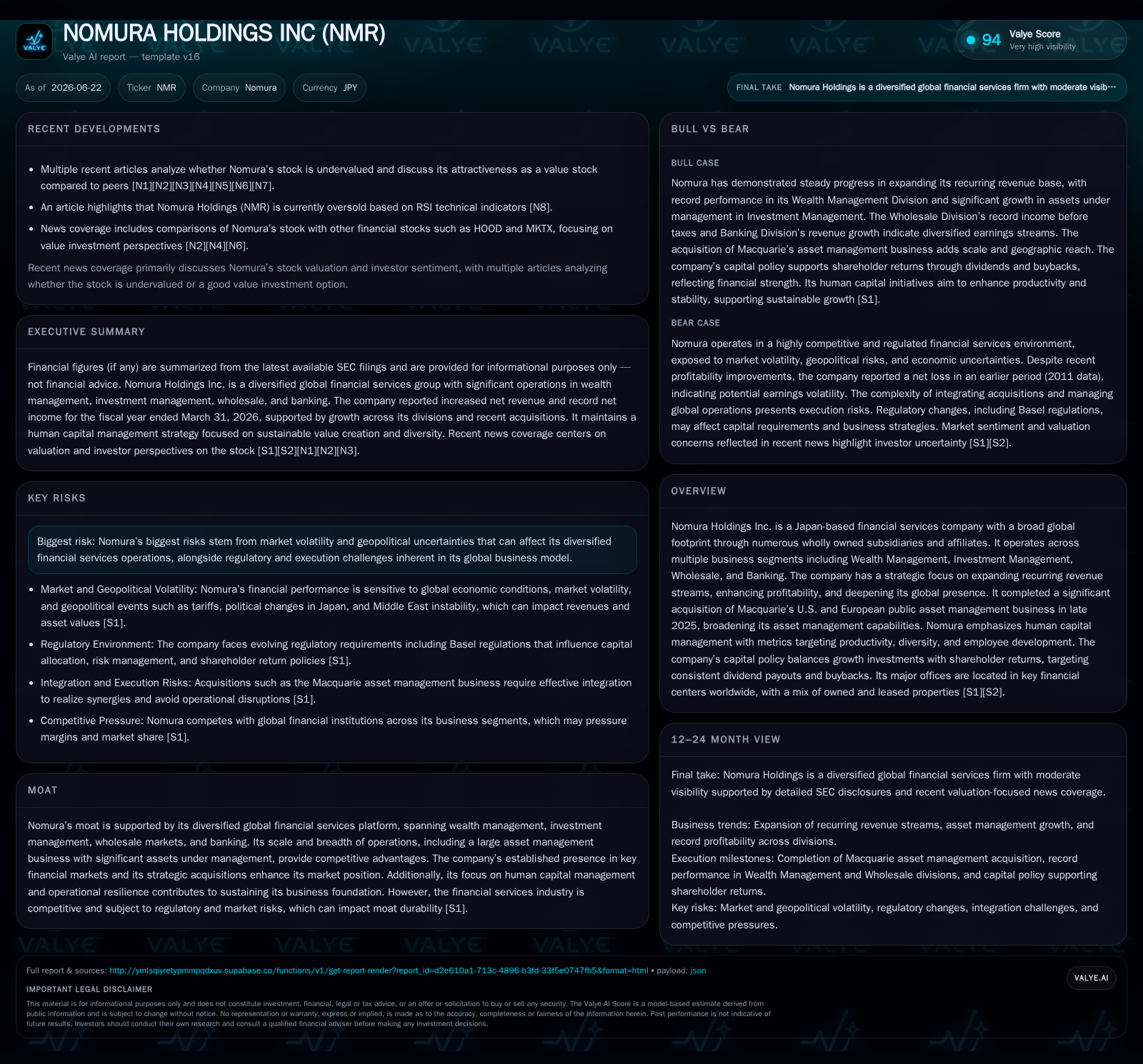

Nomura Holdings Advances Recurring Revenue Model with Record Wealth Management Performance

Nomura’s latest quarter shows strong top-line growth driven by expanded recurring revenues, global asset management inflows, and disciplined cost control.

In its most recent quarterly filing and annual report, Nomura Holdings Inc. marked significant progress toward its strategic shift to recurring revenue streams and profitability enhancement. Wealth Management achieved its best-ever performance with record net inflows and improved cost coverage, supported by a robust Investment Management segment that saw rising assets under management following key overseas acquisitions. The firm continues to leverage its diversified global financial services platform across wealth management, investment banking, wholesale markets, and banking amid a volatile macro environment. Focused capital adequacy, liquidity management, and human capital initiatives underpin operational resilience while geopolitical risks and regulatory demands persist as watchpoints.

Recent Operating Update: Renewed Momentum in Recurring Revenue

Nomura Holdings’ latest filings through June 22, 2026 reveal meaningful momentum consistent with strategic priorities focused on stable earnings and global expansion [S2][S1]. The fiscal year ended March 31, 2026 yielded net revenue of ¥2,167.7 billion, a 14.5% increase from the prior year, driven by solid performance across divisions despite heightened market volatility. Notably, net income attributable to shareholders reached a record ¥362.1 billion with a return on equity of 10.1%, reflecting the company’s progress in balancing growth investments with profitability.

The Wealth Management Division delivered its best results since establishment nearly 25 years ago, achieving an all-time high in recurring revenue underpinned by continued net inflows into recurring revenue assets [S1]. The division’s recurring revenue cost coverage ratio rose to 72%, evidencing effective cost discipline amid revenue gains — a crucial KPI indicating progress toward a more predictable earnings base anchored in fee-based businesses.

Meanwhile, the Investment Management Division expanded assets under management (AUM) to ¥136.9 trillion as of fiscal year-end [S1], benefitting from favorable market factors combined with sustained net inflows and contributions from Macquarie’s recently acquired U.S. and European public asset management business completed late 2025. This acquisition broadens Nomura’s asset management capabilities internationally, augmenting scale and product depth.

The Wholesale Division recorded a near-10% rise in net revenue to ¥1,162.2 billion with income before taxes up over 20%, supported by execution services in equities and strong advisory activity despite regional variability [S19]. The firm maintained prudent risk controls while providing client liquidity during turbulent macroeconomic conditions and geopolitical uncertainty involving U.S. tariff policies, Middle East conflict escalation, and shifting policies in Japan [S1].

Conversely, the Banking Division saw top-line growth offset by increasing expenses resulting in lower income before taxes [S19]. Nonetheless, key operational KPIs such as loan book size at The Nomura Trust & Banking Co., Ltd., investment trust balances, and assets under administration demonstrated steady advancement.

Business Model: Diversified Fee-Based Ecosystem Anchored on Global Scale

Nomura operates an integrated global financial services model spanning four principal segments: Wealth Management; Investment Management; Wholesale (encompassing Global Markets and Investment Banking); and Banking [S3]. Revenue generation is multifaceted:

- Wealth Management: earns recurring fees based on assets under administration (AUA) alongside commissions from brokerage activities targeting individuals and affluent clients.

- Investment Management: collects fee income from asset management based on AUM across various public and alternative investment products.

- Wholesale: generates brokerage commissions, underwriting fees from capital markets activities including equity/debt offerings, advisory fees from M&A transactions, plus trading profits.

- Banking: delivers interest income from lending operations balanced against deposit-taking costs.

The firm’s strategic thrust emphasizes boosting recurring revenues to enhance earnings stability amidst external uncertainties. As reflected in fiscal year results, disciplined cost control coupled with expanding high-margin asset management platforms improves profitability leverage [S1]. Synergies across divisions—especially between Wholesale’s product origination capabilities feeding into Wealth Management’s distribution channels—allow tailored client solutions leveraging Nomura’s global footprint.

Human capital management is integral to operational strength with initiatives driving talent diversity, retention rates below industry norms (6.3%), elevated labor productivity evident from rising revenue per employee metrics (¥75.6 million), and female representation targets progressing steadily [S1]. These efforts bolster innovation capacity critical for differentiated financial solutions amid competitive pressures.

Industry Structure & Competitive Position

Nomura belongs to the global cohort of diversified financial institutions operating at the nexus of investment banking, asset management, wealth advisory services, capital markets operations, and commercial banking. Its primary peers range from Goldman Sachs/Morgan Stanley/UBS in investment banking scale to BlackRock/Macquarie for asset management benchmarks.

Nomura differentiates through an extensive Asia-Pacific franchise headquartered in Japan combined with growing Western asset management platforms post-Macquarie acquisition—enhancing cross-border reach. Its wholesale platform balances traditional fixed-income/equity products with securitized products and equity derivatives catering to institutional clients globally [S19][S22]

Capital adequacy aligns with Basel III regulations; liquidity is robustly managed via diversified unsecured funding complemented by secured borrowings backed by high-quality collateral ensuring resilience against stress scenarios [S21]. Average debt maturities exceed six years reducing refinancing risks amid volatile markets.

Growth Drivers

Several structural factors underpin Nomura's potential growth trajectory:

- AUM Expansion: Rising net inflows both organically within Wealth & Investment Management and through acquisitions broaden fee pools generating stable cash flows; e.g., continued inflows into "Nomu Wrap Fund" surpassed ¥1.5 trillion marking strong investor demand for balanced portfolios [S19].

- Recurring Revenue Growth: Greater penetration of fee-based advisory solutions reduces reliance on episodic trading profits improving earnings quality.

- Globalization & Acquisitions: Strategic acquisitions like Macquarie’s public asset management units deepen capabilities in high-growth regions enhancing client access worldwide.

- Broad Capital Markets Demand: Sustained issuance activities across debt/equity markets fuel underwriting fees.

- Technology & Human Capital: Investments in digital platforms enable innovative product delivery tailored to evolving client preferences.

These drivers manifest in measurable KPIs such as rising ROE (10.1%), improved recurring revenue coverage ratios (72%), increased Assets Under Management (¥136.9 trillion), alongside strengthened global client relationships [S1][S19]

Risks & Watchpoints

Key risk vectors include:

- Market Volatility: Fluctuations affect trading volumes and AUM valuations impacting Wholesale revenues and investment fees.

- Geopolitical Uncertainty: Events such as tariffs implementation threats or Middle East conflicts introduce operational unpredictability amid global exposure.

- Regulatory Pressure: Compliance costs increase under stricter Basel III-like frameworks requiring vigilant capital optimization.

- Credit Risk: Lending activities expose Banking Division to default risks necessitating rigorous underwriting standards.

- Execution Risk: Integration complexities linked to overseas acquisitions could impact synergy realization timelines.

- Currency Fluctuations: Yen volatility influences reported earnings given international operations.

Monitoring these variables remains critical as they can materially affect profit stability despite strategic hedges embedded within the firm’s risk frameworks [S1].

What to Watch Next

Upcoming milestones include the announcement of first-quarter results for FY ending March 31, 2027 on July 29, 2026 which will provide fresh insights on whether momentum from FY2026 has sustained through initial half [S3]. Key focal points will be:

- Continuity of net inflows into Wealth & Investment segments signaling investor confidence.

- Wholesale division revenue trajectory amidst evolving macro dynamics.

- Further cost discipline evidencing margin expansion or stable recurring revenue coverage ratios.

- Capital adequacy ratios retaining compliance without constraining growth initiatives.

- Progress on integration benefits realization from recent acquisitions such as Macquarie bolt-on assets.

- Indicators of risk profiles especially credit quality trends within loan portfolios or trading risk exposures given geopolitical tensions.

This analysis synthesizes Nomura Holdings' recent quarterly disclosures anchored primarily on official SEC filings dated through June 22, 2026 ([S1],[S2],[S3]), incorporating relevant operating metrics demonstrating the company’s advancing transition towards a sustainable recurring-revenue-driven model complemented by prudent capital management amidst an uncertain macro-financial landscape. It avoids speculative projections unsupported by current-period data or forward guidance not explicitly provided within public documents. Readers should consider external sources for updated market developments beyond this report's scope.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments