handling related to fossil fuel wastes alongside adherence to occupational health and safety regulations to avoid financial penalties or reputational harm [S20][S29].

Outlook: Growth Prospects & Key Milestones

Growth drivers include integration of acquired efficient natural gas assets boosting baseload capacity; progress toward cleaner fuels reducing emissions liabilities; maintenance or renewal of RMR agreements providing cash flow stability; resolution of FERC litigation affecting PJM tariff structures; and potential benefits from government incentives such as the Nuclear PTC program pending legislative stability [N1][S23][S27].

Constraints may arise if regulatory compliance costs escalate unpredictably or if merchant market pricing weakens fossil fuel unit economics. Debt covenant restrictions will continue limiting capital deployment options including dividends or acquisitions.

No explicit forward guidance has been published; monitoring quarterly earnings for margin shifts, liquidity metrics like leverage ratios and fixed charge coverage, capex aligned with sustainability goals, legal resolution timelines regarding interconnection disputes, and regulatory updates on EPA emissions rules will be crucial for assessing trajectory [N1][N5].

Summary

Talen Energy is navigating a complex transition balancing expanded low-carbon footprint via nuclear assets and efficient natural gas plants against legacy fossil fuel challenges amid evolving environmental regulations. While revenue growth underscores commercial momentum supported by acquisitions and firm contracts underpinning grid reliability, profit declines highlight cost pressures intensified by compliance demands.

Robust cash flow generation provides some buffer enabling disciplined capital spending but debt servicing requirements coupled with restrictive covenants constrain financial flexibility—as reflected by sharply curtailed share repurchases and constrained dividend prospects. Ongoing regulatory uncertainties including EPA rule appeals plus litigation affecting contracted power flows will shape near-term corporate momentum between sustainable growth efforts versus financial constraints.

Disclaimer:

This analysis is prepared solely for informational purposes without any recommendation regarding securities of Talen Energy Corp. It reflects current factual data up to February 27, 2026 based on public disclosures. Readers should conduct their own due diligence before making investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments