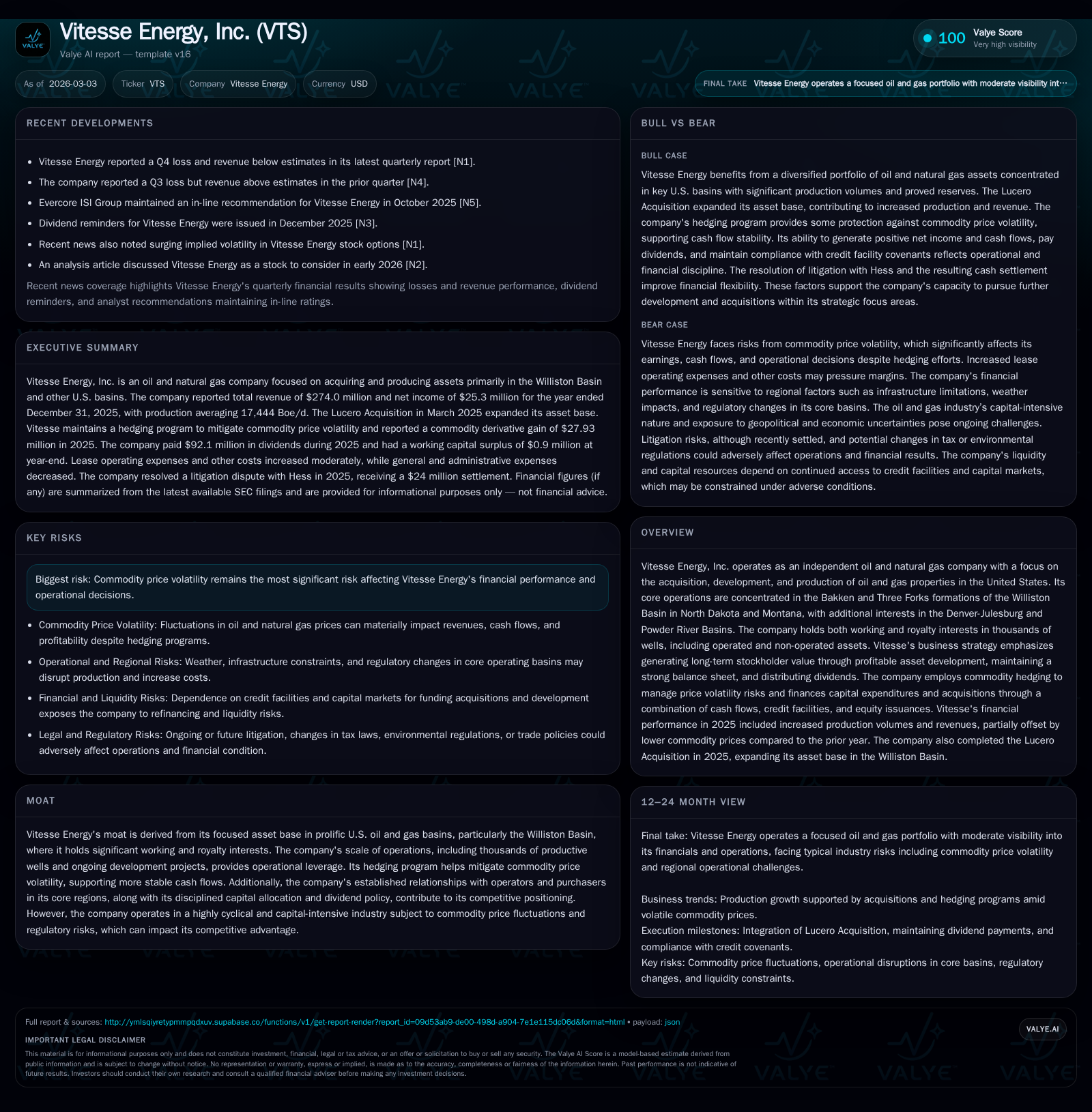

Vitesse Energy's Strategic Growth and Financial Resilience in the Williston Basin

Focused asset development, disciplined capital allocation, and hedging underpin Vitesse Energy’s stable cash flow despite volatile commodity prices.

Vitesse Energy has leveraged the 2025 all-stock Lucero Acquisition to expand its footprint in the prolific Bakken and Three Forks formations, growing production and reserves. Despite a sharp 58% decline in operating income due to market conditions, net income improved 20%, supported by operational scale and a robust hedging strategy. The company maintained disciplined capital spending and returned over $92 million in dividends, sustaining financial resilience with modest leverage and compliance with debt covenants. Monitoring commodity price trends, capital expenditures, and permit approvals will be critical for near-term operational momentum.

Historical Performance: Growth Drivers and Lucero Acquisition Impact

Vitesse Energy’s financial trajectory over recent years illustrates a nuanced balance between acquisition-led production expansion and cyclical commodity headwinds. In calendar year 2025, the company reported operating income of $17.1 million, marking a steep decline of approximately 58.2% compared to $40.9 million in 2024 [F1]. This contraction reflects external market challenges including oil price volatility compounded by global geopolitical tensions enumerated in their SEC disclosures [S1]. However, net income exhibited a contrasting improvement rising by 20% year-over-year to $25.3 million in 2025 from $21.1 million the prior year [F1]. This uptick is attributable largely to enhanced scale from the March 7, 2025 Lucero Acquisition—a transformative all-stock transaction adding operated assets primarily in the Bakken and Three Forks formations within the Williston Basin [S1][N1]. Lucero shareholders exchanged over 8.1 million shares for Vitesse common stock, augmenting Vitesse’s footprint.

Cash flow from operations grew nearly 10% to $170.3 million in 2025 compared to $155 million in 2024, which combined with reduced capex ($25.4 million versus $77.7 million), strengthened free cash flow available for dividends and debt servicing [F1][S24]. Production averaged around 17,444 barrels of oil equivalent per day (Boe/d), with oil constituting approximately 65%, underscoring operational heft achieved post-acquisition [S1]. The proved reserves augmented to nearly 47.8 MMBoe with an estimated PV-10 value of $473 million consolidating Vitesse’s competitive resource base [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 25 | 170 | 17 | 25 | +20.0% |

| 2024 | 21 | 155 | 41 | 78 | +206.7% |

| 2023 | -20 | 142 | 35 | 46 | -116.6% |

| 2022 | 119 | 147 | 154 | 21 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 92 | 0 | 145 |

| 2024 | 64 | 0 | 77 |

| 2023 | 58 | 248000 | 96 |

| 2022 | 126 |

Source: SEC companyfacts cache [F1].

Table excludes revenue data where unavailable; capex reduction reflects strategic spend adjustment post-acquisition.

Commodity Price Volatility: Effects on Earnings and Operations

Commodity prices remain the most significant determinant of Vitesse's operational results as acknowledged explicitly in its risk disclosures [S1][S13]. Global macroeconomic unpredictability including conflict zones (Ukraine-Russia war), OPEC+ quota changes, inflationary pressures elevating operational costs, and strategic petroleum reserve activities continue influencing oil price fluctuations [S1]. These dynamics directly impact operators’ drilling activity decisions and Vitesse’s acquired operators’ capital deployment.

To attenuate such variability, Vitesse implements rigorous hedging covering a substantial portion of its proved developed producing (PDP) volumes consonant with credit facility mandates [S4][S20]. At December-end 2025, derivative contracts encompassed roughly 40-50% of anticipated PDP production over forthcoming quarters through swaps and collars primarily on oil and natural gas volumes—well-aligned with covenant requirements enforcing minimum hedge coverage ratios adjusted according to facility utilization percentages [S4]. This hedging framework smooths realized cash flows aiding operational planning amidst volatile benchmark prices.

Focused Asset Base: Exploiting Bakken & Three Forks Formations

Vitesse's core asset portfolio centers on working interests across approximately 6,402 gross productive wells (226.1 net), underscoring scale advantages within Bakken and Three Forks plays of North Dakota and Montana’s Williston Basin with additional non-operated interests across Denver-Julesburg and Powder River Basins [S1][S10]. Its asset composition includes operated and non-operated properties offering diversified exposure yet maintaining concentrated geological focus.

The company also holds royalty interests in approximately 1,301 gross productive wells (3.2 net), creating additional revenue streams without direct capital outlay risks [S1]. Such a mix provides balanced exposure to development upside while permitting capital discipline.

Capital Allocation: Dividends, Capex Trends, and Leverage Management

Capital deployment reflects careful prioritization balancing growth investments with investor returns amid profitability pressures [F1][S12]. Dividend distributions were notably robust at $92.1 million in FY2025 compared to prior year’s $63.6 million despite lower operating income, underscoring reliance on operating cash flow rather than reported profits alone for shareholder returns [F1][S24]. Buybacks were negligible since early share repurchases ceased following spin-off phases.

Capital expenditures contracted sharply by more than two-thirds (-67%) year-over-year reflecting a pullback from elevated drilling activity levels seen in previous periods partly due to market sentiment uncertainties—$25.4 million spent on development/acquisition versus $77.7 million in FY24 [F1][S26][S28][S29]. Lower capex spend aligned with improved free cash flow generation (~$145 million approximated as CFO minus capex), facilitating dividend maintenance without excessive leverage buildup.

Leverage remains prudent with total debt at $124.5 million against equity base exceeding $629 million at end-2025 resulting in modest gearing ratios; company stayed compliant with revolving credit facility financial tests governing debt-to-EBITDAX limits not exceeding multiples of three times at reporting date [F1][S4][S11]. Current ratio approximated unity at about 1.02 indicating adequate working capital sufficiency aided by better receivables collection post-litigation settlement inflows [F1][S14][S23][S24].

Return on equity is modest but positive near ~4%, reflective of constrained earnings amid cyclicality but stable equity foundation cushioned by acquisitions expanding asset base [F1].

Hedging Strategy: Mitigating Commodity Risk for Stable Cash Flows

Derivative instruments form an integral risk management tactic consistent with upstream sector practices facing volatile price environments [S4][F1]. Per their revolving credit facility terms effective through late-2028 maturity, Vitesse is obligated to hedge no less than approximately 40% of PDP production for near-term quarters when borrowing utilization is low (<50%), scaling up hedge coverage above half of expected output for higher utilization bands—ensuring downside protection consistent with lender risk appetite [S4].

Current positions include oil swaps averaging floor prices around mid-$50s per barrel providing revenue floors even if spot prices drop materially; similarly natural gas collars mitigate thermal fuel pricing swings realized predominantly at Chicago City Gate benchmarks relative to Henry Hub indices [S20]. This structured approach delegates some price upside retention while locking minimum cash flow critical for sustaining dividends and capital planning.

Future Growth Outlook: Development Plans and Market Risks

Post-acquisition growth hinges on executing permitted well inventories totaling several hundred gross units inclusive of multi-basin portfolios, subject to operator scheduling decisions outlined by joint venture partners or internal operatorship plans [N1][S1]. Inflationary headwinds elevating rig rates, labor scarcity exacerbating service delays plus regulatory complexities may deflate drilling cadence initially envisioned—emphasizing measured capex forecast adjustments noted by management [N2][S2].

Commodity price trajectories remain uncertain given ongoing geopolitical disruptions highlighted by recent Middle East tensions alongside potential shifts in OPEC policies that could tighten or loosen supply dynamically impacting realizations thus investment horizons.

Industry-wide supply chain disruptions historically cause lag times between sanctioning permits versus well completions; therefore monitoring forward permit counts coupled with actual well spud activities will be effective near-term operational KPIs.

Financial Health: Debt Covenants, Liquidity, and Investor Returns

Liquidity metrics indicate sound footing as unrestricted cash hovered around low millions supplemented by ample credit lines under revolving credit facilities amounting up to $500 million maximum contingent commitments though actual borrowing is a fraction near $124 million drawn end-2025 illustrating cushion for unexpected needs or opportunistic purchases [F1][S4][S11].

The revolving credit facility entails standard ratio covenants including maintaining total funded debt/EBITDAX below threshold multiples generally set under threefold alongside current ratio minimums near one ensuring manageable short-term solvency risks; covenants also impose derivative contract minimum hedge coverage mandates enforced quarterly protecting lender collateral interests reflecting proved asset bases collateralized under first priority liens representing roughly equal or greater than ~85% present value of reserves per lender agreements [S4][S6][S7].

Investor returns are driven primarily via quarterly dividends sustained through robust operating cash flows rather than buybacks given cyclicality uncertainties—balance sheet strength positioning Vitesse for opportunistic capital deployments without compromising distributions or covenant breaches.

What to Watch: Near-Term Milestones and Operational Indicators

Key indicators warranting investor attention include:

- Commodity price realizations especially WTI crude trends impacting hedge effectiveness versus spot differentials influencing earnings volatility outcomes.

- Progress on permitted well completions translating into actual production volume inflections signaling developmental execution capabilities.

- Quarterly earnings announcements scrutinized against analyst estimates providing insights into margins stability amid fluctuating expenses.

- Changes or renewals in credit facility terms or borrowing base redeterminations occurring biannually potentially adjusting financial flexibility.

- Management commentary on capex budget revisions responsive to market conditions providing real-time strategic stance. These elements will prove decisive signals for assessing whether Vitesse can sustain its dual mandate of growth through asset exploitation and shareholder cash return amid commodity cycle gyrations.

This analysis synthesizes publicly available audited financials under SEC filings alongside pertinent market news without forwarding investment recommendations or speculative guidance beyond documented information sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments