US Nuclear Corp. Advances Radiation Detection, Facing Resource and Financial Limits

The latest quarterly update reveals ongoing innovation in niche radiation detection technologies alongside liquidity pressures constraining growth execution.

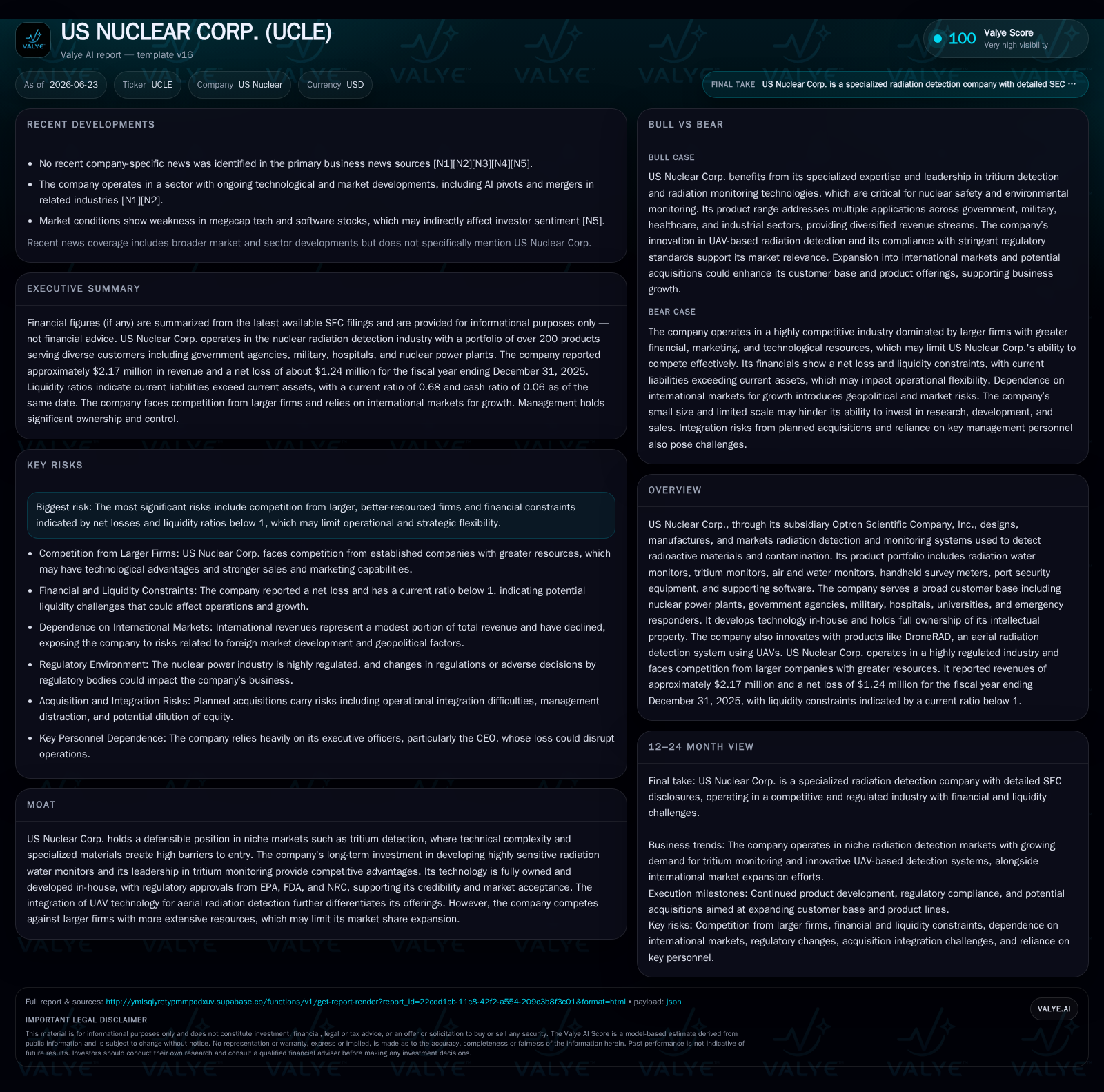

US Nuclear Corp.'s January 2026 quarter discloses steady operations in its specialized radiation detection segments, emphasizing proprietary technology development and competitive positioning in tritium monitoring and UAV-integrated aerial systems. Despite expanding its product portfolio and serving diverse customers—including nuclear power plants and government agencies—it faces headwinds from limited financial resources, low liquidity, and stiff competition from larger industry players. Growth is driven by regulatory tightening and emerging nuclear technologies like Small Modular Reactors (SMRs), but execution risks tied to capital constraints and international market challenges persist.

Latest Operating Update: Quarterly Insights from January 2026 Filing

Business Model: Specialized Radiation Detection and Customer Diversification

US Nuclear's core business derives from design, manufacture, and sale of radiation detection hardware through its subsidiaries Optron Scientific Company Inc., DBA Technical Associates and Overhoff Technology Corporation ([S1], [S7]). The product line exceeds 200 SKUs spanning radiation water monitors capable of detecting alpha, beta, gamma and neutron emissions in complex aquatic environments; specialized tritium detectors addressing technically demanding isotope monitoring; handheld survey meters for field use; and recently innovated UAV-integrated aerial monitoring platforms branded DroneRAD ([S1]). Customers are diverse: nuclear power plants form a foundational sector alongside government agencies (including Homeland Security), military entities, medical institutions like hospitals and universities, plus emergency responders requiring contamination safety solutions ([S1], [S7]).

Revenue generation is primarily transactional via product sales rather than recurring contracts. The company leverages fully proprietary technology developed internally by CEO Robert Goldstein—a notable competitive advantage given the technical complexity inherent especially in waterborne radiation detection. Ownership of intellectual property minimizes licensing friction or infringement risks ([S1]). Regulatory approvals from EPA, FDA, and NRC further facilitate access particularly into highly regulated nuclear facilities ([S1]). However, pricing power may be moderated by competitive pressures from large incumbents.

Industry Landscape: Competitive Scale vs. Differentiated Niche Focus

Operating within the radiation safety equipment industry entails battling sizable peers like Thermo Fisher Scientific—an industrial conglomerate with diversified portfolio—and Mirion Technologies known for specialized instrumentation ([S1], [S18]). Additional competitors include Canberra Industries (nuclear measurement), Smiths Detection (security screening), Ludlum Measurements (handheld devices), which enjoy more extensive sales channels and resources.

US Nuclear's defensible position stems chiefly from its expertise in technically sophisticated niches such as tritium monitoring where barriers include scientific precision demands and material complexity that limit entrants ([S1]). Their radiation water monitors reportedly benefit from proprietary designs difficult to replicate due to water’s attenuating effects on some particle radiations ([S1]). Nonetheless, scale disadvantages manifest in smaller marketing budgets and lower brand awareness relative to multinational firms.

Innovation Spotlight: UAV-Enhanced Aerial Radiation Detection Technology

A distinct feature of US Nuclear's strategy is integrating unmanned aerial vehicle (UAV) technology for remote radiation surveillance—the DroneRAD system—which taps both growing demand for environmental monitoring post-nuclear incidents and logistical efficiencies in hard-to-access areas ([S1]). This positions the company uniquely compared to traditional stationary detectors or handheld devices.

Such innovation enhances product mix quality by adding a differentiated aerial platform not widely offered by legacy peers. The innovation rate supported by internal R&D—though constrained financially—signals management intent to maintain technological relevance amidst evolving detection needs shaped by emergent nuclear energy modalities ([S1]).

Growth Drivers: Regulatory Tailwinds and Emerging Nuclear Technologies

Demand for radiation safety equipment is benefiting structurally from multi-layered industry trends. Regulatory bodies like the NRC enforce stringent standards impacting reactor safety that require continual updates or replacements of detection instrumentation ([S15]). On top of this, small modular reactors (SMRs), forecasted to be safer and more cost-effective than legacy reactors over the next 3–5 years, represent an expanding market segment potentially driving need for fitted monitoring technologies ([S15]).

Geographically, while domestic revenues remain stable, management highlights setbacks in international order capture—a critical area as Asia-Pacific (South Korea, Japan, Australia) alongside Europe are expected growth engines given rapid nuclear deployment plans ([S15], [S18]). Persistent challenges include fielding new foreign orders effectively as well as navigating varied country-specific regulatory landscapes that complicate sales cycles ([S15]).

Environmental monitoring amid growing public concern about radioactive contamination further supports sustained demand beyond just power plants into government emergency preparedness sectors.

Risks and Constraints: Competition, Financial Liquidity, and Market Uncertainties

US Nuclear faces significant risks levied by its smaller size amid dominant incumbent competitors who hold deeper pockets for marketing spend and rapid tech adoption ([S18]). Its limited ability to forecast revenue accurately underscores the unpredictable nature of project-based sales within specialized industrial hardware niches.

Liquidity concerns arise from a current ratio below one (0.68) despite moderate debt levels suggesting operational cash flow deficits or timing mismatches hampering working capital sufficiency ([F1]). The company's net losses (~$940k operating loss on $2.17 million revenue) constrain reinvestment capacity into R&D or go-to-market expansion necessary to capitalize on emerging opportunities such as SMRs or UAV scaling ([F1]).

International revenue contraction—down nearly 16% year-over-year relative contribution—reflects difficulties expanding overseas customer accounts essential for long-term diversification away from slower domestic markets ([S18]). Regulatory dependence on nuclear industry health implies systemic risk if fossil fuel commodity prices depress nuclear capacity expansions globally.

Governance disruption marked by the April 2026 board member resignation appears unrelated operationally but underscores potential volatility within leadership supporting tight resource allocation decisions ([S3]).

What to Watch Next: Upcoming Milestones and Demand Signals

Investors should track US Nuclear’s progress toward securing additional regulatory certifications needed to accelerate commercialization of both existing products like tritium monitors as well as newer DroneRAD UAV systems ([S3], [S1]). Manifestation of increased bookings or backlogs from targeted export markets such as South Korea or Germany would signal turnaround capability on international penetration noted as weak currently.[S15]

Market adoption curves for smaller modular reactors will serve as a bellwether affecting order volume forecasts given their expected growth trajectory over the coming decade ([S15]). Furthermore, announcements about strategic partnerships or acquisitions aimed at alleviating capital constraints would be pivotal execution developments given current liquidity limitations.[S16]

Financial Health Brief: Operating Losses Amid Capital-Efficient Innovation

For the twelve months ending December 31, 2025 US Nuclear reported revenues near $2.17 million juxtaposed against operating losses approximating $939k resulting in net losses slightly deeper at $1.24 million implying tight margins under pressure from fixed overheads or investment costs ([F1], [S1]). Cash reserves stand modestly at roughly $132k (last full disclosure at March 2024), while working capital remains tight with a current ratio of approximately 0.68 highlighting liquidity risks as a restraining factor on scale-up capital expenditures or marketing investment ([F1]).

These metrics conform with expectations for a niche industrial hardware player investing heavily into product innovation yet constrained operationally by limited financial firepower. Capital efficiency is vital; management’s ability to balance R&D spend versus cash burn rates will dictate sustainability amid an uncertain revenue outlook subject to cyclical nuclear infrastructure investment patterns.

This analysis synthesizes the most recent SEC disclosures through Q4 2025 complemented by event filings through mid-2026 to provide an updated industry-contextualized assessment of US Nuclear Corp.’s market positioning amidst operational challenges. No investment advice or forecast is implied herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments