Valens Semiconductor’s Growth Faces Tradeoff Between Automotive Shrinkage and Cross-Industry Recovery

Recovery in audio-video markets boosts revenues while automotive sales decline and operating losses persist.

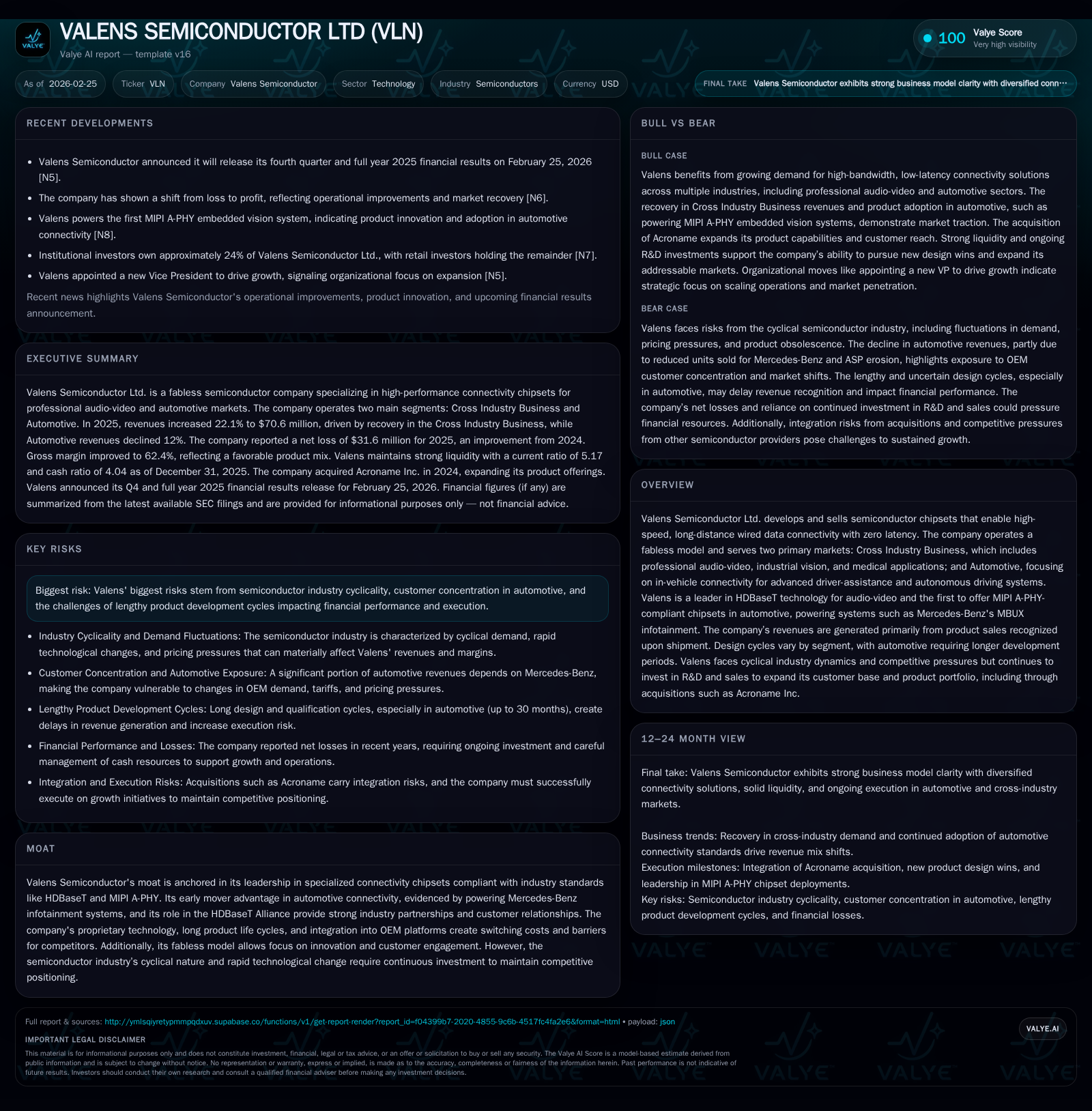

Valens Semiconductor Ltd. experienced a 22% revenue increase in 2025, driven primarily by a robust rebound in its Cross-Industry Business segment which includes professional audio-video and industrial vision. This growth was offset by a 12% decline in automotive revenues due to reduced deliveries and ASP compression in its Mercedes-Benz infotainment chipset business. Despite revenue gains, the company reported significant operating losses and negative cash flow from operations, reflecting ongoing R&D investments and cyclical semiconductor industry pressures. Valens continues investing in next-generation chipsets and expanding design wins, but execution risk remains due to the long automotive design cycles and customer concentration.

Company Overview and Industry Position

Valens Semiconductor Ltd. is a fabless semiconductor company that specializes in high-speed wired data connectivity chipsets with zero latency, serving mainly two segments: Cross Industry Business (audio-video, industrial vision, medical) and Automotive (in-vehicle connectivity for ADAS and autonomous driving). The company is notable for its leadership in the HDBaseT standard within the audio-video sector and pioneering MIPI A-PHY-compliant automotive chipsets powering systems such as Mercedes-Benz’s MBUX infotainment platform [S1][S20].

The semiconductor environment is inherently cyclical with rapid technological evolution, making continuous innovation through R&D investments critical for Valens to maintain its moat—anchored on proprietary technology, strong OEM relationships, industry alliance participation (e.g., HDBaseT Alliance), and product life cycles spanning multi-year horizons [S20][S29].

Historical Performance: Drivers of Growth and Profitability

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 71 | -32 | -13 | -34 | +22.1% | +13.7% |

| 2024 | 58 | -37 | 1 | -41 | -31.3% | -86.1% |

| 2023 | 84 | -20 | -6 | -27 | -7.2% | +28.9% |

| 2022 | 91 | -28 | -22 | -28 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 24 | -14 | -30.1 |

| 2024 | 1 | -1 | -25.6 |

| 2023 | -8 | -12.0 | |

| 2022 | -23 | -16.5 |

Source: SEC companyfacts cache [F1].

*Note: Revenue dipped significantly in 2024 due to inventory digestion effects across the industry as well as softer demand [S9][S10][F1].

Revenue trends were characterized by a sharp downturn in 2024 amid industry-wide inventory corrections, affecting especially the Cross Industry segment with slower inventory movement post-semiconductor shortage normalization [S9][S10]. Revenues recovered strongly in 2025 (+22%), predominantly driven by a 42% surge in Cross Industry revenues ($51.7M vs $36.3M prior year). In contrast, automotive revenues declined by about $2.6 million (-12%), reflecting falloff in unit shipments linked mainly to Mercedes-Benz passenger cars and pricing pressure on ASPs [S5][S9].

Gross margin improved modestly to over 62%, benefiting from a higher share of the higher-margin Cross Industry products (68%) versus Automotive (47%) which generally carry thinner margins due to the complex design requirements associated with compliance for safety-critical applications [S5][S11].

Operating losses decreased approximately $7 million from $41 million in 2024 to $34 million in 2025 but continued to reflect heavy investment levels across R&D (increasing ~5%) supporting enhancement of existing families as well as new chipset developments targeting ProAV markets [S8][S14]. SG&A expenses grew moderately +17%, notably fueled by expanded sales & marketing activities aligned with growth acceleration in non-automotive verticals [S14].

Operating cash flow remained negative at ($12.7M) versus positive cash flow generation at $1M in the prior year which benefitted from non-recurring working capital improvements; capex spending declined substantially (-43%) indicating a shift from earlier development-heavy phases toward more capital-light operations as production matures [F1][S18][S25].

Share repurchases totaled approximately $24 million during calendar year 2025 under two active buyback programs initiated since late 2024 aimed at reducing share count amid volatile stock price conditions [S7][F1]. This sizable buyback reflects confidence from management while grappling with earnings pressure.

Future Growth Prospects: Catalysts and Constraints

Valens’ future growth hinges on several interrelated factors:

Continued growth of Cross Industry segment: The professional audio-video market benefits from strong secular trends such as increased video conferencing adoption, digital signage proliferation, industrial vision automation, and medical endoscopy applications leveraging advanced connectivity solutions based on HDBaseT technology [S20][N12][N13]. Shorter design cycles (~6-12 months) allow quicker monetization of innovations in this segment compared to automotive.

Expansion of automotive chipsets: The Automotive business presents both opportunity and challenge; Valens currently leads MIPI A-PHY connectivity solutions used widely for ADAS/ADS cameras and sensor fusion architectures pivotal for autonomous features [S20][S28]. However, this business experienced a recent decline in Mercedes-Benz-related volumes possibly tied to car production slowdowns or model refresh timing influencing chip ramp-ups [S9]. Design cycles are long (~3+ years), so near-term growth depends on onboarding new OEM partnerships along with expanded system architectures beyond infotainment into ADAS sensor zones.

Technological innovation: Investment in next-generation chipsets like the VA7000 ProAV family aims to integrate multiple high-bandwidth interfaces including USB3 extension via acquisitions like Acroname enhancing product portfolio breadth and depth – essential to staying ahead of rapid industry shifts toward converged connectivity demands [S8][N8][N13].

Risks include semiconductor market cyclicality impacting demand patterns, potential delays or failures in achieving new design wins particularly within automotives where long qualification periods impose upfront costs without immediate returns, as well as customer concentration risk given dependence on key OEMs such as Mercedes-Benz [S29]. Changes in tariffs or supply chain disruptions could further weigh on automotive segment performance.

Forecasts, Milestones, And What To Watch Next

The company provided no explicit formal guidance for FY2026 but flagged ongoing robust demand momentum within the Cross Industry business and cautious outlook given automotive uncertainties [N5][N6][N7]. Key milestones include ramping production volumes of next-gen AV chipsets later this year alongside pursuing additional strategic design wins across both verticals.

Analysts watching Valens should monitor:

- Revenue mix evolution between segments as it significantly impacts margins.

- Gross margin trajectory amidst product ASP changes and manufacturing improvements.

- Impact of share repurchase activity on earnings per share metrics.

- Quarterly order book strength particularly from automotive OEM pipeline developments given longer lead times.

- R&D spending trends signaling technology roadmap progress or cost control efforts.

Returns And Capital Allocation Policy

Despite recurring net losses over recent years ranging from ($19M) to ($36M), Valens is sustaining R&D investment intensity (~$43M total R&D spend in FY25) deemed necessary for future competitiveness [F1][S14]. Operating losses have narrowed gradually but remain significant relative to revenue scale.

Capital allocation includes aggressive share repurchases totaling $25 million during fiscal years ending December 2024–25 while maintaining sufficient liquidity ($27.8M cash & equivalents; current ratio >5x) ensuring operational runway without debt leverage [F1][S15][S19]. The company does not currently pay dividends given negative earnings profile.

ROE remains negative around -30% reflecting ongoing investment phase rather than profitability focus at this stage [F1]. On delayed free cash flow basis (CFO minus Capex), Valens generated roughly negative $13.8 million free cash flow highlighting continued cash burn mitigating short-term returns but positioning for medium-term growth leadership.

Sector Analysis: Context For Valens’ Competitive Dynamics

The semiconductor connectivity sector thrives on technical standards adherence (HDBaseT, MIPI A-PHY), low-latency data transfer capability over long-reach cables, required for emerging applications across professional AV installs and increasingly sophisticated vehicle networks supporting zonal architectures. The complexity escalates particularly within automotive where electromagnetic immunity tests, rigorous certification cycles up to two years or more extend product introduction lead times. Moreover, incremental bandwidth needs are growing exponentially driven by camera-based sensor fusion systems indispensable for autonomous driving safety functions. Fabless models like Valens focus intensely on IP development and software integration partnerships rather than capital-intensive fabrication plants — agility balanced against competitive pricing pressures characterizes margin challenges here.

Summary Conclusion

Valens Semiconductor is navigating a recovery phase marked by solid growth acceleration outside automotives which partially offsets structural declines within its key car platform revenue streams tied to Mercedes-Benz installations. Substantial investments sustain its technical edge amid cyclical semiconductor headwinds imparting ongoing operating losses though improving gradually. Execution progress on next gen chipsets combined with escalating distribution footprints across Cross Industry verticals demonstrates tangible catalysts but long automotive lead times introduce uncertainty into near term financial outlook. Capital discipline exhibited through sizeable stock repurchases reflects management conviction amid extended loss-making window. Observers should closely track order books, design win momentum particularly beyond legacy automotive customers, gross margin dynamics affected by shifting product mixes plus ongoing R&D efficiency measures throughout FY26 onwards.

This report is intended solely for informational purposes regarding Valens Semiconductor Ltd.'s financial condition and industry position as reflected through public regulatory filings and market data up to early 2026 without evaluation or recommendation concerning securities transactions or holdings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments