TechPrecision Corp Confronts Operational Strains with Tactical Finance Moves

Liquidity pressure and divergent subsidiary performance compel strategic financing and operational adjustments.

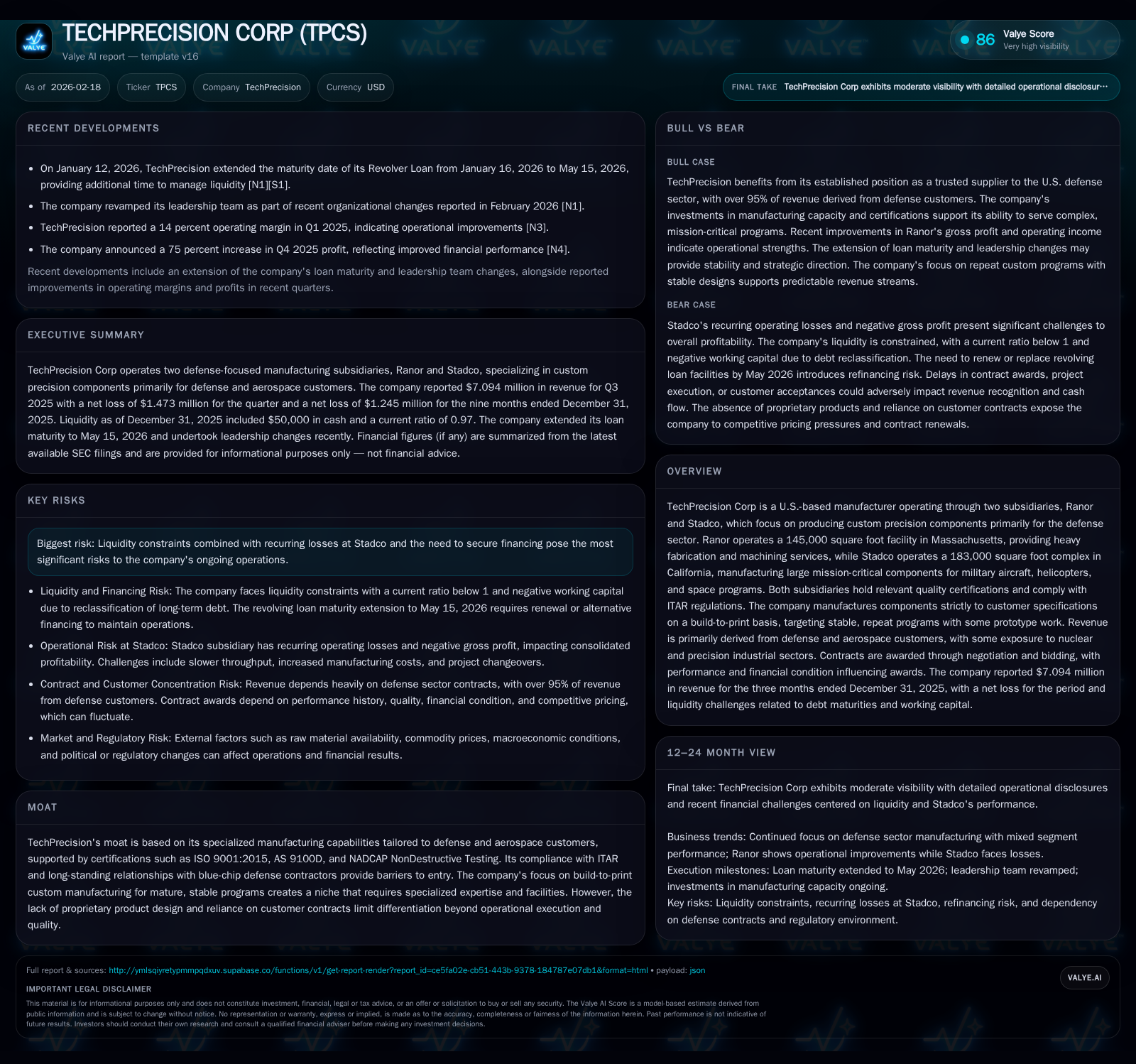

TechPrecision Corp operates two defense-focused manufacturing subsidiaries, Ranor and Stadco, with contrasting financial trajectories. While Ranor maintains stable revenue from established military contracts, Stadco faces recurring operating losses despite increased revenues, constraining overall profitability. The company confronts critical liquidity deadlines, including an upcoming revolver loan renewal by May 2026, amid debt covenant breaches that have reclassified long-term liabilities as current. Significant capital expenditures aimed at facility upgrades weigh on cash flows, resulting in negative free cash flow. Future growth hinges on Stadco’s margin recovery and successful refinancing efforts.

Corporate Profile: U.S. Defense-Centric Precision Manufacturing

TechPrecision Corporation (NASDAQ: TPCS) operates two wholly owned subsidiaries—Ranor in Massachusetts and Stadco in California—specializing in custom precision components primarily for the defense sector. Ranor focuses on heavy fabrication and machining of precision welded components up to 100 tons within its 145,000-square-foot facility. It holds ISO 9001:2015 certification and complies fully with ITAR regulations. Stadco operates approximately 183,000 square feet manufacturing large mission-critical aerospace components for military aircraft, helicopters, and space programs. It holds AS9100D, ISO 9001:2015, and NADCAP NonDestructive Testing accreditations. Both subsidiaries strictly manufacture per customer build-to-print specifications without proprietary product design or IP ownership [N1][S2][S24].

Fiscal Performance Review: Growth Drivers and Subsidiary Divergence

Between FY22 and FY25, TechPrecision's revenue grew from $22.3 million to $34 million — a compound annual growth rate around 9% — driven particularly by Stadco's higher-value military aerospace contracts despite persistent profitability challenges [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 34 | -3 | -1 | -2 | +7.7% | +61.0% |

| 2024 | 32 | -7 | 1 | -5 | +0.5% | -619.3% |

| 2023 | 31 | -1 | 3 | -1 | +41.1% | -179.8% |

| 2022 | 22 | 0 | 0 | -2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -31.4 |

| 2024 | -2 | -90.3 |

| 2023 | 1 | -6.7 |

| 2022 | -1 | -2.3 |

Source: SEC companyfacts cache [F1].

Note: Fiscal years end March 31; data sourced from SEC filings [F1].

Despite growing revenues into FY25, operating income remained negative due to recurring losses from Stadco offsetting Ranor’s more stable margins [S7]. Gross profit expanded owing to favorable project mix shifts between FY24 and FY25; however, SG&A expenses and inefficiencies constrained earnings recovery.

Ranor experienced modest revenue declines linked to shifts in defense customer project mixes but maintained gross margins near or above 17–22%. Conversely, Stadco posted revenue increases (14% year-over-year quarterly growth pre-latest quarter) but sustained recurring operating losses due to chronic gross margin contractions (-6% to -8%) [S7][S18][S21].

Operational Challenges at Stadco: Higher Revenues Coupled with Margin Pressure

Stadco's increased revenue stems from larger contract values tied to military aircraft production lines but has not translated into profitability due to low gross margins driven by high direct costs and suboptimal manufacturing capacity utilization [S7][S18]. Fixed-price contracts typical in aerospace constrain pricing flexibility amidst labor inefficiencies and raw material cost fluctuations such as steel prices.

Unique technologies like electron beam welding cells add capital intensity that pressures margins unless throughput scales adequately [N1][S4][S6]. Improving utilization rates and process efficiencies are critical for margin recovery.

Ranor Subsidiary: Stable Defense Contracts Anchor Segment Performance

Ranor generates over 95% of its revenue from mature defense contracts requiring precision welding combined with CNC machining and nondestructive testing methods such as portable CMMs [S2][S18]. While facing slight revenue contraction (3–5%) due to customer mix changes, it sustains comparatively healthier gross margins (17–22%), reflecting steady build-to-print operations focused on long-term program runs rather than prototypes or one-offs [F1][S7].

This segment provides operational steadiness within the group despite topline pressures [S12][S19].

Liquidity Pressures Amid Debt Covenant Breaches

TechPrecision faces pressing liquidity constraints tied to significant debt obligations totaling approximately $6.7 million classified as current liabilities following repeated covenant breaches [S4][S6][S8][S10]. The company's revolver loan maturity was extended recently to May 15, 2026; however, it requires renewal or alternative financing imminently to sustain operations [N1][S26][S28].

Lenders retain rights to accelerate repayment absent waivers currently not granted, posing substantial going concern risks flagged in recent filings [S6][S10]. The company must either improve operational profitability—particularly at Stadco—or secure fresh financing through restructuring or equity issuance.

Capital Expenditures and Cash Flow Dynamics

Capital investments have increased significantly from under $1 million in FY22 to over $4 million in FY25 as the company upgrades factory machinery and expands capacity tailored for complex aerospace projects [F1][S9]. Partial reimbursements under supplier development agreements mitigate some costs but negative free cash flow persists due to weak operational cash generation (-$599k CFO vs $4.12M capex in FY25).

No dividends or share repurchases are reported indicating management's focus on liquidity preservation amid financial strain [F1]. The combination of cash burn and looming debt maturities underscores the urgency for tactical financial management.

Outlook: Financing Renewal and Efficiency Gains Are Critical

TechPrecision’s near-term outlook depends on:

- Successfully renewing or replacing the revolver credit facility before mid-May 2026,

- Driving margin improvements at Stadco through better capacity utilization and cost controls,

- Maintaining stable contract flows at Ranor while managing concentration risks,

- Careful working capital management amid milestone-based progress payments,

- Prudent capex spending balancing technological needs against liquidity constraints.

Absent tangible efficiency improvements or new financing sources, going concern doubts remain given recent net losses totaling millions annually and an approximate ROE near -31% [F1].

Metrics Summary Table (Fiscal Years Ending March 31)

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue (USD millions) | 22.28 | 31.43 | 31.59 | 34.03 |

| Operating Income (USD M) | -1.56 | -1.11 | -4.63 | -2.16 |

| Net Income (USD M) | -0.35 | -0.98 | -7.04 | -2.75 |

| Operating Cash Flow (USD M) | 0.26 | 3.14 | 1.30 | -0.60 |

| Capital Expenditures (USD M) | 0.94 | 2.33 | 3.23 | 4.12 |

| Stockholders' Equity (USD M) | 15.26 | 14.59 | 7.80 | 8.74 |

Source: SEC XBRL companyfacts cache; all figures approximate [F1]

What Investors Should Monitor Next: Loan Renewal Progress & Margin Trends

Critical near-term indicators include:

- Outcome of revolver loan refinancing efforts by mid-May,

- Quarterly EBITDA trends at Stadco signaling margin recovery,

- Changes in defense contract backlogs affecting volume stability,

- Management updates on cost control initiatives amid inflationary pressures,

- Potential equity raises or amendments extending debt maturities.

Market confidence will depend on execution within a highly regulated U.S.-centric defense manufacturing niche demanding ITAR compliance, NADCAP certifications, and stringent quality standards.

Disclaimer: This analysis reflects public information available through February 18, 2026, including SEC filings and news reports [N1][F1]. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments