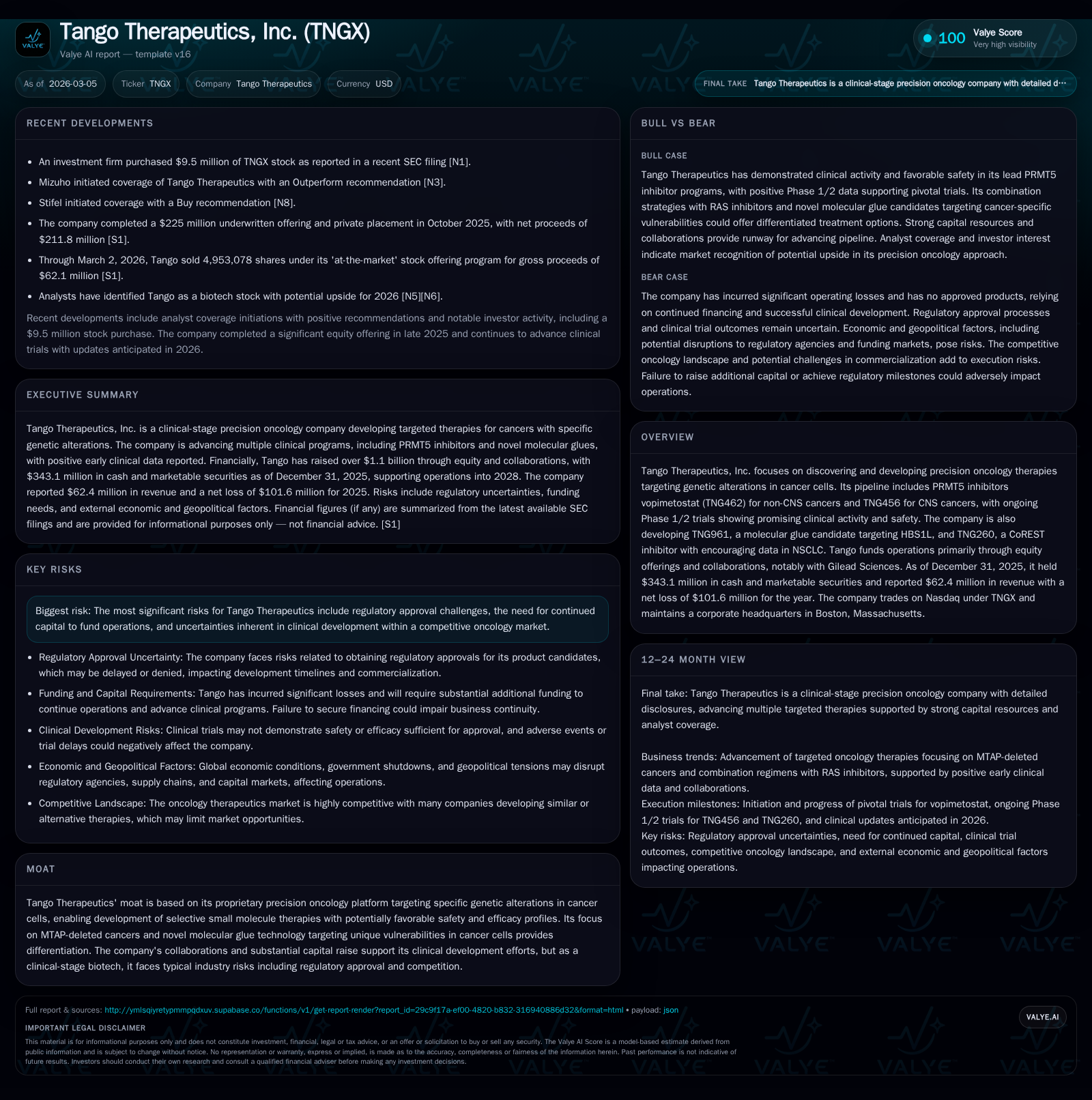

Tango Therapeutics Advances Precision Oncology While Managing Significant Losses and Strong Cash Reserves

A clinical-stage biotech focusing on genetic vulnerabilities in cancer sustains growth via collaboration and equity raises amid high R&D spending.

Tango Therapeutics has demonstrated revenue growth driven by collaborations, particularly with Gilead Sciences, and equity financing fueling its pipeline advancement. Despite significant operating losses, the company maintains a robust cash position that supports operations into 2028. Key assets include multiple precision oncology candidates in early clinical and IND-enabling stages, although regulatory and development risks remain high. Monitoring clinical milestones and capital expenditure will be critical to assessing upcoming inflection points.

Company Background and Business Focus

Founded as a precision oncology company, Tango Therapeutics pursues small molecule therapies exploiting specific genetic alterations in cancer cells to improve efficacy and reduce toxicity [S1]. The company’s pipeline targets tumor vulnerabilities linked to MTAP deletion, FOCAD loss, and other genomic contexts using mechanisms such as PRMT5 inhibition (TNG462 for non-CNS cancers and TNG456 for CNS cancers), molecular glue degraders (TNG961), and epigenetic modulation (TNG260 CoREST inhibitor) [N3],[S16]. Operating out of Boston with roughly 65,000 square feet of leased lab and office space secured through 2033 [S1], Tango employs both internal research capabilities and partnerships.

Historical Performance: Growth Drivers and Financial Overview

Over recent years through fiscal 2025, Tango has steadily increased revenue primarily from milestone recognitions under collaboration agreements—especially with Gilead Sciences [S10]. Revenue grew from $24.9 million in 2022 to $62.4 million in 2025—a compound acceleration aided by upfront payments amortized as contract obligations were fulfilled along with license fees from program out-licensing [F1],[S10]. Despite growing top-line figures, Tango remains pre-commercial with no product sales; reported losses reflect intensive R&D investments required for drug discovery and clinical validation.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 62 | -102 | -139 | -111 | +48.3% | +22.0% |

| 2024 | 42 | -130 | -132 | -146 | +15.2% | -28.1% |

| 2023 | 37 | -102 | -118 | -114 | +46.9% | +5.9% |

| 2022 | 25 | -108 | -109 | -111 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 689000 | -140 | -29.3 |

| 2024 | 689000 | -132 | -65.3 |

| 2023 | 689000 | -120 | -40.2 |

| 2022 | -117 | -43.4 |

Source: SEC companyfacts cache [F1].

Operating losses, while narrowing compared to prior years, remain significant at approximately $111 million in 2025 [F1], primarily driven by research and development expenses exceeding $130 million during the year as the company advances multiple programs through early-phase trials [S19],[S28]. General & administrative costs alongside technology platform investments also weigh on margins.

Pipeline Development and Clinical Progress

Tango focuses on genetically defined patient populations exploiting collateral lethality associated with gene deletions such as MTAP and FOCAD [S16]. Lead candidates include:

- Vopimetostat (TNG462): A PRMT5 inhibitor being tested for non-CNS cancers.

- TNG456: A PRMT5 inhibitor optimized for CNS malignancies.

- TNG961: A molecular glue candidate degrading HBS1L protein essential for certain FOCAD-deleted tumors; currently in IND-enabling stages [S16].

- TNG260: A CoREST epigenetic modulator demonstrating promising median progression-free survival doubling standard-of-care benchmarks among checkpoint inhibitor resistant NSCLC patients at selected doses [S16].

Development challenges include discontinuation of USP1 inhibitor TNG348 due to liver toxicity seen during Phase 1/2 trials [S16],[S24], plus halted enrollment of TNG908 owing to insufficient brain penetration limiting activity against glioblastoma multiforme [S24]. These setbacks reflect the high-risk nature inherent to early oncology pipelines but have led the company to reallocate resources accordingly.

Collaborations and Partnerships

The collaboration agreement with Gilead Sciences provides critical financial support underpinning Tango's research capabilities [S10],[S16]. Initially established in October 2018 with upfront payments totaling $50 million, it was expanded in August 2020 resulting in aggregate upfront funds of $175 million plus additional research extension fees totaling $24 million [S10]. In August 2025, both companies mutually truncated the research term from seven to five years without financial penalties while maintaining licenses for ongoing development programs including milestone and royalty arrangements [S10]. This adjustment reflects adaptive partnering dynamics common within biopharma alliances.

Capital Structure, Liquidity, and Capital Allocation

As of December 31, 2025, Tango held cash, cash equivalents, and marketable securities totaling approximately $343 million—a strong liquidity position enabling funding of operating expenses into at least early-to-mid-2028 under current assumptions [F1],[S15],[S18]. This follows a substantial equity raise completed in October 2025 which generated gross proceeds of $225 million less issuance costs translating into net proceeds of about $211.8 million [S4],[S11],[F1]. Additional proceeds derive from "at-the-market" offerings conducted through early March 2026 accumulating another $62 million [N1],[S18].

The company has not declared or paid dividends historically nor expects to do so given its development stage; capital allocation prioritizes R&D advancement over shareholder returns [S1],[F1]. Share repurchases are minimal historically ($0.7 million) indicating focus remains on funding innovation rather than buybacks [F1]. Tangible property investments are modest ($1M capex in FY25), consistent with emphasis on innovation activities over fixed asset accumulation.[F1]

Regulatory and Market Risks

Tango faces typical clinical-stage biotech risks including regulatory approval uncertainties, clinical trial variability, reimbursement challenges driven by evolving healthcare policies such as drug pricing reforms under the Inflation Reduction Act, and competitive pressures within precision oncology sectors [S5],[S6],[S7],[S21],[S22],[S23]. Recent FDA staffing disruptions may slow approval timelines further complicating commercial outlooks [S7]. Sustained capital access remains necessary until commercial revenues or royalties materialize.[S11]

Internal operational risks such as cybersecurity threats are managed through oversight by experienced IT leadership consistent with best practices for protecting sensitive data within the biotech industry [S9].

Forward Looking Considerations

While explicit forward guidance is limited, key near-term milestones include initiation of a pivotal pancreatic cancer study anticipated in mid-2026 under new consulting leadership alongside dose expansion studies for TNG260 informed by promising NSCLC activity signals [S16]. Future performance will hinge on clinical progress across pipeline candidates, partnership developments especially relating to post-research truncation phases with Gilead Sciences, and prudent capital stewardship amid ongoing negative free cash flow burn.[N3],[N4],[S16]

Summary Outlook Context

Tango Therapeutics operates in a high-potential yet volatile segment focused on genetically-targeted cancer therapies requiring extended investment horizons prior to commercialization. The diversified pipeline leveraging emerging modalities such as molecular glues alongside proteomic targeting distinguishes it among peers. However substantial operating losses persist alongside limited near-term revenue visibility beyond collaborations reflecting typical small-molecule clinical-stage biotech dynamics.

Successful execution of strategic clinical milestones paired with strong recent equity inflows positions Tango favorably relative to peers facing earlier cash constraints or dilution risks. External challenges including regulatory environments around drug pricing add complexity aligned with broader sector trends.

Investors should monitor tranche-based milestones related to key pipeline programs—especially pivotal pancreatic cancer trials—and regulatory interactions alongside updates from collaboration adjustments with Gilead Sciences.

Disclaimer: This report is produced solely for informational purposes based on publicly available documents and does not constitute investment advice or an endorsement of any security or strategy.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments