Uniti Group’s Fiber Network Expansion and Integration Challenge Drive 2025 Results

Uniti Group leverages a vast fiber network post-merger while balancing growth investments against significant debt and intense competition.

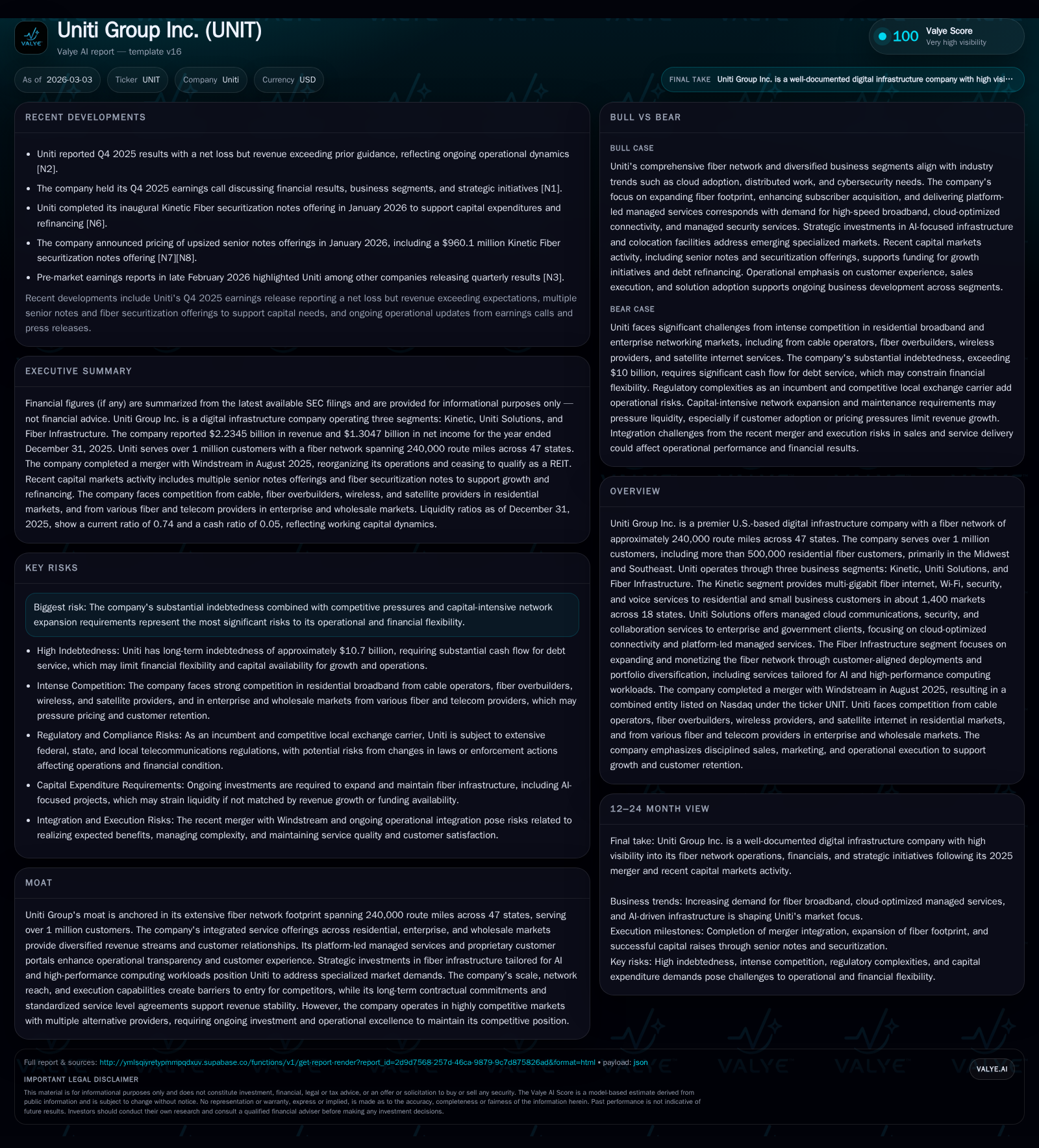

Uniti Group Inc. transformed in 2025 through a pivotal merger integrating Windstream, creating a premier digital infrastructure company with roughly 240,000 fiber route miles serving over 1 million customers. The company generated $2.23 billion in revenue and strong net income of $1.3 billion, driven by contributions from its three segments: Kinetic, Uniti Solutions, and Fiber Infrastructure. While the extensive fiber network underpins diversified revenue streams and competitive barriers, Uniti faces significant risks from heavy indebtedness, competition from alternative broadband providers, and capital-intensive expansion demands. Future growth hinges on network densification, AI-focused infrastructure investments, and monetizing long-term customer contracts.

Company Overview

Uniti Group Inc., newly consolidated post-merger with Windstream as of August 2025, stands as a leading U.S. digital infrastructure company focused on delivering advanced communications services via its extensive fiber network of around 240,000 route miles deployed across 47 states [S24], [S17]. The combined entity services over one million customers including approximately 500,000 residential fiber subscribers situated primarily in the Midwest and Southeast regions [S4]. Uniti operates across three business segments: Kinetic (residential/small business broadband and voice), Uniti Solutions (enterprise managed cloud communications, security, collaboration), and Fiber Infrastructure (fiber leasing and high-capacity transport) [S6], [S7].

Historical Performance and Growth Drivers

In fiscal year 2025, Uniti posted total revenues of $2.234 billion along with an operating income of $262 million and net income reaching approximately $1.305 billion [F1]. The net income figure reflects acquisition accounting effects related to the recent merger [S1]. Below is a summary of key financial metrics for 2025:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

The Kinetic segment contributed just under $930 million in revenue in 2025 by offering multi-gigabit fiber internet packages integrated with Wi-Fi, security and voice services across approximately 1,400 markets spanning 18 states [S6], [S7]. This segment’s growth is driven by rising bandwidth demand fueled by video streaming, remote work applications, telemedicine and gaming proliferation [S6].

Uniti Solutions represented approximately $332 million in revenues focused on enterprise clients’ needs for managed SD-WAN networks, converged security architectures such as SASE/SSE frameworks, UCaaS collaboration tools like OfficeSuite®, and CCaaS contact center platforms—all tailored to facilitate cloud migration and reduce vendor complexity [S4], [S21].

Fiber Infrastructure recorded around $1.054 billion in revenues supporting wholesale transport services to hyperscalers (large cloud providers), content distributors, cable operators, and other telecom carriers through wavelength services up to Nx400 Gbps speeds alongside colocation at fiber-rich points of presence [S14], [S22]. The company’s platform integrates a customer portal featuring map-based Network Intelligence that improves visibility into capacity planning and order fulfillment for these customers [S14].

Network Footprint and Competitive Moat

A critical source of Uniti's moat lies in its expansive fiber footprint totaling nearly a quarter-million route miles servicing roughly 1.9 million equipped premises [S24], enabling connectivity predominantly outside major coastal metros but strategically located near Tier 2/3 cities where emerging AI compute centers are proliferating [S22]. These characteristics allow Uniti to offer dark fiber products that meet hyper-specific requirements of new high-performance computing workloads driven by AI applications.

The firm has prioritized multi-year investment programs to build out long-haul diverse routes with resilient metro laterals aimed at meeting forecast-driven customer expansions while maintaining predictable construction timelines through standardized designs [S14], [S22]. Their commercial arrangements emphasize long-term contractual commitments including indefeasible rights of use (IRUs) to underpin recurring revenue stability.

Competition comes from incumbent local exchange carriers (ILECs), cable companies expanding their own fiber assets along with wireless operators aggressively advancing fixed wireless broadband alternatives—often subsidized by government broadband grants like RDOF or BEAD that threaten accelerated consumer churn or pricing compression within overlapping footprints [S1], [S26], [S9]. Nonetheless, Uniti’s integrated managed service offerings combining connectivity with security layers deliver differentiation vs pure-play infrastructure providers or capex-light MSPs [S12].

Financial Structure & Capital Allocation

As of December 31, 2025, Uniti carried substantial long-term debt totaling about $9.5 billion made up mainly of senior secured/unsecured notes alongside asset-backed securities (ABS), term loans and revolving credit facilities totaling an additional committable capacity near $540 million [F1], [S26]. Early Q1 2026 saw further refinancing transactions including issuing $1 billion issuance of secured notes at an interest rate around 8.625%, intended to optimize maturities but maintaining overall leverage levels given ongoing capital expenditure programs [N7],[N8],[S26].

Liquidity appears somewhat constrained as reflected by a current ratio under one at approximately 0.74 calculated from reported current assets/liabilities as of year-end 2025 [F1]. Cash on hand was relatively modest at $53.5 million.

Capital allocation priorities currently focus on reinvesting free cash flows into fiber densification projects aligned with established customers’ roadmap needs especially in AI growth corridors versus share buybacks or dividend payments which are not projected according to public disclosures or historical trends [S27].

Future Growth Prospects and Risks

Looking forward, Uniti’s growth trajectory hinges heavily on its ability to capitalize on workload migrations toward multi-cloud platforms requiring secure low-latency connections supported by integrated SD-WAN to SASE/SSE transitions within enterprise environments—market segments where it positions itself as a trusted partner through platform-led managed services delivering transparency via its customer portal tools (U Connect for small business/consumers; iconnect for wholesale) combined with specialized engineering resources supporting solution design/migration plans [S21],[S16],[S4].

Additionally, proactive expansion targeting AI-specific infrastructure solutions such as high-count dark fiber routes linking hyperscale data centers outside traditional mega-metropolitan areas may unlock new opportunities as data flow demands explode due to artificial intelligence usage patterns demanding resilience and diverse routing options [S14],[S22].

Conversely, growth ceilings could occur due to various headwinds including intensifying competition fueled by FCC or state broadband subsidies awarded potentially allowing others to overbuild existing facilities driving margin compression or subscriber erosion within legacy consumer markets especially around Kinetic footprint areas facing cord-cutting trends toward purely wireless internet options [S1],[S26],[S9]. Another significant risk vector remains Uniti's high leverage ratio which reduces financial flexibility for opportunistic investments or responding swiftly to market pricing pressures without raising cost of capital considerably [F1],[S26],[N2]. Additional operational risks relate to cybersecurity threats against network infrastructure critical to customers’ operations along with regulatory developments imposing increased compliance burdens particularly related to privacy laws or environmental litigations concerning legacy copper cables containing hazardous materials like lead—all possibly resulting in incremental costs or reputational impacts absent preventive measures [S18],[S19],[S23],[S25].

What To Watch

Going forward into 2026-27 periods analysts should monitor:

- Execution pace of ongoing network expansion projects especially those calibrated for AI compute hubs,

- Growth metrics including broadband penetration rates within the Kinetic footprint,

- Enterprise client adoption rates for advanced managed services incorporating cloud-security solutions,

- Trends in wholesale transport utilization levels tied to hyperscaler demand,

- Impact from incremental government subsidy awards granted competitors,

- Movements in leverage ratios post-refinancing cycle,

- Any shifts in capital allocation policies toward dividends or buybacks.

Conclusion

Uniti Group stands at an inflection point capturing scale benefits from its transformative merger while confronting typical integration challenges amid intense sector competition. Its entrenched position via an extensive U.S.-wide fiber network combined with evolving managed solutions portfolio targeting cloud migration needs underpins solid financial results evidenced by over $2 billion revenue scale complemented by high net profitability metrics. However, substantial indebtedness coupled with ongoing competitive vigor from multiple broadband technologies pose considerable operational constraints. Strategic investments prioritizing AI-tailored infrastructure paired with disciplined capital management will be critical factors shaping Uniti’s growth trajectory through mid-decade.

This analysis is based solely on publicly available information including SEC filings up through March 2nd, 2026 ([F1], [S#]) and recent earnings calls ([N#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments