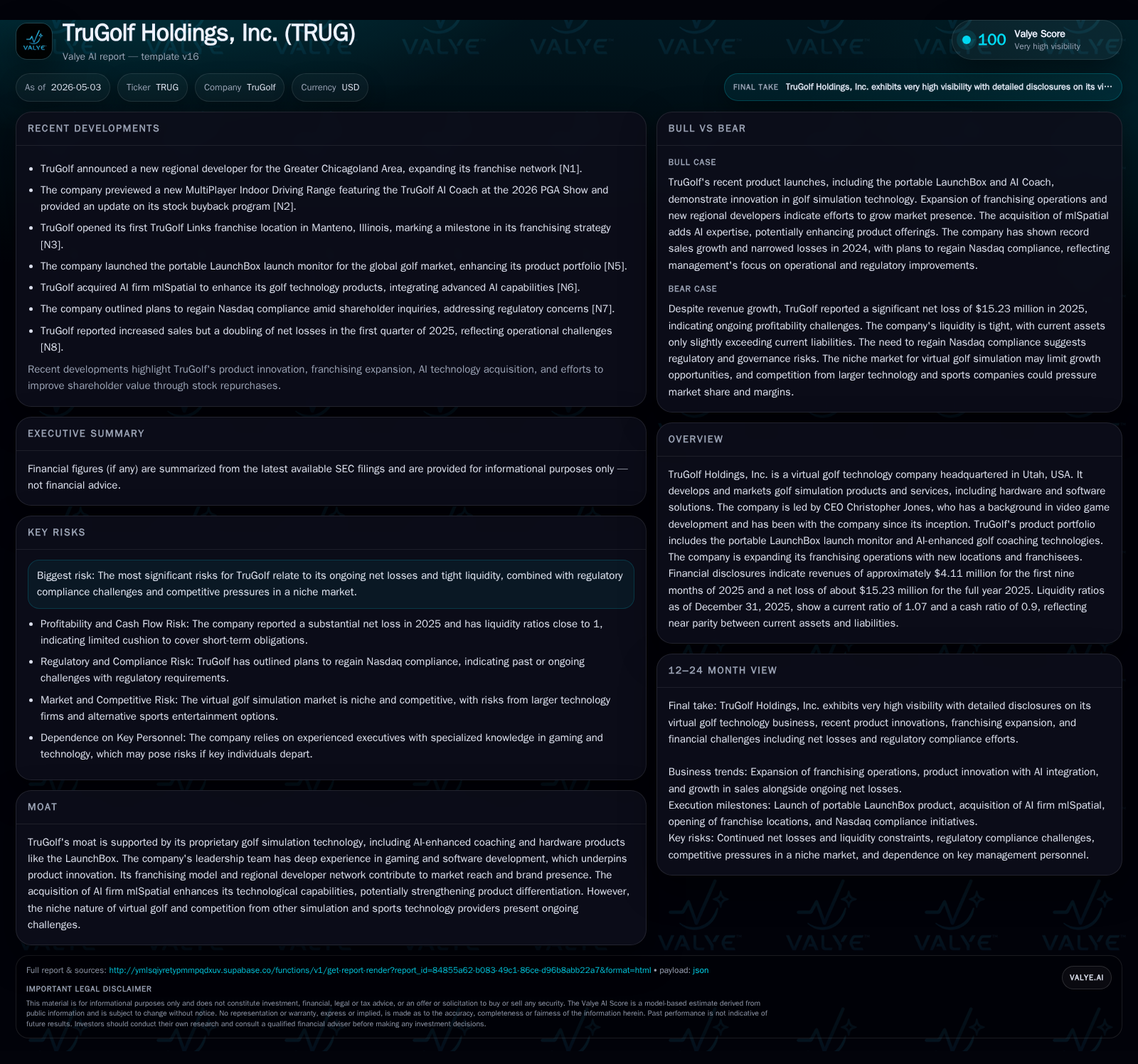

TruGolf Strengthens Governance as Virtual Golf Market Evolves

Recent board changes at TruGolf signal a strategic pivot as the company leverages technology and franchising to capture growth in golf simulation.

On March 16, 2026, TruGolf Holdings appointed Brenner Adams to its board, while Shaun Limbers resigned, marking a shift in governance amid the company's scaling phase. TruGolf's business model integrates proprietary hardware, such as the portable LaunchBox launch monitor, AI-driven coaching software, and a growing franchise network. This positions TruGolf uniquely in the niche virtual golf market, which faces competitive pressures but benefits from differentiated technology and brand expansion strategies. Financials reveal persistent net losses offset by reasonable liquidity and manageable debt, underscoring operational challenges. Key watchpoints include successful franchise rollouts, AI product advances, and board-driven strategic execution.

Board Updates and Strategic Implications

TruGolf Holdings disclosed significant leadership changes on March 16, 2026: Brenner Adams was appointed to the Board of Directors while resigning his role as Chief Growth Officer. Concurrently, longtime director Shaun Limbers stepped down amicably without any operational disagreements reported [S3]. Adams’ new role on the board without committee assignments signals a strategic shift from direct growth management to broader governance oversight—a move that could reflect an evolution in TruGolf’s growth phase or a desire to leverage his expertise at the board level.

Limbers’ departure creates room for refreshed oversight as the company navigates both technological development and franchise expansion. The board changes imply a governance alignment focused on scaling operations sustainably while managing emerging complexities inherent in their hybrid tech-franchise model. Such shifts tend to presage nuanced strategy refinements rather than abrupt course alterations.

Business Model and Product Suite

TruGolf’s revenue model is multilayered. Central to it is the sale of its proprietary hardware products—most notably the portable LaunchBox launch monitor—that enables high-fidelity golf ball tracking for simulations [S1]. These hardware solutions are complemented by AI-powered software aimed at enhancing golf coaching effectiveness through data analytics and personalized feedback mechanisms.

Beyond product sales, TruGolf generates income from franchising virtual golf centers that utilize its systems as experiential venues for consumers. This franchise model offers recurring revenue potential, scalability, and network effects with unit economics improving as more franchises launch successfully [S1]. The company thereby blends B2B-like franchising contracts with end-user engagement through immersive technology.

Moreover, TruGolf has augmented its technological edge through acquisitions like mlSpatial—a firm specializing in AI enhancements—further enriching its software capabilities and deepening product differentiation amid competitors who may lack equivalent integrations.

Competitive Landscape in Virtual Golf Simulation

TruGolf operates in a niche but technologically sophisticated segment marked by rising consumer interest in indoor sports entertainment and simulation fidelity. Competition stems from other simulation providers offering diverse immersive experiences that vary in hardware quality and software realism [S1]. Switching costs are moderate given the unique integration required between hardware installation and coaching platforms.

Barriers include proprietary IP around ball-tracking sensor precision, software sophistication including AI coaching modules, and growing franchise footprint that establishes TruGolf as an ecosystem player rather than a mere equipment vendor. This ecosystem advantage combines customer stickiness through multi-product offerings with established brand identity fostered across franchise locations.

However, competitive pressure endures from companies innovating rapidly in sports technology sectors—especially those targeting golf simulators or indoor recreation alternatives—posing ongoing threats to pricing power unless TruGolf continues advancing its tech stack.

Growth Drivers: Technology and Franchise Expansion

Key growth engines are anchored on several pillars: first is the enhancement of AI capabilities leveraging mlSpatial’s expertise enabling more personalized coaching tools that increase user engagement and perceived value.

Second is the accelerating rollout of new franchise locations which expands TruGolf’s physical presence beyond digital sales alone. Franchise network expansion decreases customer acquisition cost per location due to shared marketing resources and brand equity built via regional developer networks [S1].

Thirdly, geographic diversification into nontraditional golfing climates broadens addressable markets by mitigating weather dependency intrinsic to outdoor golf. Indoor simulations offer stable year-round engagement that is appealing especially for urban populations.

Recurring revenue streams also arise from software licensing or subscription fees related to coaching solutions embedded within franchise venues or sold direct-to-consumers via digital platforms—adding margin mix improvement potential alongside hardware transactions.

Risks and Operational Challenges

Despite promising growth avenues, TruGolf faces notable risks primarily stemming from financial strain: net losses totaled approximately $15.23 million for FY 2025 underpinning investor scrutiny over cash burn sustainability [F1]. While liquidity remains sufficient with a current ratio just above parity at 1.07 supported by $10.5 million cash against $14.4 million liabilities as of December 31, 2025 [F1], further capital injections or improved profitability will be critical to extend runway without dilution.

Operationally, managing quality control across expanding franchises challenges corporate resources—uneven franchisee performance risks brand dilution if not tightly governed [S1]. Additionally, regulatory compliance complexities arise given the tech-franchise hybrid nature requiring adherence to both consumer protection laws and technology device regulations.

Competition-induced pricing pressures could erode margins if substitutes or lower-cost alternatives gain traction before TruGolf solidifies distinctive moat advantages through innovation continuity.

Key Upcoming Milestones and Metrics to Monitor

Key near-term markers include board meetings where strategy concerning growth execution will be refined post-Adams’ appointment [S1]. Monitoring how effectively the board influences expansion priorities offers insights into governance effectiveness.

Franchise launch cadence represents an essential metric; tracking unit economics per new site will highlight scalability success or reveal structural bottlenecks impacting margin improvement.

Product innovation milestones—for instance new iterations of LaunchBox integrating enhanced sensors or superior AI algorithms—will serve as demand drivers reinforcing competitive positioning.

While explicit forward guidance awaits future SEC disclosures, these qualitative indicators function as barometers of operational momentum.

Latest Financial Snapshot and Balance Sheet Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2025-12-31 | ||

| Total debt | $3mm | |

| 2025-12-31 | ||

| Net debt | $-8mm | |

| 2025-12-31 | ||

| Current assets | $15mm | |

| 2025-12-31 | ||

| Current liabilities | $14mm | |

| 2025-12-31 | ||

| Current ratio | 1.07x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period Ended |

|---|---|---|

| Revenue | 21,858,864 | |

| 2024-12-31 | ||

| Operating Income | -6,102,354 | |

| 2025-12-31 | ||

| Net Income | -15,227,893 | |

| 2025-12-31 | ||

| Cash & Equivalents | 10,469,263 | |

| 2025-12-31 | ||

| Total Debt | 2,824,000 | |

| 2025-12-31 | ||

| Current Ratio | 1.07 | |

| 2025-12-31 |

The financials portray a growth-stage company investing aggressively in technology development and franchise rollout resulting in substantial operating deficits [F1]. Cash reserves provide a buffer but necessitate prudent capital deployment given persistent losses near $15 million annually.

Debt levels remain moderate relative to cash on hand yielding net cash positive status of around $7.6 million excluding other liabilities [F1]. Maintaining this balance will be key to sustaining operations without costly capital raises in short term.

This analysis synthesizes publicly available regulatory filings focusing on recent governance developments combined with an overview of TruGolf’s business operations contextualized within the virtual golf simulation sector. The evolving executive team composition aligns with broader strategic ambitions tied to technological innovation and scalable franchising models that may underpin long-term market positioning despite near-term financial headwinds.

Disclaimer: This report is for informational purposes only based on publicly available data as of May 3rd, 2026. It does not constitute investment advice or recommendations regarding TruGolf Holdings' securities or business prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments