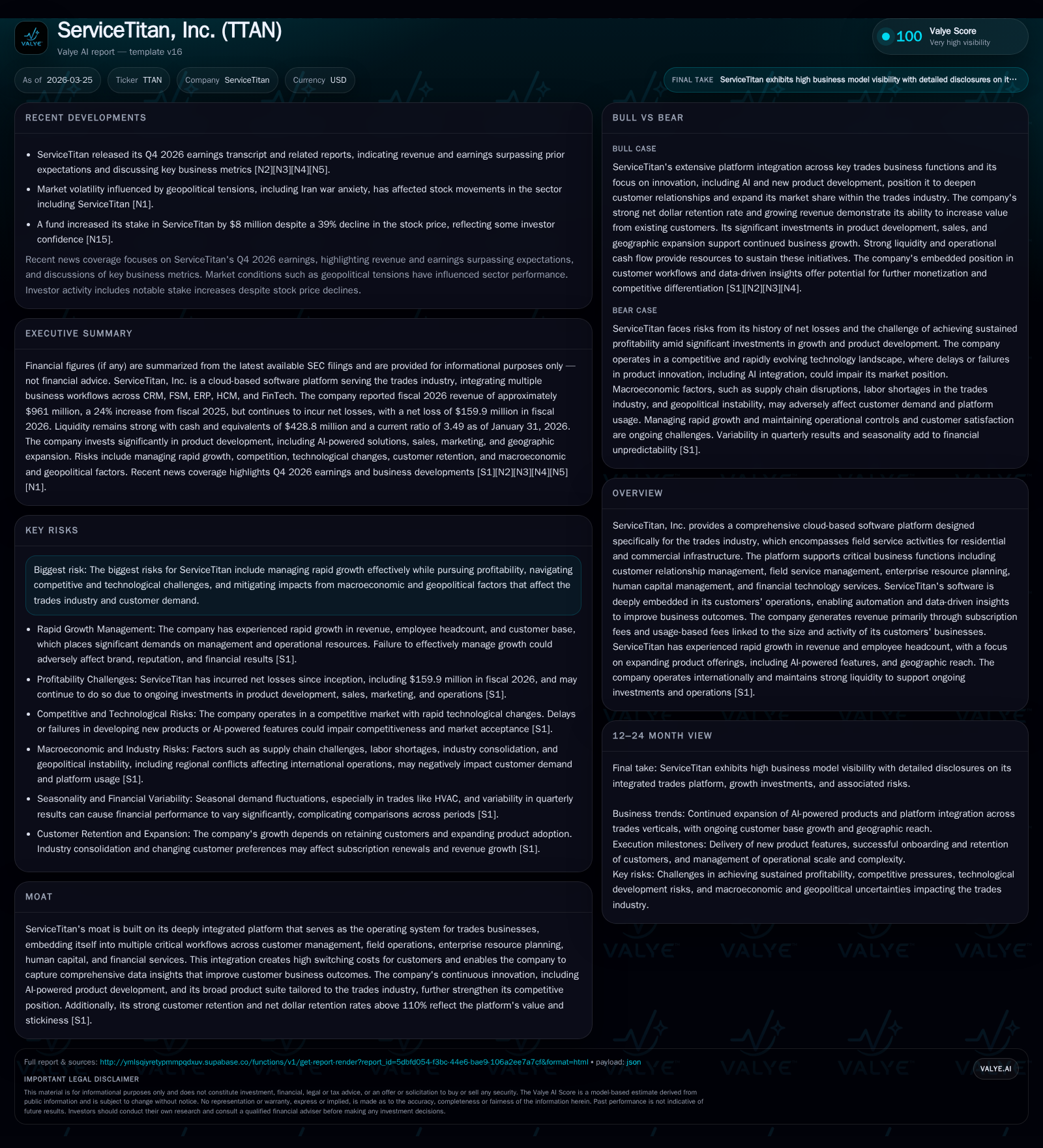

ServiceTitan’s Growth and Profitability: Balancing Expansion with Financial Discipline

ServiceTitan advances rapid revenue gains and AI integration while tackling operating losses to refine its financial model.

ServiceTitan, Inc. posted strong fiscal 2026 revenue growth of 24% year-over-year, reaching $961 million, driven by platform adoption and expanded product offerings including AI-enabled features. Operating losses narrowed by over 26%, reflecting ongoing investments in R&D and sales to scale innovation and market reach. The company maintains a robust liquidity position with $429 million in cash and no outstanding debt, supported by operating cash flow of $110 million and modest capital expenditures. Growth avenues include geographic expansion, new trade verticals, and fintech partnerships amid competitive and macroeconomic pressures. Profitability improvement remains dependent on managing operating leverage alongside growth.

Historical Revenue Growth and Operating Trends

ServiceTitan reported revenue of $961 million for fiscal 2026 compared to $772 million in fiscal 2025, representing a 24% year-over-year increase [F1][S1]. This growth was driven by increased gross transaction volume (GTV) as customers expanded their technician headcount and adopted additional product functionalities. Operating losses improved by approximately 26.4%, narrowing from -$230 million in FY25 to -$169 million in FY26 [F1], signaling progress toward improved operating leverage.

Operating cash flow rose nearly threefold to $110 million in FY26 from $37 million the prior year [F1][S4]. After capital expenditures of $4.7 million [F1], free cash flow was approximately $105 million, providing internal funding for growth initiatives without reliance on external debt.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -160 | 110 | -169 | 5 | +33.1% |

| 2025 | -239 | 37 | -230 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2026 | 105 | -10.5 |

| 2025 | 33 | -16.4 |

Source: SEC companyfacts cache [F1].

Table: ServiceTitan Selected Fiscal Year Performance

Key Drivers Behind ServiceTitan’s Expansion

ServiceTitan's cloud-based SaaS platform serves the trades industry with modules covering CRM, field service management, ERP, human capital management (HCM), and integrated fintech solutions [S1]. The platform’s comprehensive scope embeds deeply into customers’ operations, creating high switching costs reflected in net dollar retention rates exceeding 110% [S28][S1].

Continuous enhancement includes AI-powered tools that improve scheduling efficiency and customer engagement tailored for field technicians—a niche often underserved by general enterprise software [N1][S1]. Fintech partnerships expand monetization through integrated payment processing and consumer financing referral fees within the platform ecosystem [S1][N14].

Effective onboarding and support enable upselling of advanced modules (“Pro offerings”) while facilitating new customer wins. This positions ServiceTitan as an operational backbone offering real-time data-driven decision-making benefits beyond traditional software.

Current Profitability Status and Operating Leverage Challenges

Despite improving operating losses (-$169M vs. -$230M prior year), net income remains negative at about -$160 million for FY26 resulting in an approximate ROE of -10.5% based on equity near $1.53 billion [F1]. Elevated spending on research & development—focused on AI enhancements—and increased sales & marketing expenses constrain profitability [F1][S18][N1].

Sales and marketing expense rose by approximately $38 million (+15%), but declined as a percentage of revenue from ~33% to ~30%, indicating some operating leverage while investing for growth [S16]. This reflects a strategic emphasis on sustaining innovation velocity alongside aggressive market expansion.

AI-Enabled Innovations Enhancing Product Differentiation

AI is central to ServiceTitan’s differentiation strategy. The company deploys AI-driven CRM capabilities enabling smarter targeting along with predictive scheduling algorithms optimizing technician routing—addressing labor shortages in trades sectors [S1][N1].

Additional AI features include dynamic workforce optimization using demand pattern analysis from extensive platform data. These innovations enhance ROI for users, reinforcing adoption stickiness and supporting upsell opportunities.

Capital Structure, Liquidity and Cash Flow Generation

As of fiscal year-end January 31, 2026, ServiceTitan held approximately $429 million in cash and equivalents with no outstanding borrowings under its Amended Credit Agreement that provides up to $250 million in revolving credit capacity through January 2031 [F1][S4][S5]. This absence of debt preserves financial flexibility.

Strong operating cash flow supports modest capital expenditures (~$4.7 million), yielding free cash flow exceeding $100 million that funds organic investments internally without immediate external financing needs [F1][S4].

Credit agreement covenants impose restrictions limiting additional indebtedness or shareholder returns such as dividends or buybacks at this stage [S7], requiring careful capital allocation decisions.

Risks in Scaling Profitably Amid Competition and Macro Pressures

Management highlights risks including operational scalability challenges that could hinder margin recovery if growth is not carefully managed [S1][S8]. Competition spans specialized SaaS providers targeting trades workflows plus broader enterprise platforms like Salesforce or SAP competing adjacently with larger resources but less niche focus [S28].

Emerging competitors investing heavily in AI may erode ServiceTitan’s innovation edge necessitating sustained R&D investment.

Externally, trades sectors face supply chain disruptions affecting material costs and availability alongside labor shortages limiting technician capacity—factors that may constrain customers’ willingness or ability to pay subscription or usage fees typically based on technicians or transaction volume processed [S13][S14]. Macroeconomic volatility including inflationary pressures can dampen demand.

Growth Opportunities Through Geographic and Product Diversification

To extend market reach beyond core segments, ServiceTitan targets international geographic expansion alongside broadening trade vertical coverage supported by recent acquisitions enhancing product breadth and customer diversity [N14][S2].

Further fintech integration aims to embed additional financial services such as payment processing and consumer financing options within the platform to increase monetization while reducing friction for customers traditionally relying on separate vendors.

These diversification strategies also mitigate concentration risks inherent in serving limited verticals or geographies exclusively.

Outlook: Market Expectations and Milestones to Monitor

While formal EPS guidance is limited post-FY26 results announcements [N1], key near-term indicators include new customer additions, engagement with newly launched AI features, fintech partner revenue growth reflecting increasing transaction volumes processed via integrated payments, plus gross transaction volume trends closely tied to usage-based revenues.

Analyst commentary anticipates continued double-digit revenue growth but notes profit inflection timing depends on balancing R&D spend against operating efficiency gains over coming quarters [N2][N3]. Monitoring competitive developments around AI deployment will be critical given rapid technology evolution affecting differentiation sustainability.

Disclaimer: This report is based solely on publicly available filings and news sources as referenced. It does not constitute investment advice or recommendations regarding securities holdings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments