Oracle's Q3 Momentum Tests Cloud Subscription and AI Investment Dynamics

Oracle’s latest quarterly results reveal robust cloud subscription growth alongside sharply increased capital expenditures for AI-driven infrastructure expansion, highlighting a strategic inflection point.

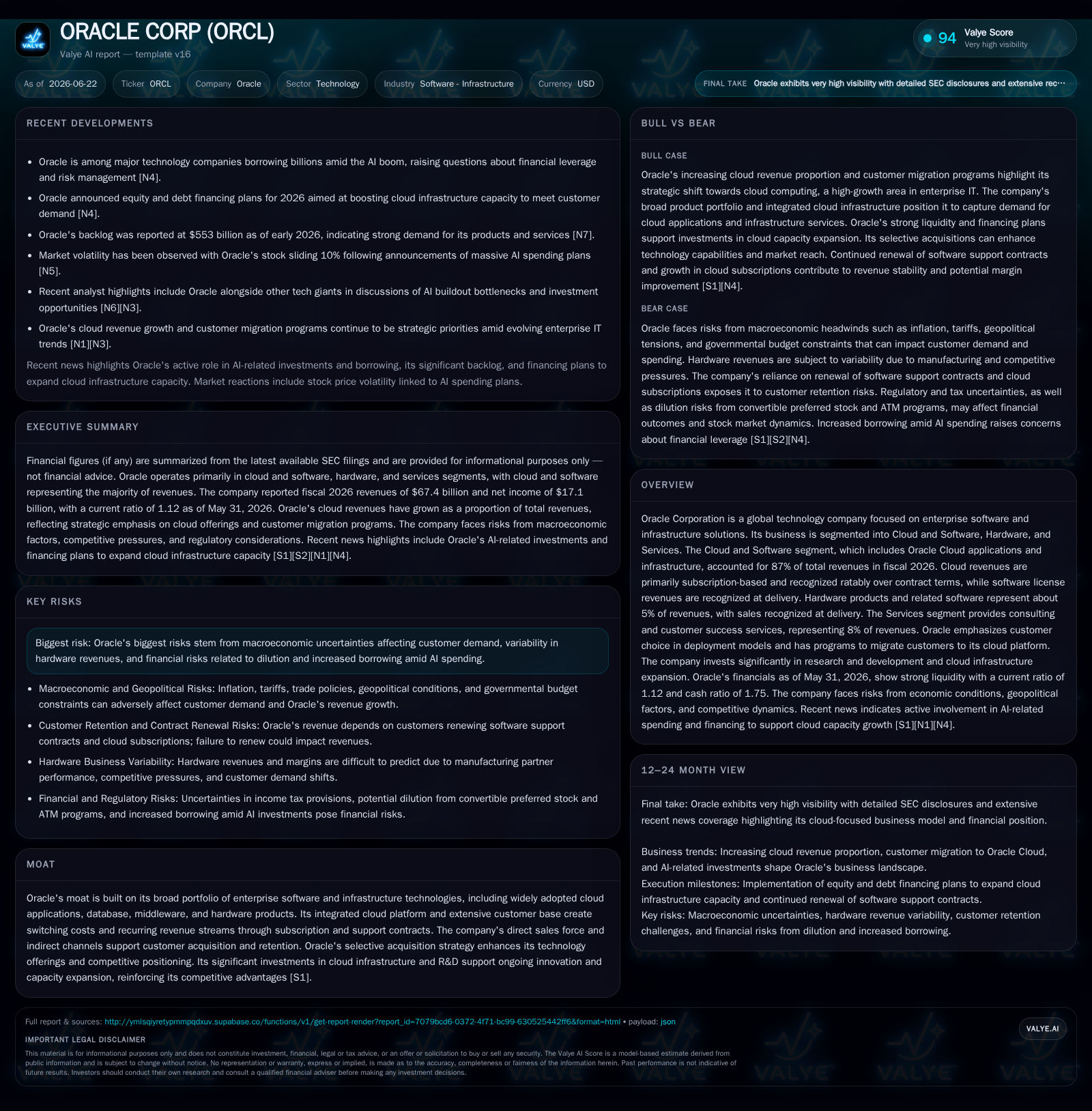

In its Q3 FY2026 10-Q filing, Oracle reported sustained momentum in cloud subscription revenues, which now constitute the majority of its sales base and are recognized ratably over contract terms. This growth is juxtaposed with a significant surge in capital expenditures to expand data center capacity tailored for AI workloads, a trend that continued into fiscal 2026’s year-end annual filing. Oracle’s hybrid business model balances upfront software license fees with recurring subscription and support revenues, engendering considerable recurring revenue streams. However, elevated financial leverage driven by borrowing to fund aggressive AI infrastructure investments poses liquidity and risk considerations going forward.

Latest Quarterly Operating Update: Subscription Strength Meets Elevated Infrastructure Spending

During fiscal 2026, capital expenditures soared from $21.2 billion in the prior year to $55.7 billion largely due to investments expanding data center infrastructure targeting AI workload capacity [S1][S12]. This ramp reflects Oracle’s commitment to scaling Oracle Cloud Infrastructure (OCI) offerings optimized for artificial intelligence applications. The March quarter did not report significant changes in share repurchase activity but reiterated the ongoing capex trajectory aligned with long-term cloud strategy [S3].

Notably, despite hefty capex spending yielding negative free cash flow (-$23.7 billion trailing twelve months) due to these investments, operating income improved to over $20 billion for fiscal 2026 [F1][S1]. These dynamics underscore a deliberate tradeoff favoring growth acceleration through capital intensity.

Oracle’s Hybrid Business Model: Subscription Growth Versus Traditional License Dynamics

Oracle operates a bifurcated revenue model combining cloud subscription incomes with traditional software license fees complemented by software support services [S1]. Cloud contract durations generally range from one to five years, renewing at customer discretion; this ensures revenues are ratably booked throughout the contract span enhancing revenue visibility [S1]. Conversely, software licenses – spanning Oracle Applications, Database systems, Middleware solutions, and Java – generate upfront revenues recognized at delivery.

A sizable portion of recurring revenue stems from software support contracts associated with existing licenses; these renewals command a percentage fee based on license expense and are renewed by the vast majority of customers due to the critical nature of ongoing technical support and continuous update access [S1]. The combined effect of recurring subscription plus support revenues significantly bolsters Annual Recurring Revenue (ARR), dampens churn risk, and stabilizes cash flow [S1].

Further anchoring retention is Oracle’s integrated portfolio including middleware platforms and database management systems that create switching costs via ecosystem lock-in effects as well as channel partner ecosystems that extend reach efficiently [S1]. Customer contracts with multi-year commitments smooth cash flow volatility inherent in point-in-time license bookings.

Competitive Context and Industry Dynamics in Enterprise Software and Cloud Infrastructure

Oracle occupies a distinct position as both an enterprise software provider and a cloud infrastructure operator. Its integrated stack rivals other large vendors such as Microsoft Azure’s hybrid cloud combined with Dynamics 365 SaaS suite or Salesforce’s CRM platform. While providers like Amazon Web Services specialize purely in infrastructure-as-a-service (IaaS), Oracle uniquely pairs robust database management technology with its growing cloud applications universe.

Investment emphasis on AI-optimized data centers mirrors trends seen among competitors but is notable for its scale jump within fiscal 2026 capex allocations [S1][N5]. Unlike pure-play SaaS companies less burdened by hardware costs, Oracle faces margin pressures due to elevated capital intensity but offsets this through cross-selling within a loyal enterprise customer base supported by strong sales teams.

This ecosystem approach offers competitive advantages through enhanced customer retention metrics but also requires persistent R&D investment maintaining technological parity or leadership amid rapid innovation cycles.

Growth Catalysts: AI Investments, Cloud Migration, and Customer Expansion Programs

Growth drivers center on accelerating enterprise digital transformation fueling demand for scalable cloud platforms with flexible deployment options including hybrid models [S1]. Investments in expanding data centers explicitly target supporting emerging AI workloads that require specialized hardware capabilities absent in legacy deployments [S12][N5].

Within its large installed base of enterprise clients globally spanning diverse verticals, Oracle leverages upselling opportunities by embedding AI-driven analytics into its core applications thus increasing per-customer wallet share while advancing net revenue retention rates [S1]. Enhanced middleware integration further supports this expansion.

Strategic acquisitions supplement organic development providing complementary technologies reinforcing competitive moat around key application domains. Meeting client needs for secure multi-cloud environments aligns well with market shifts favoring hybrid cloud adoption.

Key Risks: Financial Leverage, Macroeconomy, Customer Renewal Volatility, Competitive Pressures

Macroeconomic headwinds pose classic risks including constrained IT budgets reducing discretionary spending impacting Oracle’s license-dependent portions disproportionately [S1][S2]. Large software license transactions cause inherent quarterly volatility given upfront recognition timing. This unpredictability contrasts with stabilizing subscription streams but remains material.

Current assets stood at about $46.6 billion versus current liabilities near $41.8 billion, yielding a current ratio of approximately 1.12, indicating adequate near-term liquidity though leverage remains elevated [F1]. Elevated debt issuance underwrites capital expenditures supporting long-term cloud infrastructure buildout but heightens refinancing risk particularly amid tightened credit conditions or rising interest rate environments [S14][N4].

Rapid technological change mandates continuous innovation investment risking obsolescence without maintaining R&D rigor; failure here can erode competitive positioning quickly within the enterprise software sector. In addition regulatory complexities tied to global operations expose Oracle to compliance burdens potentially raising costs or limiting market access.

What to Watch Next: Guidance Signals, Milestones on AI Product Adoption and Capex Efficiency

Upcoming quarterly releases will be pivotal to assess whether ARR growth can sustain itself amidst intensifying competition and macro uncertainties; indicators include renewal rates within cloud subscriptions and any shifts in churn dynamics reported [S2][S3]

Monitoring efficiency gains or margin improvement post completion of major data center expansions will provide evidence whether heavy capex is translating effectively into scalable infrastructure capacity benefiting gross margins eventually.

Further disclosures around adoption rates of new AI-infused enterprise application modules may offer qualitative insight on market traction for Oracle’s strategic technology pivots [N5]. Executive commentary will also be scrutinized for spending discipline signals amid aggressive investment cycles.

Supporting Financial Overview: Leverage Profile and Capital Allocation Priorities

As per the latest balance sheet data through May 31, 2026, cash & equivalents approximate $31.3 billion versus total debt near $130.1 billion resulting in net debt around $98.8 billion; this underpins an elevated leverage position [F1]. The company executed no share repurchases during Q3 but holds about $6.3 billion remaining authorization available which may be reinitiated depending on working capital needs or debt repayment strategies [S12].

Free cash flow turned negative due largely to capex spikes while operating income remained solid at roughly $20.6 billion reflecting operational scale; maintaining profitability alongside investment pacing will be essential going forward [F1][S1][S12]

Overall capital allocation balances sustaining R&D sufficient for innovation leadership while funding extensive OCI infrastructure rollouts critical for long-run growth prospects.

Disclaimer: This analysis is based solely on publicly available SEC filings including the latest quarterly (10-Q) and annual reports (10-K), along with recent event disclosures relevant up to June 2026. It aims to provide an informed industry perspective on Oracle Corporation's business model dynamics without offering investment advice or valuations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments