Trinity Capital Inc.: Earnings Growth Bolstered by Strategic Venture Partnerships and Capital Structure

Focused venture-backed lending and a layered capital structure underpin Trinity’s earnings growth amid regulatory and credit nuances.

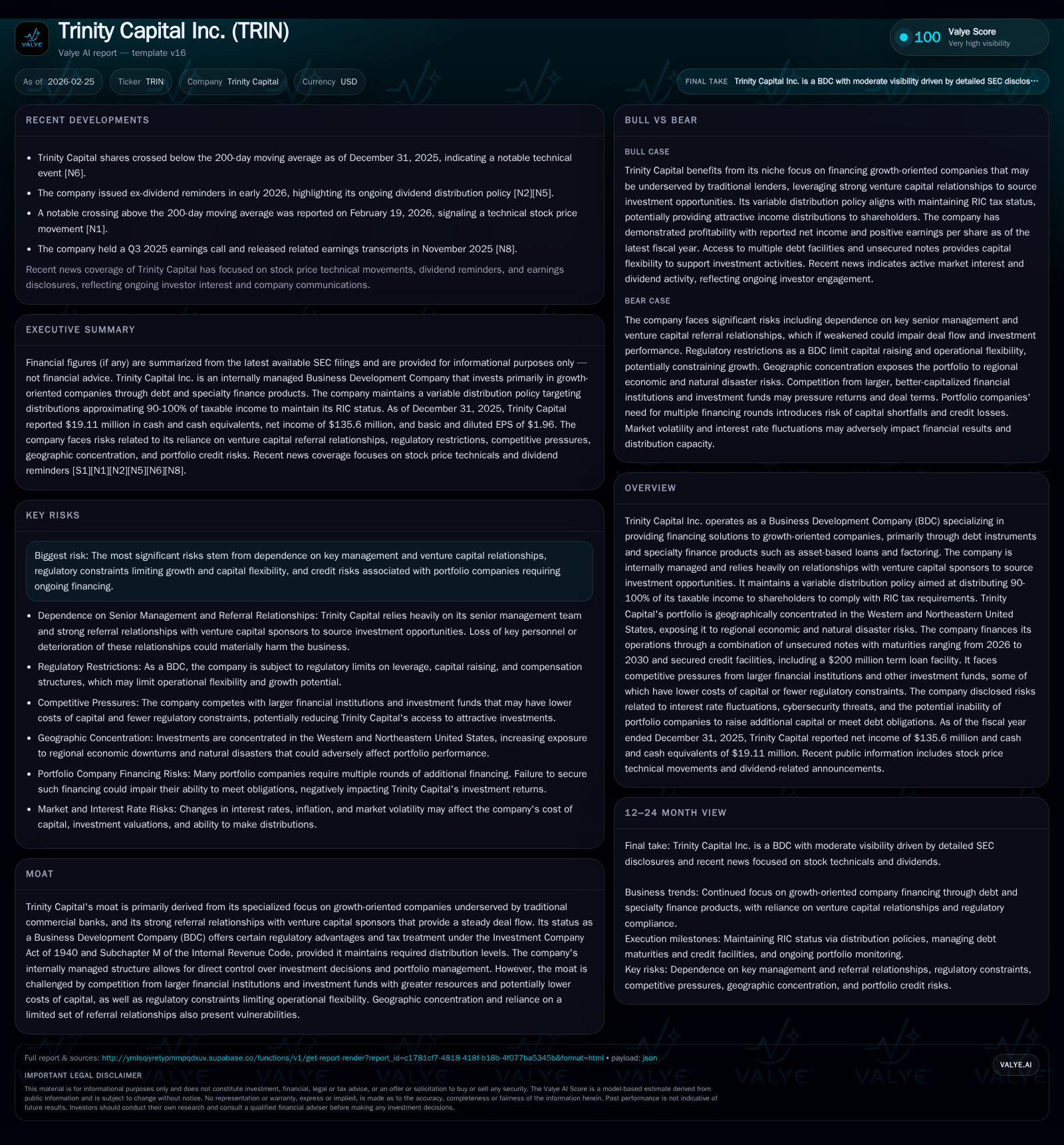

Trinity Capital Inc. has transformed from a loss-maker in FY2022 to showing robust net income of $135.6 million by FY2025, supported by its specialization in venture-backed, growth-oriented financing. The firm’s strong referral network with venture capital sponsors fuels a differentiated deal pipeline, offsetting credit risks inherent to early-stage lending. Its capital framework balances secured and unsecured debt facilities with covenants that impose operational discipline, while the variable dividend policy aligns with RIC regulatory mandates. However, significant negative operating cash flows and geographic concentration present notable challenges. Going forward, monitoring refinancing activity, portfolio yields, and dividend sustainability will be key to assessing ongoing prospects.

Foundations of Growth: Exploring Historical Performance Trends

Trinity Capital Inc.'s financial journey over the past four years reveals a dramatic turnaround. The company swung from a significant net loss of approximately -$30.4 million in fiscal year (FY) 2022 to generating robust profits totaling $135.6 million in FY2025 [F1]. This progression illustrates an effective execution of its growth lending strategy targeting venture-backed companies underserved by traditional banks.

Equally significant is the expansion in stockholders’ equity which rose from about $460 million at the end of FY2022 to over $1.09 billion by FY2025—an increase surpassing 130% over this period [F1]. When juxtaposed against the recent net income figure, this equity growth corresponds to an approximate return on equity (ROE) of 12.4%, suggesting disciplined capital deployment within the constraints faced by Business Development Companies (BDCs).

Despite strong profitability metrics, Trinity’s operating cash flows tell a more nuanced story. Operating cash flow declined substantially each year and was deeply negative at -$535 million for FY2025—a staggering 69% year-over-year deterioration [F1]. This contrast highlights ongoing challenges in cash conversion amidst aggressive portfolio investment activity often seen within specialty finance products such as asset-based loans and factoring.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 136 | -535 | +17.3% |

| 2024 | 116 | -317 | +50.3% |

| 2023 | 77 | -96 | +353.1% |

| 2022 | -30 | -236 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 12.4 |

| 2024 | 14.0 |

| 2023 | 12.6 |

| 2022 | -6.6 |

Source: SEC companyfacts cache [F1].

Note: Dividends paid, buybacks information not available from current filings.

Venture-Backed Lending: The Unique Driver of Trinity’s Investment Pipeline

Trinity's competitive advantage clearly stems from its deep integration with the venture capital ecosystem [S1]. Leveraging close referral relationships with venture capital sponsors allows continuous access to early- and growth-stage companies seeking non-traditional debt financing — which many commercial lenders avoid due to risk or complexity.

This dynamic translates into a highly specialized underwriting approach focused on "venture-backed obligors" where credit analysis blends quantitative financial metrics with qualitative assessments such as innovation potential and sponsor reputation. Although this relationship-centric sourcing bolsters deal flow quality and volume, it also concentrates counterparty risk exposure within select venture capital networks.

The portfolio is predominantly located across Western and Northeastern U.S.—regions synonymous with tech hubs but also vulnerable to sector-specific downturns or regional economic shocks [S29]. As such, credit diligence must carefully weigh borrower-specific growth trajectories against macroeconomic volatility.

Capital Framework: Navigating Debt Facilities and Leverage Conditions

On the funding side, Trinity utilizes a blended capital structure including unsecured notes with staggered maturities ranging between 2026 and 2030 as well as secured credit facilities.

Among its key instruments is the $200 million secured term loan facility arranged through KeyBank, which commenced interest payments in early 2026 at Term SOFR +2.40%, featuring a maximum advance rate of approximately 58% of collateral value [S4][S7][S14]. This facility is coupled with other revolving facilities targeting liquidity needs.

Crucially for investors familiar with BDC regulatory frameworks, Trinity operates under leverage limitations imposed by asset coverage requirements—typically mandating no less than 150% coverage according to Section 18(a)(1)(B) of the Investment Company Act—and contractually enforced borrowing base controls that may call for supplemental collateral or forced repayments upon deficiency events [S6][S25].

Given these constraints, failure to meet covenants could precipitate accelerated debt maturities or restrictions curtailing investment activity and distributions.

Intercreditor agreements related to unitranche or subordinated structures further limit influence over collateral enforcement actions if senior creditors act independently following default scenarios [S20]. In addition, structural subordination exists between Trinity Inc.'s debt instruments versus obligations of subsidiaries which hold underlying assets.

Dividend Strategy and Shareholder Returns Under Regulatory Mandates

BDCs like Trinity benefit from favorable pass-through tax treatment under Subchapter M provided they distribute at least 90% of taxable income annually. Accordingly, Trinity maintains a variable distribution policy designed to approximate this range [S1][S23].

Dividend payments are partially offset by share issuances under their Distribution Reinvestment Plan (DRIP), which issued roughly $1.4 million worth of common stock in FY2025 alone—helping conserve cash while mitigating dilution impact when shares trade near net asset value levels [S23][N2][N5].

The intermittent issuance under DRIP signals a careful balancing act between maintaining attractive shareholder returns through distributions while preserving sufficient capital for portfolio reinvestment across product cycles.

No formal share buyback programs were executed under the most recent authorization despite board approval for repurchases up to $30 million previously announced—with any future programs contingent on market conditions and regulatory compliance considerations [S23].

Risk Spectrum: Management Reliance and Geographic Concentration Insights

Trinity’s unique business model inherently involves several risk dimensions detailed extensively in its latest SEC filings [S1][S5][S10]:

- Key Person Risk: Heavy dependence on senior management and investment committee members introduces execution risk if departures occur abruptly.

- Concentration Risk: Geographic concentration primarily in Western/Northeastern U.S exposes portfolio companies to local economic cycles or natural disasters affecting operating outcomes.

- Counterparty Risk: Reliance on venture capital sponsor networks concentrates exposure among select counterparties impacting deal pipelines.

- Credit Risk: Specialty finance products rely on structural protections such as borrowing base audits; yet fraud or misrepresentation can erode collateral value posing downside risks.

- Regulatory Risk: Compliance burdens from evolving BDC regulations may restrict fundraising flexibility or mandate strategic shifts.

- Liquidity Risk: Illiquidity inherent to growth-stage investments restricts quick liquidation options forcing holding during adverse market periods.

- Cybersecurity & Environmental Risks: Exposure through portfolio companies' operations presents operational continuity vulnerabilities or potential liability.

These layered risks necessitate active mitigation protocols through governance oversight, diversified underwriting methodologies despite scale limits, and operational prudence given covenant sensitivities.

Forward View: Identifying Key Indicators for Trinity’s Upcoming Milestones

Explicit forward-looking guidance is notably absent from available disclosures; however analysts should keenly watch several datapoints indicative of near-term performance:

- Changes in utilization levels against KeyBank secured term loan facility could signal portfolio investment cadence shifts or liquidity refinancing strategies [N1][S7].

- Dividend declaration dates and ex-dividend timing provide clues on distributable earnings sustainability amid variability inherent to specialty lending [N2][N5].

- Upcoming maturities spanning unsecured notes into late-decade windows require scrutiny over refinancing terms or rollover risks enduring into higher rate environments [S4][S14].

- Credit quality trends reflected through delinquencies or charge-off metrics posted quarterly will illuminate deteriorations within a relatively high-risk borrower base reliant on equity financing cycles.

Collectively monitoring these indicators alongside macroeconomic data relevant to innovation-driven sectors offers actionable insights into translating structural advantages into consistent shareholder value creation—despite regulatory leverage restrictions.

What Investors Should Monitor: Near-Term Catalysts and Constraints

Looking ahead through an analytical lens uncoupled from explicit company guidance reveals crucial dynamics shaping Trinity’s valuation landscape:

- Regulatory reforms targeting BDC leverage rules or distribution frameworks could alter strategic levers affecting capital deployment flexibility [S21][S22].

- Interest rate volatility influences borrowing costs directly tied to variable rate debt instruments impacting net interest margins given the rising rate environment at present.

- Retaining top-tier investment committee talent remains vital due to their outsized role in navigating complex venture-backed credit landscapes uniquely relevant for deal selection quality stability [S26].

- Macro headwinds affecting tech-heavy regional economies may filter down causing stress on portfolio companies’ cash flows impacting payment schedules.

- Access to cost-efficient debt markets continues being challenged by broader liquidity fluctuations requiring vigilant refinancings amidst maturing liabilities nearing performance inflection points [N4].

These elements combined set the stage for both opportunities rooted in differentiated deal origination models alongside headwinds emanating from external systemic factors inherent to BDCs specializing in nascent industry segments.

Disclaimer: This report is for informational purposes only based on publicly available data as of February 25, 2026. It does not constitute investment advice or a recommendation regarding any securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments