UFP Technologies' Growth Constrained by Customer Concentration and Supply Chain Dependencies

Custom-engineered medical products propel steady operating gains at UFP Technologies, while concentrated customers and material sourcing challenge future expansion.

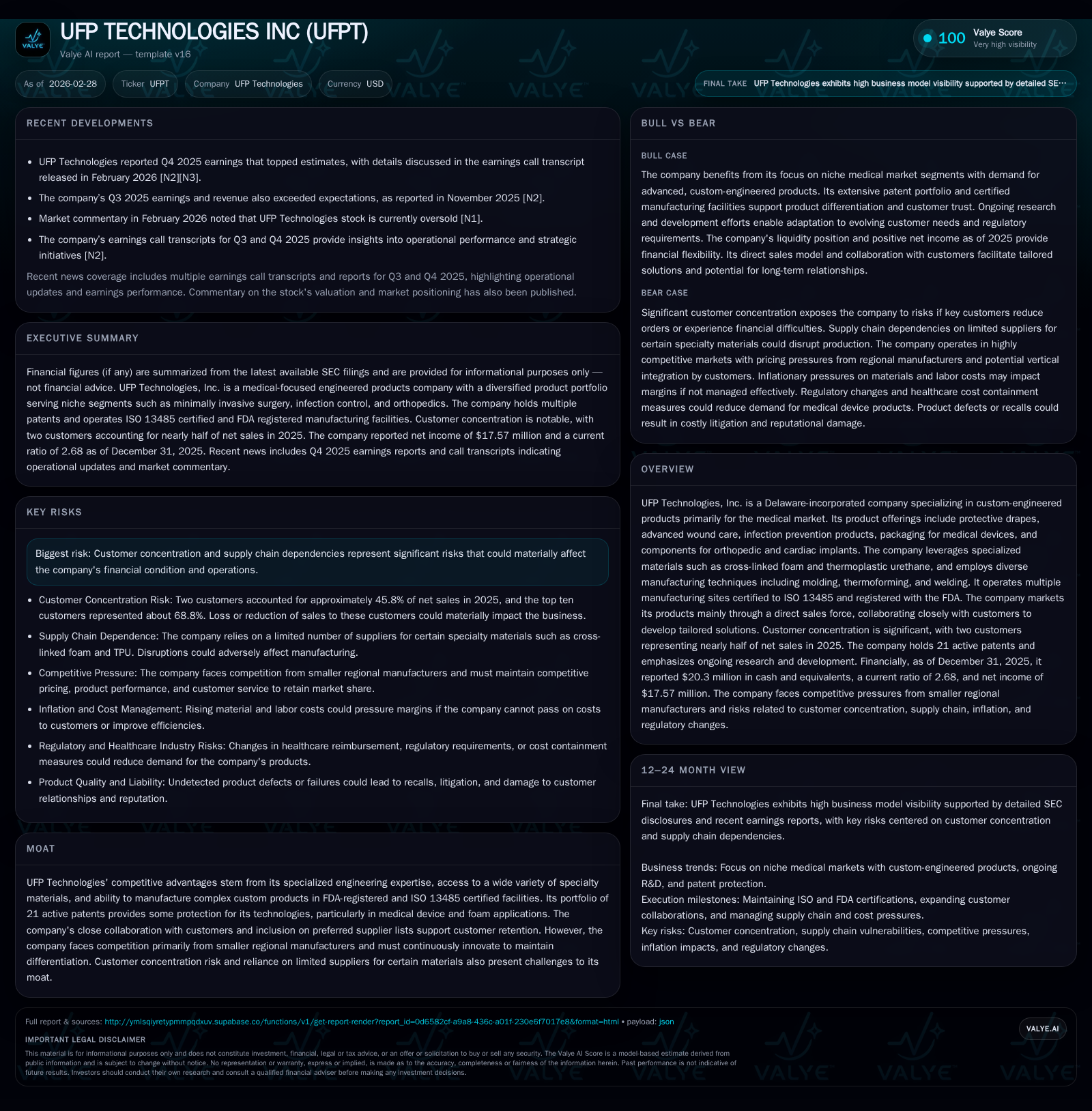

UFP Technologies, Inc. specializes in engineered foam and plastic components primarily serving the medical market, with a focus on custom solutions leveraging specialized materials and manufacturing techniques. The company has delivered solid operating income growth driven by niche product expertise and operational scale, but faces risks from heavy reliance on two key customers who accounted for nearly half of net sales in 2025. Supply chain limitations involving specialty foams add volatility to production continuity. While the firm maintains strong engineering capabilities backed by patents and quality certifications, sustaining growth will require diversification beyond core customer relationships and mitigating supplier risks.

Company Overview

UFP Technologies, Inc., incorporated in Delaware in 1993, operates primarily within the custom-engineered products sector tailored to the medical market. Its portfolio includes protective drapes for robotic surgery, advanced wound care solutions, infection prevention devices, packaging for medical instruments, and specialized components for orthopedic and cardiac implants. Key materials utilized include cross-linked foam and thermoplastic urethane, processed through diverse manufacturing processes such as molding (compression and injection), thermoforming, vacuum-forming, radio frequency welding, impulse welding, laminating, precise die-cutting, and waterjet cutting. The firm's manufacturing footprint encompasses multiple FDA-registered facilities with ISO 13485 certification—reflecting adherence to stringent medical device quality standards [S4][S11].

The company's business model emphasizes collaboration between sales teams and engineers working closely with customers to develop tailored products that optimize clinical outcomes while managing costs effectively. Over time UFP has acquired patents (21 active) protecting various innovations predominantly focused on medical device applications involving foam technologies.

Historical Performance

Revenue growth over recent years has been relatively modest but consistent. The revenue rose from $35.2 million in 2014 to approximately $37.2 million in 2017 reflecting gradual expansion into target niches. However, the latest available full-year data indicates a modest revenue increase of about 2% year-over-year in the most recent fiscal period [F1].

Operating income expanded more robustly from $55.4 million in FY2022 to $92.3 million in FY2025 (+14.1% YoY last year), signaling improved operational leverage or cost control enhancements even as top-line growth remained restrained [F1]. Net income trends tell a more nuanced story—while net income grew from about $41.8 million (FY2022) up to nearly $59 million in FY2024 before declining sharply by over 70% to $17.6 million in FY2025—the reasons for this net income drop are not articulated fully here but may reflect non-operational charges or one-time expenses reported during the last fiscal year [F1].

The company also generated substantial operating cash flow ($91.9 million in FY2025), supporting capital expenditures while yielding free cash flow near $82 million after accounting for capital investments primarily focused on plant upgrades and R&D efforts [F1]. Equity grew steadily reaching $423.9 million at end-2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 18 | 92 | 92 | -70.2% | |

| 2024 | 59 | 67 | 81 | 10 | +31.3% |

| 2023 | 45 | 41 | 58 | 10 | +7.5% |

| 2022 | 42 | 18 | 55 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 4.1 | |

| 2024 | 57 | 17.2 |

| 2023 | 31 | 15.7 |

| 2022 | 4 | 17.6 |

Source: SEC companyfacts cache [F1].

Industry Positioning and Competitive Moat

UFP's competitive moat arises mainly from its significant engineering expertise coupled with access to specialty materials essential for manufacturing complex foam-based medical device components under exacting regulatory standards (FDA registration & ISO certification). Its portfolio of patents reinforces barriers against competitors replicating core technological features particularly concerning cross-linked foam applications designed for infection prevention or implantable device components.

The firm's direct sales approach enables tight integration with customers across product development cycles fostering preferred supplier status among leading medical OEMs such as Intuitive Surgical SARL (robotic surgical systems) and Stryker (orthopedic devices). Nonetheless, heavy reliance on two customers accounting collectively for nearly half of net sales introduces concentrated risk if either alters purchasing strategies or experiences financial distress [S5][S6][S19].

On competition, UFP faces pressure primarily from smaller regional manufacturers specializing in localized markets—a dynamic typical within plastics converting industries where geographic proximity often dictates competitive landscapes due to logistics cost sensitivity [S11]. Core differentiation depends heavily on engineering sophistication plus ability to scale custom prototype-to-production runs economically.

Growth Drivers and Constraints

Drivers:

- Continued demand growth for minimally invasive surgical components and infection control products aligns with broad macro healthcare spending trends.

- Innovation pipeline propelled by ongoing R&D investment targeting novel polymeric materials and assembly technologies expands addressable niches.

- Expansion of manufacturing footprint internationally offers potential capacity additions albeit accompanied by geopolitical risk exposure.

- Cross-selling opportunities stemming from existing relationships within key accounts.

- Growing regulatory emphasis on environmentally responsible packaging incentivizes material innovation potentially favorable to UFP’s specialized portfolio.

Constraints:

- Customer concentration constrains negotiating power; loss or volume reduction from any major client could materially impair revenues.

- Supply chain constraints related to specialty raw materials like cross-linked foam impose production bottlenecks with few alternative sources available [S11][S12].

- Rising input costs (energy prices including electricity/natural gas) coupled with inflationary labor pressures may compress margins without offsetting price adjustments possible given competitive intensity [S25][S26].

- Healthcare industry consolidation may amplify buyer bargaining power increasing price pressure risks [S18].

- Complex regulatory environment including data protection laws adds compliance burden potentially raising operating costs further.

Forward-Looking Considerations

Explicit forward guidance from UFP Technologies is limited according to currently reviewed disclosure documents; instead investors should monitor key indicators including customer order activity from major clients Intuitive Surgical and Stryker given their representativeness of nearly half consolidated revenues [N1][N2][S22]. Strategic acquisition prospects aimed at expanding technology capabilities or geographic reach remain an avenue discussed historically but execution remains uncertain due to integration risks outlined at length by management [S17]. The company plans incremental investments in new production equipment intending to enhance efficiency per recent filings but the impact timing is unclear.

A critical metric will be how effectively UFP manages supplier relationships amidst tight markets for specialty foams—any disruption here could delay deliveries or increase costs notably impacting margins given modest pricing flexibility documented within competitive population segments.

Capital Allocation & Financial Returns

UFP Technologies maintains a strong liquidity position evidenced by cash/equivalents exceeding $20 million while current assets comfortably cover liabilities illustrating a current ratio approximating 2.68—a healthy short-term financial structure [F1][S10]. Capital expenditures have been stable though slightly down (-8% YoY), focusing primarily on upgrading existing plants rather than aggressive expansion signaling disciplined capex management aligned with measured organic growth expectations [F1][S17].

Operating cash flows have ramped impressively—up more than double since FY2022—resulting in robust free cash flow generation supporting balance sheet strength without notable reliance on debt financing which remains controlled per credit agreement references [F1][S7][S8][S10].

Despite solid profitability metrics at the operating level (operating income margin improvement implied), ROE calculated at approximately 4.1% signals room for enhanced efficiency translating equity base into earnings which may align with company’s reinvestment geometry emphasizing technology development versus shareholder distributions presently low or absent based on available data.[F1]

Buyback activities are historically limited absent recent evidence confirming continuation.[F1]

Risks Summary

Key risks crystallize around customer concentration—with just two buyers contributing nearly half of net sales—and supplier dependence on few specialized raw material sources introduces vulnerability especially during global supply chain shocks or regional geopolitical instability (notably facilities near Haiti face unrest threats) [S6][S21][S23][S26]. Regulatory compliance complexity regarding FDA rules plus data privacy laws heightens operational risk exposure.[S12][S24]

Innovative advancements by competitors or rapid technological shifts could erode current patent protections rendering UFP’s offerings less unique causing margin compression.[S13][S16] Inflation dynamics and energy cost volatility elevate input cost uncertainty potentially pressuring pricing power within a competitive contract manufacturing market segment.[S25]

Conclusion

UFP Technologies demonstrates solid core strengths anchored by proprietary engineered solutions serving targeted segments of the medical device industry characterized by demanding regulatory requirements and material specialization needs creating barriers to entry against smaller competitors constrained mainly regionally.

Recent financial results underscore operational maturity delivering improved operating income alongside strong free cash flow generation despite sluggish revenue growth reflective of market niche saturation or mitigated volume expansion potential constrained further by high customer concentration risking abrupt financial impacts upon any client disruption.

Future growth hinges significantly on diversifying its customer base beyond concentrated top accounts while strengthening supply chain resilience amid rising global uncertainties pertaining to geopolitics and raw material availability typical within specialty polymer sectors.

Investors should keep watch on indications of new contract wins outside core clients combined with supply chain developments along with management's moves toward broader geographic or product diversification initiatives that could sustain upward trajectory balancing legacy client dependency risks inherent today.

This analysis is intended solely for informational purposes summarizing SEC filings and related disclosures without expressing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments