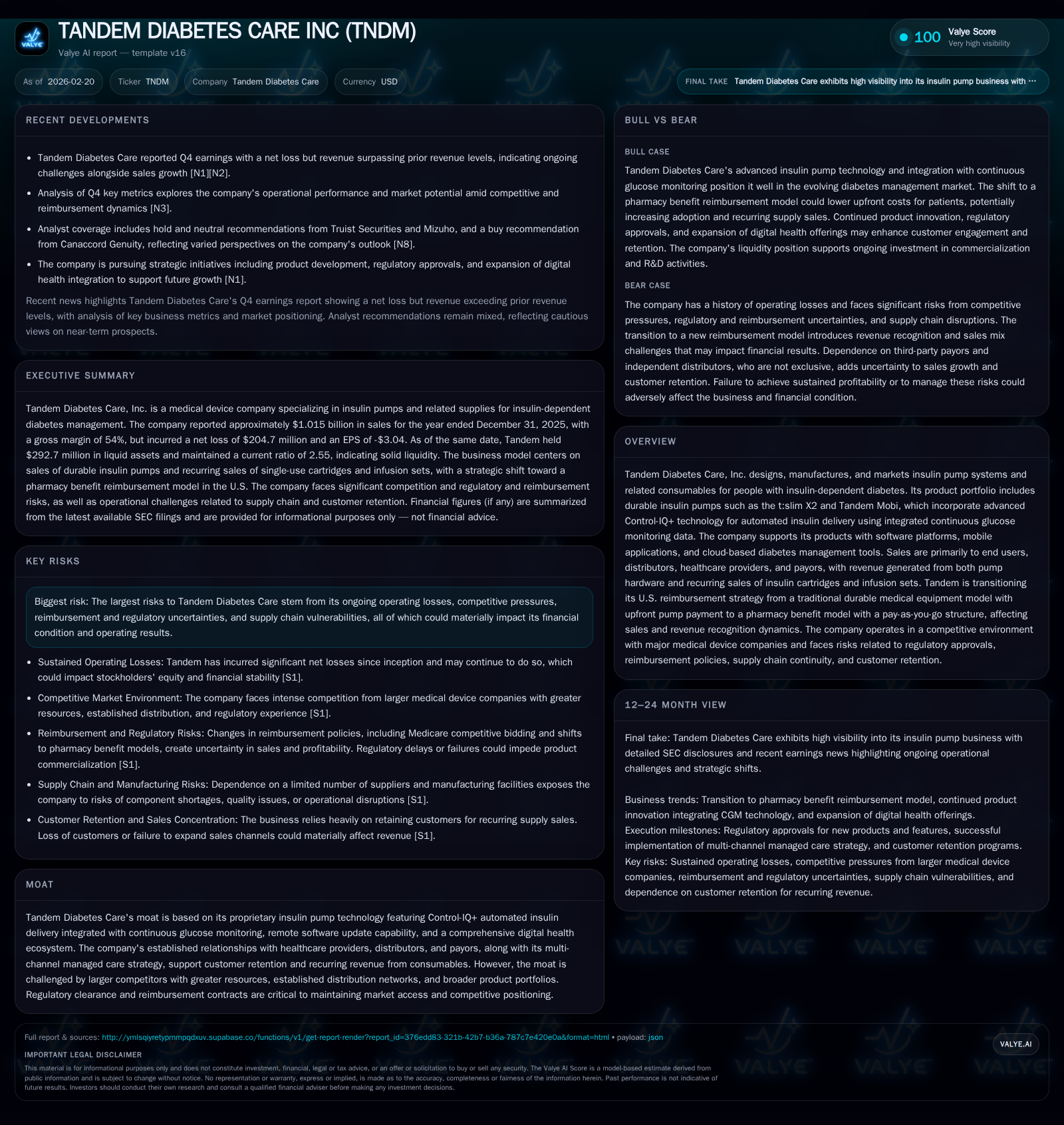

Tandem Diabetes Care Inc Harnesses Innovation Amidst Financial Strain

Tandem Diabetes Care balances cutting-edge diabetes management technology with ongoing financial pressures during a strategic reimbursement transition.

Tandem Diabetes Care has demonstrated a notable turnaround in operating income, shifting from significant losses to modest profitability by 2025, driven by expanded product adoption and technology integration. However, net losses persist due to elevated R&D and SG&A spending amid a strategic pivot in U.S. reimbursement from upfront pump sales under a durable medical equipment model to a pay-as-you-go pharmacy benefit model. The company’s competitive moat relies heavily on its Control-IQ+ insulin delivery system integrated with continuous glucose monitoring and a digital health ecosystem, yet faces growing pressure from larger rivals and reimbursement uncertainties. Capital allocation favors sustained R&D investment over shareholder returns, reflecting the need to innovate in a complex regulatory and market environment.

Evolution of Tandem’s Growth: Historical Performance and Profitability Trends

From FY2022 through FY2025, Tandem Diabetes Care displayed a marked improvement in operating income but still grappled with net losses and volatile cash flows [F1]. Operating income rose sharply from a loss of approximately $17.8 million in 2022 to an $8.3 million profit in 2025—a nearly fivefold turnaround indicating better cost management or higher-margin product mix improvements. However, net income reveals persistent challenges with a small net loss of $0.6 million recorded in 2025 after a positive swing in 2024's $0.75 million net income that proved unsustainable. This volatility underscores the company's ongoing struggle to convert operational gains into bottom-line profitability.

Operating cash flow (CFO) data portrays an inconsistent trend characterized by positive inflows in 2022 and 2024 but a negative swing turning CFO negative by roughly $9.7 million in 2025 [F1]. The resulting free cash flow (FCF), approximated by subtracting capital expenditures (Capex) from CFO, remained negative near -$29.7 million in 2025 due to Capex levels holding steady around $19 million after prior higher expenditures.

The company’s equity base contracted rapidly during this period as recurring losses eroded shareholders' equity from $440 million in 2022 to $155 million by the end of 2025. Consequently, approximate return on equity (ROE) was slightly negative (-0.4%) despite recent operating income gains, highlighting the lingering impact of accumulated deficits [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -10 | 8 | 20 | -178.0% |

| 2024 | 1 | 24 | -1 | 19 | +102.5% |

| 2023 | -30 | -32 | -35 | 27 | -89.3% |

| 2022 | -16 | 50 | -18 | 34 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -30 | -0.4 |

| 2024 | 30 | 5 | 0.3 |

| 2023 | -59 | -9.6 | |

| 2022 | 16 | -3.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue unavailable; YoY figures for OpInc, Net Income, CFO, Capex computed when sufficient data points exist.

Technological Differentiation: Control-IQ+ and Digital Health Ecosystem as Moat Drivers

Tandem’s primary source of differentiation lies in its proprietary insulin pump systems— notably the t:slim X2 and Tandem Mobi—which integrate advanced Control-IQ+ automated insulin delivery algorithms linked with real-time continuous glucose monitoring (CGM) data [S7]. This closed-loop system enhances glycemic control while reducing hypoglycemia risk through predictive algorithms that automatically adjust insulin delivery.

What further fortifies Tandem's competitive position is the ability to deliver remote software updates to devices post-sale, creating a dynamic feature upgrade path akin to consumer electronics paradigms [S7]. This updateability extends device lifespan and user experience without necessitating hardware replacements.

Complementing hardware innovation is Tandem's cloud-based diabetes management platform and mobile apps designed for patients and healthcare providers alike, fostering user retention through data-driven insights supporting treatment optimization.

These capabilities constitute substantial intangible assets guarded by intellectual property rights granted via recent patent licenses acquired following settlement agreements [S20]. However, the fast-evolving nature of diabetes technology demands continued R&D investment to refresh algorithmic control heuristics and maintain leadership.

Reimbursement Model Shift: From Durable Medical Equipment to Pay-as-You-Go Pharmacy Benefit

In recent years, Tandem initiated a strategic transformation of its U.S.-focused reimbursement approach moving away from traditional upfront pump payments classified under durable medical equipment toward a novel pharmacy benefit channel leveraging a pay-as-you-go model [S6][N1][N2].

Under this evolving structure starting in early 2026, customers no longer incur substantial initial costs for pumps; instead, payment is spread across ongoing insulin cartridge and infusion set purchases reimbursed through pharmacy benefit managers (PBMs). While this lowers patient acquisition barriers enhancing adoption potential, it introduces timing and recognition complexity with deferred revenue realization impacting short-term gross margins.

This shift may exert transient pressure on top-line sales figures for pump hardware but ideally yields enhanced lifetime customer value through recurring consumable revenues along with higher gross profit contribution due to favorable margins on supplies [S6]. The company expects total revenue over the typical four-year device lifecycle per user will exceed legacy reimbursement models despite initial shortfalls.

However, risks materialize around execution clarity such as collection timing from PBMs versus distributors under channel reconfiguration and possible payer pushback delaying payments [N1][N2]. Close monitoring of receivable days sales outstanding (DSO) trends post-implementation will be critical.

Competitive Landscape and Market Challenges in Insulin Delivery Devices

Tandem operates within an intensely competitive sector populated by major incumbents including Medtronic, Insulet, Beta Bionics among others with extensive resources enabling wider product offerings and entrenched distribution networks [S7][S17]. These players frequently leverage aggressive pricing tactics including rebates or bundled offerings creating cost pressure on midsized competitors.

The accelerating usage of GLP-1 receptor agonists broadly for type 2 diabetes treatment further complicates market prospects by potentially shrinking insulin-dependent patient populations or slowing growth trajectories across segments [S7]. Patients often exhibit shifting preferences balancing convenience, wearability perceptions— aspects which Tandem addresses via consumer-inspired designs—against cost considerations.

International expansion also entails navigating heterogeneous regulatory landscapes coupled with government price controls impacting reimbursements unevenly across geographies [S22][S23]. Furthermore, competition increasingly spans hybrid delivery technologies incorporating Bluetooth-enabled insulin pens paired with devices offering non-invasive glucose sensing technologies under development.

Maintaining strong relationships with payors and providers remains paramount given their gatekeeper role influencing patient access within managed care frameworks.

Capital Deployment and Financial Returns: R&D, Capex, and ROE Under the Microscope

Tandem prioritized intensive R&D investment encompassing engineering programs for hardware, software, digital health products under development as well as activities associated with core technologies [S5][S6]. R&D expenses include personnel costs such as salary, incentive compensation including stock-based awards alongside external prototype development costs and clinical trial expenses.

Capex expenditures have remained relatively stable around $19–20 million annually post an earlier downtrend from over $34 million in FY22 suggesting emphasis placed more on incremental capacity enhancement rather than large-scale plant expansions [F1][S28].

Despite operational margin improvements culminating in positive operating income in FY25, weak net income outcomes coupled with significant accumulated deficits translated into negative ROE hovering near zero (-0.4%) illustrating capital inefficiency driven primarily by losses before interest & tax effects [F1].

No dividends were declared while the company abstained from share repurchases during FY25 following a $30 million buyback program completed the prior year implying cautious capital stewardship focused on preserving liquidity amid uncertain earnings durability [F1].

Cash Flow Volatility and Liquidity Position: Current Risks and Financial Flexibility

The company held approximately $90.6 million in cash & equivalents at December 31, 2025 supported by current assets totaling about $618 million against current liabilities near $243 million yielding a healthy current ratio around 2.55x [F1][S4][S16]. This liquidity ratio reflects sufficient near-term cushion to cover operational obligations excluding debt maturities.

Operating cash flow turned negative at nearly -$9.7 million during FY25 contrasting sharply with prior year positive inflows signifying heightened working capital consumption or provisional delays linked partially to the pay-as-you-go revenue transition negatively impacting collections cycles [F1][N2].

Debt structure includes convertible senior notes due 2029 featuring below-market coupon rates (1.50%), which helps manage interest expense rounds but requires vigilant future refinancing strategies given significant principal amounts outstanding (~$316 million) [S16][S18].

Importantly, no share repurchases contributed positively toward liquidity stability though elevated R&D spending alongside marketing investments continues consuming cash flows restraining free cash generation potential visibly negative after accounting for Capex outlays.

Outlook: Key Milestones, Regulatory Approvals, and Market Expansion Prospects

While specific milestone timelines are not detailed explicitly within provided tags or news citations, key expectations include successful execution of the U.S pharmacy benefit reimbursement rollout anticipated over calendar year 2026 which will largely dictate near-term revenue cadence shifts along with margin trajectories [N1][N2].

Regulatory milestones such as FDA clearances on clinical trial endpoints for upgraded Control-IQ+ features or new hardware iterations remain pivotal growth catalysts likely influencing clinician prescribing patterns enhancing market penetration beyond existing installed bases [N5][S1].

Expanding international direct sales presence presents an opportunity for revenue diversification but requires overcoming localized reimbursement negotiations and adapting sales models as evidenced historically within Europe challenges transitioning from distributor-led frameworks [S22][N1].

Investor attention should track quarterly channel mix evolution between distributors versus pharmacy benefit channels alongside signed contracts with major PBMs indicative of scalable adoption.

Risks on the Horizon: Operating Losses, Competitive Pressures, and Regulatory Uncertainties

Recurring operating losses though diminished pose consistent threats requiring scale efficiencies not guaranteed given competitive price wars led by deep-pocketed incumbents who seek to erode Tandem's growing footprint [S1][S7].

Patent litigation has receded following settlement but intellectual property claims along with costly defense liabilities could re-emerge impeding innovation via resource diversion or licensing cost escalations [S8][S20].

Supply chain fragility stemming from component shortages or logistic disruptions—compounded by geopolitical trade barriers—is a material consideration potentially limiting product availability impacting customer satisfaction negatively [S23].

Regulatory environment volatility—including direct-to-consumer advertising scrutiny tightening under evolving FDA/FTC guidelines—raises compliance overheads while imposing constraints on marketing flexibility curbing growth initiatives [S10][S12][S26].

Lastly, healthcare legislation affecting Medicare/Medicaid reimbursements especially amidst policy shifts narrows access which could compress pricing power or delay payments undermining high-margin consumables revenue streams critical under new pharmacy benefit models [S13].

Disclaimer: This analysis is based solely on publicly available documents filed by Tandem Diabetes Care Inc., recent news articles cited herein, and standard industry context as annotated explicitly. It does not constitute investment advice or recommendations nor incorporates any non-public proprietary information about the company.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments