Traws Pharma Emerges as Infectious Disease Drug Innovator with Clinical Pipeline Momentum

Recent quarterly filings highlight Traws Pharma's sustained clinical progression and financing efforts amid regulatory challenges.

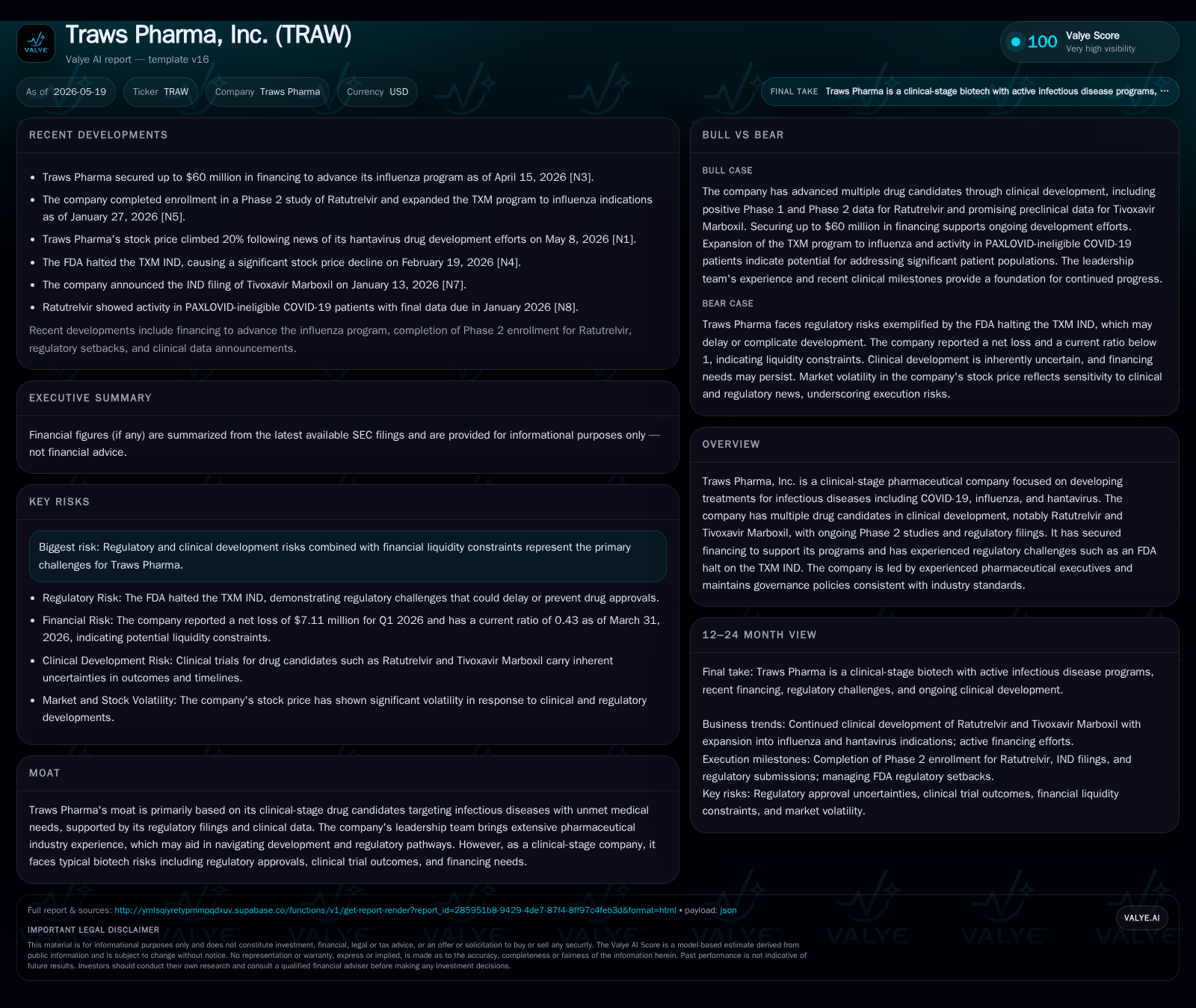

Traws Pharma, Inc., a clinical-stage biopharmaceutical company focused on infectious diseases, advanced its lead drug candidates during the latest quarter despite regulatory setbacks such as the FDA hold on its TXM IND. The company secured capital to support ongoing Phase 2 trials of Ratutrelvir for COVID-19 and Tivoxavir Marboxil for influenza, while ramping up preclinical efforts against hantavirus. Traws operates within a highly competitive infectious disease therapeutics space where regulatory approval and clinical outcomes critically shape value creation. Its current liquidity position signals financial pressure underlying the importance of upcoming clinical milestones and continued funding.

Latest Quarterly Operating Update Highlights

In its May 15, 2026 Form 10-Q filing [S2], Traws Pharma disclosed continued advancement of its clinical pipeline amid regulatory hurdles. Notably, an ongoing FDA clinical hold on the TXM Investigational New Drug (IND) application affects trial timelines but has not derailed overall development strategies. Concurrently, an April Private Investment in Public Equity (PIPE) funded approximately $10 million of new capital with potential extension up to $60 million to support core programs [S27]. The May 15 event filing further incorporated the latest earnings release commentary emphasizing cash management amid fixed liabilities exceeding current assets as of end-March [F1]. Operationally, Phase 2 studies of Ratutrelvir—the company’s ritonavir-free antiviral for COVID-19—and Tivoxavir Marboxil, targeted at seasonal influenza prophylaxis, remain active. These updates anchor Traws’ near-term narrative: progressing through key clinical phases while addressing financial runway constraints.

Clinical-Stage Pipeline and Product Development Strategy

Traws Pharma's core drug candidates focus heavily on infectious disease antivirals designed to address significant unmet medical needs absent fully effective or well-tolerated options [S1]. Ratutrelvir is distinct as a ritonavir-free agent developed for mild-to-moderate COVID-19 patients both eligible and ineligible for existing PAXLOVID® therapy. Positive interim Phase 2 data announced late 2025 validated antiviral activity without ritonavir’s metabolic interactions [S16]. Parallelly, Tivoxavir Marboxil is positioned as a prophylactic treatment candidate for seasonal influenza with regulatory filings including the U.S. IND submitted early 2026 [S18]. Expanding beyond these viruses, Traws recently intensified efforts against hantavirus disease—a rare but fatal viral infection—signaling diversification within their infectious disease portfolio [N1]. The product differentiation resides in oral administration routes combined with novel mechanisms that may improve patient adherence and tolerability versus competitive offerings.

Regulatory strategy involves navigating FDA feedback loops actively; while the TXM IND hold causes procedural delays, it underscores typical rigorous oversight endemic to antiviral development. Endpoint selection prioritizes virologic clearance and symptom resolution metrics aligned with FDA guidance for respiratory virus therapeutics. This strategic focus reflects an understanding of both clinical relevance and regulatory expectations critical for eventual market access.

Business Model and Revenue Dynamics in Clinical BioPharma

Traws Pharma operates under a traditional clinical-stage biopharma model where revenues from product sales are currently negligible due to absence of commercialized drugs [F1]. Funding relies predominantly on equity financing rounds—as evidenced by the recent April PIPE raising $10 million with warrants constructing potential dilution structures [S27]—and anticipated milestone payments or licensing partnerships that may materialize upon successful trial outcomes.

Revenue generation mechanisms await commercialization milestones; thus, financial value accrues through advancement of pipeline candidates across clinical phases and regulatory approvals that trigger option exercises or deal term renegotiations. Cost structures are heavily weighted towards research & development expenditures encompassing clinical trial execution, manufacturing scale-up planning, and preclinical studies.

Customer base at this stage encompasses institutional stakeholders—investors seeking pipeline validation—and later payors such as healthcare providers or government purchasers upon launch. Switching costs remain low until branded therapies reach formulary lists post-regulatory clearance.

Competitive Environment and Industry Positioning

Within the crowded yet innovation-driven infectious disease sector, Traws contends alongside established pharmaceutical groups deploying antiviral solutions targeting SARS-CoV-2 variants, seasonal influenza strains, and rare viral pathologies. It competes primarily on differentiation via chemical composition (ritonavir-free), administration convenience (oral), and expanded patient eligibility profiles.

The company's leadership team comprises seasoned executives bringing meaningful drug development expertise enabling sophisticated navigation through complex FDA approval pathways—an evident competitive edge considering frequent regulatory headwinds facing early-stage biotech peers.

Regulatory scrutiny emerges as a double-edged sword: while raising hurdles such as the present TXM IND hold [S2], efficient management thereof can build credibility enhancing partnership prospects. Market size estimates for COVID-19 therapeutics have compressed since initial pandemic waves but remain significant given variant emergence risks. Seasonal influenza retains steady demand especially if novel prophylactics demonstrate superior efficacy or safety profiles compared to incumbent neuraminidase inhibitors.

Hantavirus therapeutics represent nascent market opportunities dominated by unmet clinical need rather than incumbent competition but face challenges tied to small patient populations impacting development incentives.

Key Growth Drivers Shaping Future Value Trajectory

Several measurable catalysts underpin Traws’ prospective value creation:

- Clinical Trial Milestones: Completion of Phase 2 enrollment and data readouts for Ratutrelvir and Tivoxavir Marboxil will validate efficacy/safety hypotheses central to FDA approval timeline acceleration [S2][N1].

- Regulatory Resolutions: Lifting of the FDA hold on TXM IND use would reduce uncertainty surrounding trial continuance timetable impacting investor confidence.

- Further Financing: Successful execution or upsizing of recently initiated PIPE can extend operational runway stabilizing development continuity given leverage constraints [S27].

- Strategic Partnerships: Potential license agreements or co-development deals following positive proof-of-concept results can generate non-dilutive capital inflows enhancing sustainability.

Key performance indicators include trial enrollment velocity (patient recruitment pace), reported interim efficacy data quality (viral load reduction percentages), cash burn rates relative to runway projections sourced from forthcoming quarterly disclosures.

Risks Centered on Regulatory, Clinical, and Financial Constraints

Risk factors reiterated in the latest quarterly report confirm persistent vulnerabilities inherent in early-stage pharmaceutical developers:

- Regulatory Uncertainty: The FDA clinical hold illustrates inherent delays reducing trial momentum and increasing costs without guaranteed resolution timelines [S2].

- Clinical Outcomes Risk: Efficacy or safety shortfalls at any stage could lead to costly study redesigns or program terminations undermining invested capital value.

- Liquidity Pressure: As of March 31, 2026 balance sheet metrics demonstrate current assets totaling approximately $5.7 million against current liabilities exceeding $13 million resulting in a current ratio around 0.43 signaling tight short-term liquidity [F1]. Additional financing is likely required before commercialization stages; this presents dilution risk impacting shareholder equity stakes.

- Competitive Dynamics: Rapid innovation cycles by larger pharma players with robust R&D budgets could outpace Traws’ moderate scale capabilities restricting market entry timing.

These risks are amplified by typical macroeconomic factors affecting biotech venture funding availability including capital market volatility impacting fundraising success.

Milestones and Market Catalysts to Monitor Next

Investor attention should focus keenly on near-term execution markers that will materially influence Traws’ valuation trajectory:

- Next Quarterly Report (Q2 2026) expected to provide updated cash flow status, progress summaries across trials including responses from regulators post-hold issuance [S2][S3].

- Phase 2 Data Readout Timelines for Ratutrelvir scheduled throughout late 2026 will serve as pivotal demonstration points influencing partnering discussions.

- FDA Interaction Updates concerning resolution pathways for TXM IND holds should be disclosed as they define feasibility of uninterrupted study progression.

- Financing Announcements linked to exercise of warrants issued under recent PIPE transaction or new credit facilities affecting cash runway length.

Monitoring these execution points offers clarity on demand drivers such as enrollment completion rates and provides insight into management’s ability to convert pipeline assets into commercially viable products.

Financial Profile Brief Context

Despite some positive net income previously recorded suggesting exceptional items effect as of year-end 2025 [F1], Traws Pharma’s operating income remains negative reflecting heavy investment in drug development activities offsetting minimal revenue streams typical at this stage. Cash balances last reported are modest reflecting high cash consumption associated with multiple ongoing Phase 2 trials.

This financial state underscores the criticality of managing burn rates prudently while achieving meaningful clinical milestones which could unlock financing alternatives less dilutive than equity issuances alone.

This analysis relies strictly on publicly filed SEC documents dated through May 15, 2026, supplemented by reported market news sources. All forward-looking statements referenced derive directly from official corporate disclosures without subjective valuation extrapolation or speculative projection beyond cited operational data. This report does not constitute investment advice but aims to provide industry-calibrated clarity about Traws Pharma's strategic positioning within infectious disease drug development in mid-2026.

Financial position in context

Current assets of $6mm and current liabilities of $13mm imply a current ratio near 0.43x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments