TRANSUITE.ORG Builds Digital Financial Ecosystem While Facing Acute Liquidity Constraints

Recent governance amendments and strategic partnerships underpin TRANSUITE.ORG’s pivot toward Web3 infrastructure amid pressing financial challenges.

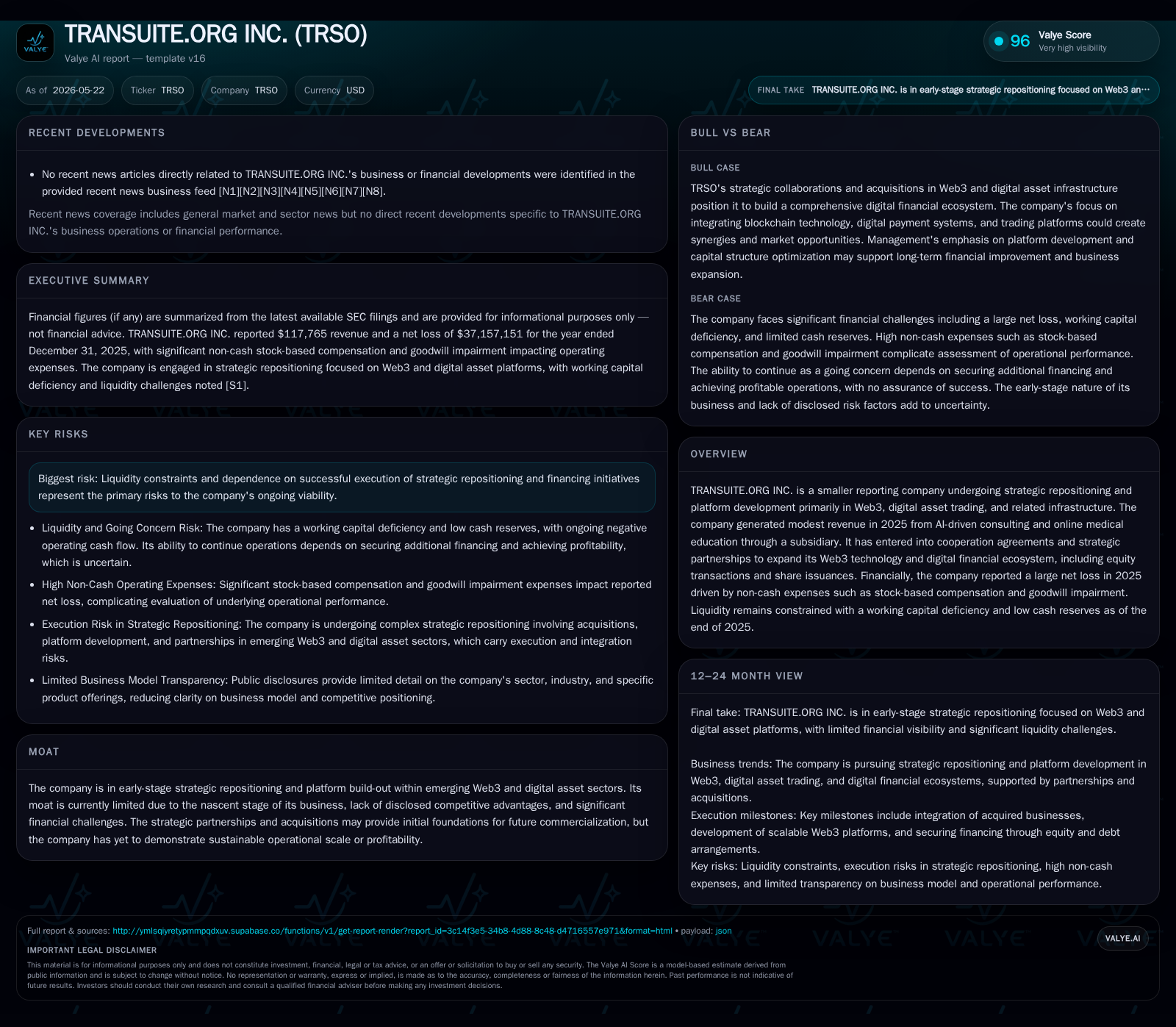

TRANSUITE.ORG Inc. is aggressively repositioning itself into the Web3 and digital assets space through strategic acquisitions, cooperation agreements, and platform development aimed at building an integrated digital financial ecosystem with AI capabilities. The April 2026 filing discloses amended corporate governance provisions allowing expanded capital flexibility, critical in light of the company’s substantial working capital deficiency and minimal cash reserves reported at year-end 2025. Although early revenues arose from AI consulting and online medical education subsidiaries, operating losses driven by non-cash goodwill impairments and stock-based compensation remain severe. The company’s growth hinges on successful integration of newly acquired technology assets and securing fresh financing amidst evolving regulatory frameworks for digital asset platforms.

Recent Strategic Developments and Governance Amendments

In its April 14, 2026 Form 8-K filing [S3], TRANSUITE.ORG Inc. announced that it had filed Amended and Restated Articles of Incorporation expanding its authorized shares to a total of 1.1 billion, comprising 1 billion common stock shares plus 100 million preferred shares. These amendments also introduced provisions for the authorization of preferred stock in various series, new director and officer indemnification clauses, opt-out elections under Nevada statutes, enhanced bylaw authority, and forum selection clauses for internal corporate disputes. This governance restructuring clearly signals an intent to enhance corporate flexibility to pursue diverse financing alternatives—including equity offerings or strategic transactions—and better position the company for growth initiatives requiring shareholder or board approval [S18].

Management simultaneously outlined strategic priorities focused on accelerating revenue growth through integration of recently acquired businesses, advancing platform technology capabilities particularly in Web3 infrastructure and digital asset technologies, developing markets across multiple jurisdictions, and prudently managing capital structure through equity or debt financings as needed [S3][S5]. The filing highlighted that while a large portion of operating expenses in the prior fiscal year were non-cash in nature (stock-based compensation and goodwill impairments), these corporate moves serve as foundational steps toward future commercialization.

Business Model: Evolution Toward Web3 and Digital Asset Services

TRANSUITE.ORG’s business model currently straddles legacy consulting offerings alongside emergent Web3 platform development targeting digital financial ecosystems. For the fiscal year ending December 31, 2025, the company reported modest revenue totaling approximately $117.8K derived largely from its AI-Driven Ecosystem Product Planning consulting services ($115K) complemented by a subsidiary’s online medical education revenue ($2.8K) [S1][F1]. This revenue mix signals initial steps away from bespoke consultancy toward recurring productized services leveraging artificial intelligence.

Concurrently, the company has been embedding Web3 infrastructure components via acquisitions (notably Goldfinch Group Co., Limited—focused on IoT-enabled asset management for e-bike charging terminals with on-chain real-world asset initiatives—and SolanAI Global Ltd.) [S10][S8]. These moves suggest a strategic pivot to build platform-based offerings that connect decentralized applications, blockchain-enabled asset monetization models, and intelligent payment systems within a regulated framework.

The company derives revenue by charging consulting fees for AI ecosystem planning while aiming to monetize integrated Web3 platforms through service agreements tied potentially to transaction volumes, usage fees on asset management platforms, or licensing intellectual property embedded in these infrastructures over time. However, recurring income streams remain undeveloped given the early-stage commercialization status described by management.

Competitive Environment and Industry Positioning in Emerging Tech Platforms

Although precise peer benchmarking information is unavailable due to limited disclosure, TRSO operates in a highly competitive nascent sector characterized by fragmented incumbents pursuing blockchain infrastructure deployment, decentralized finance (DeFi) applications, digital asset exchanges, and AI-enabled fintech solutions. Industry dynamics include rapid technological innovation cycles demanding seamless platform integration capabilities across heterogeneous ecosystems comprising public chains (such as Solana), trading terminals, payment gateways, and compliance tooling.

Switching costs for enterprise customers in this environment can hinge heavily on network effects derived from user base scale and interoperability standards compliance; however regulatory uncertainties—especially with cross-jurisdictional digital assets—introduce adoption hurdles that could slow customer onboarding until clearer frameworks emerge. Partnerships with established fintech groups like Honwo Technology Holding Limited [S8] help bridge technological gaps while facilitating knowledge transfer within evolving regulatory landscapes.

The cumulative ecosystem approach TRSO pursues aims to differentiate their offering via combined AI capabilities plus blockchain-enabled commerce workflow integration—yet until greater operational scale or scalable proprietary IP emerges, the company’s moat is intrinsically limited.

Operational Progress: Acquisitions, Partnerships, and Market Development

Operationally significant events since late 2025 underpin the company's transition narrative [S10][S16]. In late December 2025 TRSO acquired a controlling interest (51%) in Goldfinch Group Co., Limited which operates an IoT-enabled e-bike charging network with over 1.6 million active users across ~100k terminals. Goldfinch-Chong’s initiative embedding real-world assets (RWA) onto blockchain platforms represents a pioneering use case aligned with TRSO’s intended digital financial ecosystem expansion.

Further partnership agreements include a cooperation deal signed February 21, 2026 with Honwo Technology Holding Limited to integrate core Web3 technologies into SolanAI Global Limited—a controlled subsidiary dedicated to exclusive global development subject to regulatory compliance [S8]. This deal involved transferring minority equity interests in SolanAI to Honwo while issuing restricted common stock as consideration reflecting strategic support/incentive alignment mechanisms.

Another significant initiative includes a March agreement with Australian Fintech Group Pty Ltd (AFT Group) focusing on joint long-term collaboration for a comprehensive "payments + public chain + terminals + trading platform" solution encompassing cross-border settlement innovations relevant for TRSO's AUXSTO digital asset trading platform based in Sydney [S17].

These acquisitions and partnerships necessitate complex integration efforts across legal frameworks (multi-jurisdictional registrations such as AUSTRAC), technical interoperability challenges between diverse blockchain protocols/security architectures, and management bandwidth coordination—all critical for timely delivery of envisioned platform synergies.

Growth Drivers and Future Commercialization Potential

Key identified growth drivers consist primarily of: expanding strategic consulting operations leveraging AI-driven ecosystem analytics; scaling digital financial infrastructure capable of serving global markets; broadening enterprise client penetration through cooperative alliances; advancing intellectual property assets enabling novel blockchain-real-world hybrid offerings; and actively pursuing capital structure optimization to fund sustained development [S1][S4][S5]

The company’s acquisition strategy accumulates usable technological building blocks while cooperation agreements extend reach into adjacent fintech ecosystems particularly relevant for trading platforms and payment systems needed within regional markets such as Australia-China corridors.

This phased ramp involves near-term revenue buildup from consulting fees supplemented by anticipated transactional flow monetization tied to deployed digital payment terminals or trading software licenses once regulatory approvals solidify market acceptance.

However growth realization remains contingent on executing multiple integration workstreams efficiently while navigating variable timeline dependencies inherent to evolving technology implementations coupled with external financing availability.

Key Risks: Liquidity, Execution, and Market Adoption Challenges

The most pressing challenge confronting TRANSUITE.ORG is its liquidity position highlighted by a working capital deficit of approximately $489K against current liabilities nearing $810K at fiscal year-end December 31, 2025; cash reserves stood at roughly $3.7K—indicative of short-term coverage stress—and a low current ratio calculated at about 0.4 [F1][S1]

Operating losses escalated sharply to more than $37 million during the same period driven overwhelmingly by large non-cash charges including goodwill impairment ($14.7M) plus substantial stock-based compensation expenses exceeding $22 million issued chiefly via new common shares granted to consultants/related parties [S1]. These accounting considerations mask underlying cash burn but nonetheless reflect continued operational drag absent positive cash flow generation.

Execution risks are multiplied by ongoing efforts to integrate several disparate acquired entities spanning different geographies/markets each with unique compliance demands plus heterogeneous technology stacks requiring rationalization under one coherent ecosystem blueprint [S5][S8][S10]. Regulatory uncertainty remains material especially relating to cross-border digital asset trading platforms necessitating rigorous AUSTRAC registration compliance among others [S17].

Additionally dependence on external financing—equity or debt—to maintain operations adds credit risk exposure until sustainable profitable operation is reached or alternative capital solutions are secured successfully within planned time horizons [S6][S18]

What to Watch Next: Audit Completion, Financing Events, and Commercial Milestones

Investors should monitor several near-term milestones signaling execution momentum: completion status of the company’s annual audit process which remains underway as cited in recent filings potentially affecting SEC reporting compliance timelines [S3]; announcements regarding planned equity raises or debt restructuring activities designed to alleviate current liquidity constraints; updates on operational rollouts particularly deployment progress related to SolanAI consolidation projects integrating Honwo Technology’s core products [S5][S8]; emergence of first meaningful transactional revenues from newly integrated digital financial platforms especially those linked with AUXSTO trading infrastructure proposed under Australian market expansions [S17]; as well as any clarifying commentary around regulatory clearances impacting multi-jurisdictional operations.

These catalysts will offer tangible markers validating the company’s strategic repositioning efficacy or alternatively raise red flags if delays or funding gaps recur.

Financial Overview: Snapshot of Operating Performance and Liquidity

For full-year 2025 as per latest annual filing dated May 22, 2026 [F1][S1], TRANSUITE.ORG reported total revenues incrementally rising from zero previously to about $117.8K sourced predominantly from AI consulting services augmented modestly by online medical education subsidiary contributions amounting to approximately $2.8K.

Despite this modest top line pickup there was an expansive net operating loss tallying roughly $37.2 million principally attributable to significant goodwill impairment charges close to $14.7 million along with extensive stock-based compensation totaling more than $22 million arising mainly from share issuances tied to services rendered rather than cash outlays.

Cash-on-hand was approximately $3.7 thousand at year-end consistent with negative operating cash flows around $69 thousand despite some investing inflows attributable nominally from acquisition-related transactions ($3.36K) [F1]

Management narratives emphasize that non-cash expenses should be weighed carefully against underlying cash burn rates while underscoring reliance on forthcoming funding rounds combined with related-party support integral for sustaining operations over upcoming periods [S1][S6]

This analysis is based solely on information publicly available through SEC filings as of mid-2026 combined with general industry context regarding emerging Web3 ecosystems without incorporating any proprietary data or forward-looking forecasts beyond documented statements. It does not constitute investment advice or research views but serves as an independent assessment highlighting both opportunities inherent in strategic transformation efforts alongside material risks stemming from liquidity pressures and execution uncertainty within a rapidly evolving technology sector.

Financial position in context

As of 2025-12-31, companyfacts shows $3,705 in cash and equivalents, current assets of $320,301, and current liabilities of $809,897, implying a current ratio near 0.4x for 2025-12-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments