INNOVATE Corp. Extends Debt Maturities While Advancing Its Medical Device Portfolio

INNOVATE Corp.’s latest quarter highlights strategic refinancing and FDA approval events shaping its liquidity management and growth outlook.

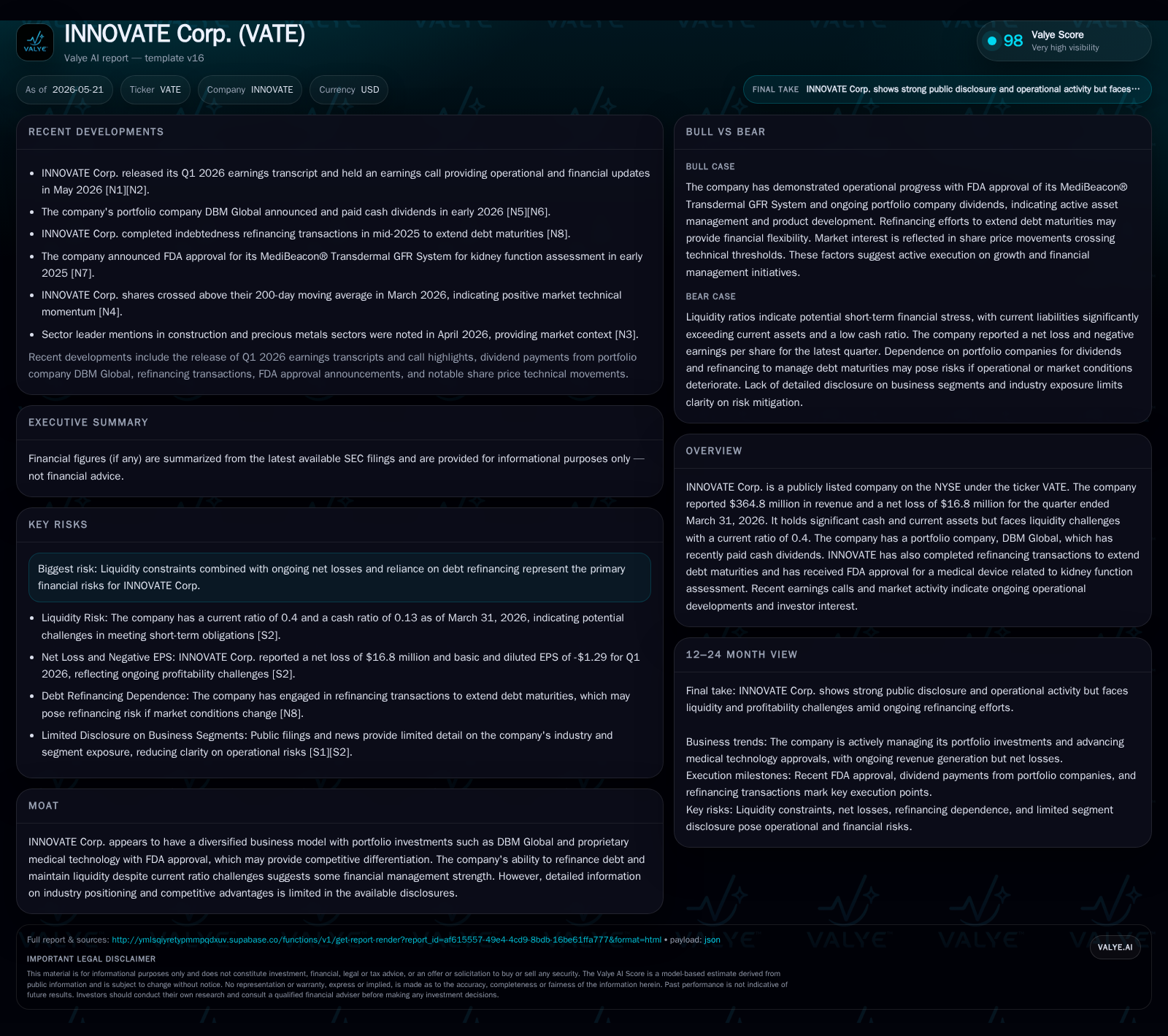

INNOVATE Corp.’s Q1 2026 filings reveal key developments including debt refinancing extending maturities and increased financial flexibility amid liquidity challenges. The company’s recent FDA clearance of its proprietary kidney function assessment device marks a significant product milestone supporting future commercial expansion. Portfolio investments like DBM Global contributed stable dividend income, partially offsetting operational losses. However, ongoing net losses and a low current ratio underscore liquidity risks requiring monitoring through upcoming execution of growth initiatives and balance-sheet management.

Recent Quarter Operational Highlights and Their Significance

INNOVATE Corp.’s most recent quarterly filing dated May 14, 2026 [S2] reveals pivotal operational updates vital to understanding the company’s near-term trajectory. Foremost among these was the completion of refinancing transactions extending the maturities on existing debt obligations [S3]. This action provides immediate relief against looming liquidity pressures by alleviating short-term cash outflows tied to debt repayments.

In parallel, INNOVATE disclosed receiving FDA approval for its transdermal Glomerular Filtration Rate (GFR) monitor device [S18]. This regulatory milestone marks a crucial validation step for its proprietary medical technology platform focused on non-invasive kidney function assessment—the first of its kind cleared for commercial use. Complementing this development was the announcement that its portfolio company, DBM Global (a construction infrastructure entity), paid cash dividends during the quarter [S15], contributing positively to consolidated cash flows.

These movements converge to highlight an operating picture balancing financial strain with tangible asset-backed growth prospects. The refinancing extends the company’s liquidity runway despite an uncomfortably low current ratio (approximately 0.4) that signals significant working capital challenges [F1]. Moreover, the FDA clearance evidences progress toward product-market fit for medical devices in a competitive life sciences landscape.

Business Model and Revenue Drivers: Portfolio Investments and Proprietary Medical Devices

INNOVATE Corp operates a hybrid business model combining portfolio investment income with revenues from proprietary medical technologies as detailed in its 10-K filing dated March 26, 2026 [S1]. The portfolio segment, typified by subsidiaries like DBM Global, generates steady cash dividends often reflecting infrastructure contracting activities. Such distributions constitute a reliable albeit cyclical income stream influenced by construction project timing and contract pricing.

On the other hand, INNOVATE’s medical devices division centers on innovative life sciences products such as the transdermal GFR monitor system. Revenue here stems primarily from sales or licensing agreements secured post-regulatory approvals such as FDA clearance [N1]. Pricing power in this segment benefits from regulatory barriers to entry and technological differentiation facilitated by intellectual property protections noted in filings [S1].

Together, these two revenue engines serve distinct customer bases: institutional investors or operators in infrastructure markets provide capital through dividends; healthcare providers or device purchasers underpin medical tech sales. The diversification offers risk mitigation via multiple revenue pools but requires effective capital allocation to support both portfolio maintenance and ongoing R&D or commercialization expenditures.

Competitive Positioning within Life Sciences and Infrastructure Segments

In life sciences technology—particularly FDA-regulated medical devices—INNOVATE confronts intense competition characterized by rapid innovation cycles and substantial regulatory hurdles [S1]. Its cleared transdermal GFR system situates it as a niche player addressing nephrology diagnostics through less invasive means compared to traditional lab tests or imaging.

The ability to obtain approvals such as CE Mark in Europe [S21] besides FDA clearance aids international expansion potential but puts emphasis on timely execution of market entry strategies amid competitors advancing alternative solutions.

Meanwhile, infrastructure-related operations reflected through DBM Global contend with cyclicality related to construction contract availability and commodity price volatility (e.g., steel tariffs) [S1]. The mixed fixed-price versus cost-plus contract structures add margin uncertainty, while project execution risks can affect backlog realization. INNOVATE’s financial management demonstrated by refinancing efforts indicates some capability to navigate these capital-intensive segments under stress [S2].

Growth Catalysts: FDA Approval, Dividend Income, and Debt Refinancing

Several actionable growth vectors emerge from recent disclosures:

- FDA Approval Commercialization: The December 2025 FDA clearance of the MediBeacon Next Generation TGFR™ system unlocks a path toward penetrating nephrology markets with novel diagnostics [S18]. Coupled with subsequent European CE Mark accreditation [S21], this creates a multi-jurisdictional launch platform potentially supporting incremental revenues over coming quarters.

- Portfolio Dividend Stability: Cash dividends declared by DBM Global contribute positively to INNOVATE’s liquidity profile during periods when core operations are loss-making [S15][N2]. Maintaining or growing these dividend flows could be instrumental for steady cash generation.

- Debt Refinancing: Recent maturity extensions alleviate immediate funding pressures while preserving operational continuity [S3]. This provides breathing room to focus capital on scaling commercialization efforts without pressing liquidity constraints disrupting business execution.

Together these drivers connect concrete KPIs: timely ramp-up of sales volumes for devices post-launch, sustaining or increasing dividend yield percentages from portfolio entities, and adherence to refreshed debt service schedules ensure balanced support for top-line growth alongside financial stability.

Financial Health: Liquidity Constraints and Debt Management

INNOVATE’s March 31, 2026 balance sheet shows $134.6 million in cash and equivalents and total debt of approximately $68.8 million, resulting in a net cash position of about $65.8 million [F1]. The current ratio stands at approximately 0.4, reflecting current assets of $405.9 million against current liabilities of $1.02 billion [F1].

Refinancing initiatives announced during Q1 effectively defer debt maturities granting tactical relief but do not fully address overarching working capital demands [S3]. Notably:

- Substantial doubt persists about going concern viability owing primarily to challenging working capital adequacy.

- Obligations under secured notes impose limitations on cash uses including restricted payments impacting shareholder returns.

- Market dynamics intensify competitive pressure particularly in life sciences units facing entrenched players investing heavily into next-generation diagnostics technology.

- Infrastructure-related segments are sensitive to construction backlog volatility and raw material cost inflation introducing earnings unpredictability.

- Reliance on successful deployment of new products introduces execution risk against demanding regulatory environments.

These factors collectively underscore material uncertainties necessitating vigilant balance-sheet oversight paired with focused operational delivery efforts under stringent resource conditions.

Upcoming Milestones and Monitoring Points

Investor attention should prioritize several upcoming milestones:

- Quarterly Financial Results: Subsequent quarters will reveal momentum shifts particularly if margins improve or shrink driven by device sales ramp or portfolio income changes [N2].

- Commercial Launch Progress: Market adoption rates and reimbursement acquisition status for the FDA-approved TGFR system are critical indicators of scalable revenue generation potential [S18].

- Dividend Announcements: Continuity or growth in dividends from DBM Global will materially affect consolidated free cash flow assumptions moving forward [S15][N16].

- Debt Covenant Compliance: Monitoring covenant adherence post-refinancing is essential given leverage sensitivities embedded in credit facilities [S3].

- Potential Asset Sales: Should liquidity deteriorate further execution of asset divestitures may become necessary per contractual requirements outlined in secured financing agreements [S1].

These checkpoints offer actionable insight into whether INNOVATE can transition from managing constraints toward realizing organic growth initiatives embedded within its diversified operations.

Disclaimer: This report is an industry analysis based strictly on publicly available filings and news sources regarding INNOVATE Corp. It does not constitute investment advice or research views concerning any securities mentioned herein.

Financial position in context

As of 2026-03-31, companyfacts shows $135 million in cash and equivalents and $69 million of total debt [F1]. The same snapshot implies net debt of roughly negative $66 million, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $406 million and current liabilities of $1.02 billion imply a current ratio near 0.4x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments