TREX CO INC Navigates Margin Pressures Amid Capacity Expansion and Input Cost Inflation

TREX's financials reflect challenges from raw material inflation and significant capital investments, balanced by strong brand positioning in sustainable composite decking.

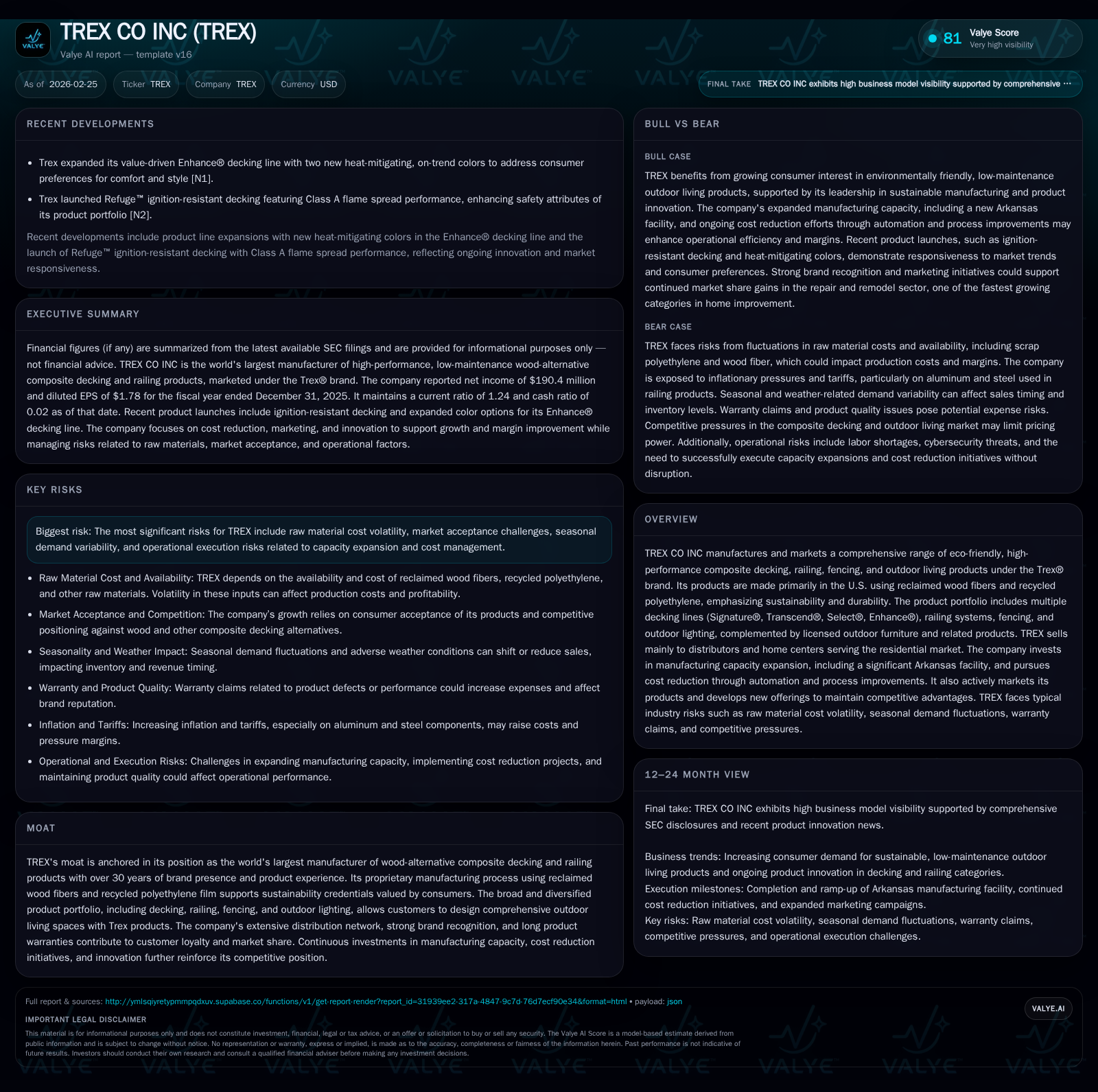

TREX CO INC, the leading manufacturer of composite decking and outdoor living products, reported a decline in operating income and net income for FY2025 driven by higher raw material costs and expenses related to its Arkansas manufacturing facility expansion. Despite these headwinds, the company maintained solid operating cash flow supported by working capital improvements. TREX continues to invest heavily in capacity expansion and manufacturing efficiency with a capital expenditure program focused on automation and modernization. Share repurchases remain part of its capital allocation strategy, while dividend information is not publicly available. Key risks include raw material cost volatility, seasonal demand fluctuations, and operational execution risks tied to capacity ramp-up. Monitoring the company’s ability to restore margins post-expansion and manage input costs will be critical going forward.

Business Overview

TREX CO INC is the world’s largest manufacturer of high-performance composite decking, railing, fencing, and outdoor living products marketed under the Trex® brand. The company employs a proprietary manufacturing process that combines reclaimed wood fibers with recycled polyethylene film emphasizing sustainability. Its broad product lineup includes multiple decking lines such as Signature®, Transcend®, Select®, and Enhance®, along with complementary railing systems, fencing solutions, and outdoor lighting [S1].

With over thirty years of market presence, TREX has established strong competitive advantages through brand strength, extensive warranties, a wide distribution network including over 50 global distributors plus two national retail merchandisers, and continuous product innovation [S1][S7]. The company primarily serves the residential repair, remodeling, and new construction markets.

Historical Performance

TREX experienced growth momentum through the early 2020s driven by strong demand for outdoor living enhancements—a fast-growing segment within home repair and remodel sectors [S1]. However, FY2025 presented operational challenges stemming from rising raw material costs (notably scrap polyethylene and wood fiber), inflationary pressures on labor and freight, alongside costs related to its Arkansas manufacturing facility expansion initiated earlier in the decade.

Despite these headwinds, net sales grew modestly by approximately 3% during nine-month periods ending September 30, 2025 versus prior year due to new product introductions [S25]. Operating income declined sharply due to margin compression linked to higher input costs outpacing revenue gains.

A summary of key financial metrics from FY2022 through FY2025 is shown below:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 190 | 358 | 258 | 224 | -15.9% |

| 2024 | 226 | 144 | 306 | 232 | +10.2% |

| 2023 | 205 | 389 | 276 | 166 | +11.2% |

| 2022 | 185 | 216 | 247 | 176 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 54 | 135 | 18.4 |

| 2024 | 106 | -88 | 26.6 |

| 2023 | 18 | 223 | 28.7 |

| 2022 | 398 | 40 | 35.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available from provided tags; year-over-year percentages are calculated using available operating income and net income figures [F1].

Gross margins compressed in FY2025 as cost increases outpaced revenue growth despite ongoing efforts toward automation and efficiency improvements [S25].

Future Growth Prospects

TREX aims to leverage sustained housing market activity focused on deck replacements and renovations that favor its eco-friendly composite decking products [S1][N11]. Product line expansions such as heat-mitigating colors for the Enhance® decking series target value-conscious consumers seeking differentiated features [N9]. Additionally, innovations like Refuge™ ignition-resistant decking bolster competitive positioning against traditional wood alternatives [N11].

A key strategic focus remains the completion and ramp-up of the Arkansas manufacturing facility designed to increase production capacity significantly while lowering unit costs via automation and modernization [S24][S16]. This expansion is expected to address recent supply constraints during demand surges.

Growth could be tempered by input cost volatility—especially scrap polyethylene pricing—and macroeconomic uncertainties impacting consumer spending on home improvement projects [S1][S28]. Seasonal weather variability also influences quarterly sales timing [S18]. Competitive pressures necessitate ongoing product differentiation.

Financial Outlook & Milestones

While explicit guidance for FY2026 was not provided at reporting date [S3], TREX anticipates flat-to-modest revenue growth coupled with persistent margin pressures during early quarters due to elevated production costs and increased marketing investment.

Key milestones include:

- Achieving steady-state production volumes at Arkansas facility post ramp-up phase expected beyond FY2026.

- Completion of planned capital projects totaling approximately $100-$120 million aimed at manufacturing modernization and innovation pipelines [S9][S16].

- Continued rollout of new products aligned with sustainability trends.

Performance indicators such as gross margin stabilization and operating income recovery will be critical metrics signaling successful capacity absorption.

Capital Structure & Returns

As of December 31, 2025, TREX held cash and equivalents of approximately $3.8 million against current liabilities near $251 million yielding a current ratio around 1.24x [F1]. Total borrowings under revolving credit facilities stood at $133.5 million with availability near $413 million; interest rates averaged roughly mid-4% range reflecting market conditions [S6][S23].

The company has actively repurchased shares as part of capital return initiatives—spending $54 million in FY2025 following $106 million in FY2024—with no dividends disclosed in SEC filings or earnings releases [F1][S15][S16][N8]. Return on equity was an estimated ~18.4% for FY2025 based on net income relative to shareholders’ equity exceeding $1 billion [F1].

Capital expenditures remain substantial reflecting investments focused on growth-oriented capacity expansion rather than maintenance capex alone—a necessary tradeoff constraining free cash flow growth but establishing foundations for longer-term margin improvement [F1][S24].

Risk Assessment Summary

Key risks facing TREX include:

- Raw Material Inflation: Volatility in scrap polyethylene resin or wood fiber prices directly impacts cost structure.

- Operational Execution: Risks associated with ramping new Arkansas plant including potential delays or elevated startup costs.

- Seasonal Demand Variability: Weather-driven shifts can affect quarterly sales patterns unpredictably.

- Competitive Landscape: Increasing competition from alternative composite producers or novel technologies may pressure market share without continued innovation.

- Customer Concentration: Heavy reliance on three major customers (~73% sales) may pose counterparty risk.

- Macroeconomic Sensitivity: Housing market slowdowns or reduced discretionary spending could dampen demand.

Conclusion

TREX remains a category leader leveraging brand equity, sustainability credentials, diverse product mix, and growing manufacturing scale through major capital investments such as its Arkansas facility expansion. While FY2025 financials reflected margin compression due primarily to inflationary inputs and build-out costs resulting in declines in operating income and net income—the robust operating cash flow highlights business resilience.

Ongoing monitoring of operational execution progress on capacity ramps alongside managing raw material cost volatility will be pivotal for assessing when productivity gains translate into improving profitability metrics going forward. Capital allocation prioritizes strategic capex combined with measured share repurchases supporting shareholder returns albeit without current dividend payments.

Overall TREX exemplifies a balanced approach managing near-term profit headwinds amid long-term structural investments within an evolving building materials industry increasingly focused on sustainable innovation.

This analysis is based exclusively on publicly available SEC filings ([F1], [S1]-[S29]) and recent news sources as of February 25, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments