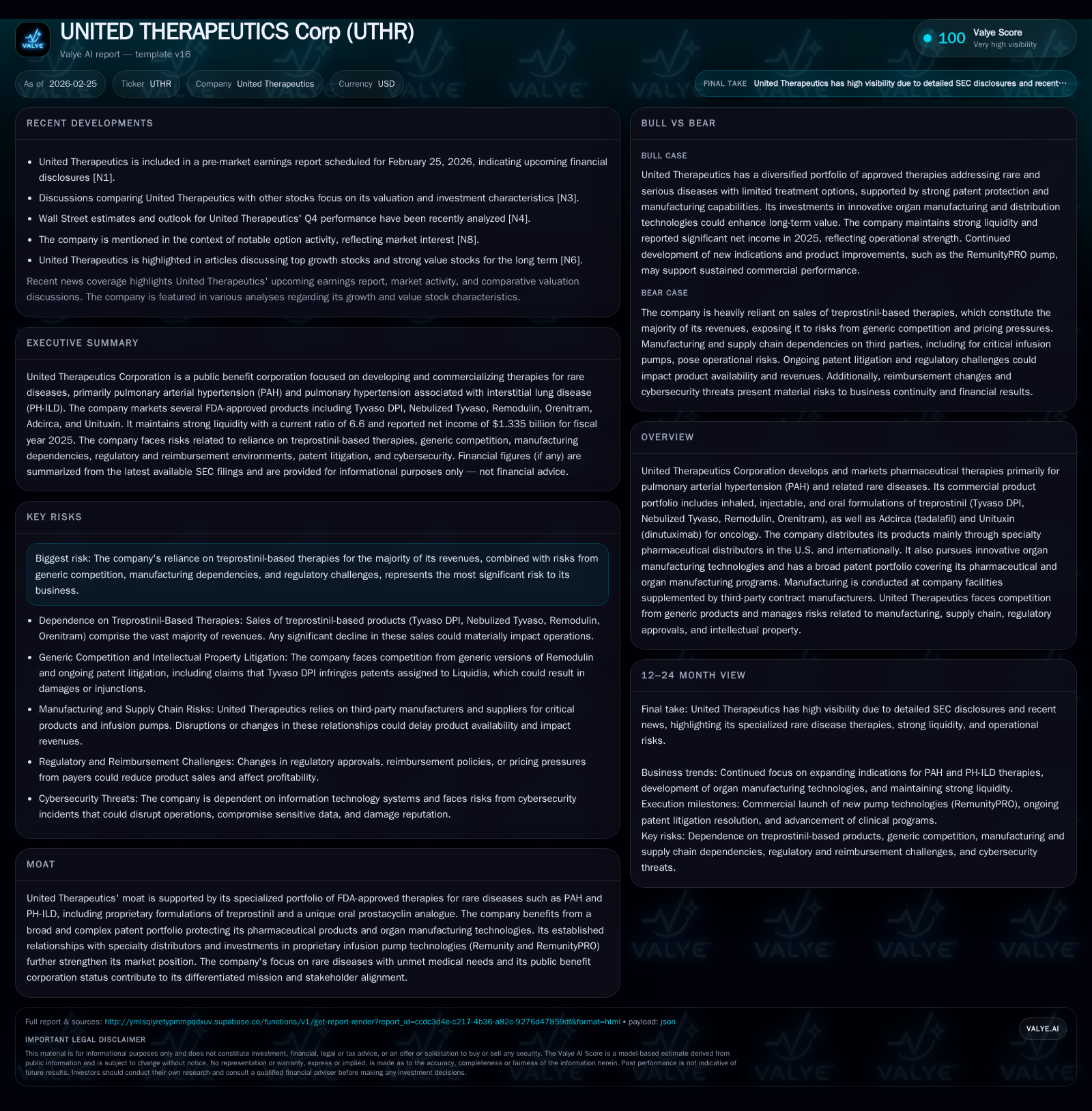

United Therapeutics’ Historic Reliance on Treprostinil Amid Expansion in Organ Manufacturing

United Therapeutics leverages a robust patent moat and product dominance in rare pulmonary conditions while navigating risks from generic competition and regulatory pressures.

United Therapeutics Corporation (UTHR) has achieved impressive revenue and income growth over recent years by focusing primarily on treprostinil-based therapies for pulmonary arterial hypertension (PAH) and related rare diseases. The company benefits from a dense patent portfolio, specialty distribution partnerships, and unique infusion pump technology, securing a competitive moat in a challenging biotech landscape. Going forward, growth opportunities lie in expanding organ manufacturing technologies and further indications like PH-ILD, but persistent risks from generics, regulatory scrutiny, and reimbursement reforms temper upside potential. Capital allocation has focused on share repurchases alongside significant reinvestment in facilities supporting its innovative pipeline. Close attention is warranted to new drug approvals, litigation outcomes on patents, and evolving pricing regulations that could materially influence operational momentum.

Historical Performance and Growth Drivers

United Therapeutics has demonstrated marked growth throughout the last half-decade primarily driven by its suite of treprostinil-based therapies targeting pulmonary arterial hypertension (PAH) and pulmonary hypertension associated with interstitial lung disease (PH-ILD). Revenues surged from $311 million in 2019 to approximately $1.48 billion recorded in 2020 [F1]. Operating income grew correspondingly from $979.7 million in 2022 to $1.49 billion by fiscal year-end December 31, 2025, an 8.4% year-over-year improvement versus the prior year [F1]. Net income rose solidly to $1.33 billion in FY2025, an increase of about 11.7% YoY reflecting operating leverage despite ongoing investment in manufacturing capabilities [F1].

Underlying this financial performance is United Therapeutics' dominant market position with treprostinil products — including Tyvaso DPI inhalation powder, nebulized Tyvaso solution, Remodulin injections with proprietary Remunity pumps, and Orenitram oral extended-release tablets — which together constitute the lion's share of revenue [S1]. This portfolio uniquely addresses rare disease cohorts that have historically faced limited treatment options resulting in high unmet needs.

The company's strategy of diversifying delivery modes (inhaled, injectable, oral) offers prescribers flexibility while strengthening patient adherence through dedicated infusion systems such as RemunityPRO pumps. Moreover, incremental indications like PH-ILD approval broaden addressable patient populations beyond traditional PAH [S1]. Integrated specialty distributors—primarily Accredo and CVS Specialty—play an outsized role in revenue concentration domestically [S22]. International sales benefit from collaborations with established partners distributing remodulin and unituxin across Europe, Japan, Asia, Middle East, and Latin America.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1335 | 1561 | 1493 | 521 | +11.7% |

| 2024 | 1195 | 1327 | 1377 | 247 | +21.4% |

| 2023 | 985 | 978 | 1185 | 230 | |

| 2022 | 803 | 980 | 139 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1000 | 1041 | 18.8 |

| 2024 | 1000 | 1081 | 18.5 |

| 2023 | 748 | 16.5 | |

| 2022 | 664 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY data unavailable except for latest noted increase; dividends data not available from provided tags.

Future Growth Prospects

Looking ahead, growth prospects hinge largely on expanding clinical indications within the rare disease segment as well as pioneering organ manufacturing technologies—a frontier area where United Therapeutics has invested heavily [S1]. Pipeline programs target idiopathic pulmonary fibrosis (IPF), progressive pulmonary fibrosis (PPF), alongside sustained oncology offerings such as Unituxin for high-risk neuroblastoma patients.

The company’s research into bio-artificial organs aims to alleviate transplant shortages by developing manufactured lungs suitable for transplantation—a highly complex endeavor involving tissue engineering licensed under expansive patent protections [S1]. If realized commercially at scale over the medium term, this initiative could materially diversify revenue streams beyond pharma sales while reinforcing its moat.

Nonetheless, future growth faces important constraints: United Therapeutics remains highly dependent on its core treprostinil franchise representing most revenues—repackaging these products or securing fresh patent life cycles will be essential amid intensifying generic competition threats documented by ongoing patent infringement litigation with Liquidia Pharmaceuticals over Tyvaso DPI [S8]. Additionally, evolving regulatory landscapes around drug pricing—including Medicare Part D price negotiation effects under the Inflation Reduction Act—could cap achievable pricing power or reimbursement levels going forward [S9][S27].

Regulatory Environment & Risks

United Therapeutics operates within a complex regulatory matrix spanning FDA requirements for CGMP manufacturing compliance, clinical trial oversight for new indications or formulations, marketing approval restrictions tied closely to orphan drug designations offering a seven-year exclusivity window [S16][S17][S18]. Outside the U.S., regulatory dynamics vary considerably by country often requiring local distributor engagement for approvals.

Risk factors related to government policies remain prominent: intensifying scrutiny on patient assistance programs invites possible DOJ investigations under False Claims Act allegations as well as restrictions imposed by co-pay accumulator programs limiting manufacturer support benefits [S5][S10]. Further legal risk arises from patent infringement suits that could impose royalty burdens or limit certain product sales if unfavorable [S8][S21]. Cybersecurity risks related to patient data handled through their United Therapeutics Cares program represent another emerging concern for material consequences following breaches [S8][S20].

Legislative pressures manifest through state-specific price caps or reporting mandates affecting pharmaceutical profitability broadly [S11], while multilateral importation rules create uncertainty around gaps between U.S.-market prices vs international pricing benchmarks [S9][S11]. Recent administrative flux at FDA contributes to longer review times potentially slowing new product approvals or supplemental applications impacting pipeline momentum [S23].

Financial Returns & Capital Allocation

United Therapeutics exhibits a disciplined capital allocation model evidenced by high free cash flow generation coupled with aggressive reinvestment into infrastructure expansion. For FY2025 alone, operating cash flow reached approximately $1.56 billion against capital expenditures of $520 million—a substantial upward step from prior years commensurate with scaling organ manufacturing initiatives [F1]. The implied free cash flow exceeded $1 billion annually.

Simultaneously, the company executed consistent buyback programs with $1 billion worth of common stock repurchased each year over FY2024–FY2025 after lower-level activity earlier in the decade—supporting shareholder value alongside foundational growth investments [F1]. Dividend payments are not disclosed publicly indicating retained earnings reinvested principally into R&D/manufacturing or share repurchase schemes.

With equity surpassing $7 billion by end-FY2025 and a strong liquidity profile demonstrated via a current ratio near 6.6x (current assets over liabilities), United Therapeutics maintains ample balance sheet flexibility providing resilience amidst sector volatility or unexpected capital needs [F1][S19]. Return-on-equity deployed was approximately 18.8%, reflecting profitable operations balanced against steadily growing shareholders’ equity base through retained earnings accumulation.

Note: Dividend data is not available from provided XBRL tags.

Industry Context & Competitive Positioning

Analyzing United Therapeutics within the broader specialty pharma industry underscores its defensive positioning hinged on rare disease specialization where barriers to entry arise chiefly from regulatory exclusivities and manufacturing complexity rather than scale economies alone. The company’s broad patent estate extends not only across molecule compositions but also device technologies linked to drug delivery systems—a notable domain detail underscoring ‘device-drug combination’ sophistication typical of advanced prostacyclin analog therapies used here.

Specialty distributors serve a similar role to wholesalers but add clinical expertise and logistical capabilities tailored for handling complex biologic treatments necessitating temperature controls and patient education support systems; reliance on two major U.S.-based distributors disproportionately affects revenue cadence timing due to inventory order volatility rather than smooth end-patient uptake alone [S22].

Globally, payor pressure around pharmaceutical costs has spawned intricate rebate architectures possibly compressing realized net prices despite list price increases being recorded—the effect amplified under government health care plans that control formulary access tightly emphasizing cost-effectiveness and comparative efficacy debates common within orphan drug segments.

Monitoring Points & What To Watch

Absent explicit guidance on upcoming quarterly or annual milestones beyond routine filing schedules ([N7],[N3]), close market monitoring should focus on:

- Progression of organ manufacturing research toward clinical proof-of-concept or commercialization pathways,

- Resolution timelines related to Liquidia patent challenges,

- Emerging legislative actions especially those impacting Medicare Part D rebate frameworks,

- Adoption rates for next-generation delivery devices like RemunityPRO,

- New indication approvals expanding patient populations served including PH-ILD or progressive fibrotic lung disease,

- Competitor moves within treprostinil analogs or biosimilars,

- Governmental investigations outcomes related to patient assistance programs and pricing compliance enforcement.

Summary

United Therapeutics sits at an intriguing intersection of late-stage specialty pharmaceuticals combined with innovative biotech-enabled organ manufacturing ambitions—leveraging decades-long leadership in a tightly regulated niche disease space marked by high entry barriers but rising vulnerability from external policy pressures. The company's financial strength backed by consistent profitability coupled with aggressive capex into futuristic platforms signals confidence but underscores inherent tradeoffs balancing present cash flow generation versus heavy reinvestment cycles.

Complexities arising from regulatory uncertainty around pricing reforms alongside intensifying legal contestations mean that sustaining long-term dominance will demand nimble adaptation augmented by successful diversification beyond legacy drug franchises into transformative cell therapy areas including manufacturable organs—the latter being a potentially groundbreaking paradigm shift if commercialized successfully.

This analysis is based solely on historical factual data sourced from SEC filings ([S#]), news reports ([N#]), and structured financial data ([F1]). It does not constitute investment advice nor any recommendation regarding securities of United Therapeutics Corporation. Readers should independently verify data points before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments