NCR Voyix Corp’s Transition to Unified Commerce Platform Amid Hardware Outsourcing

Focus sharpens on retail and restaurant segments with SaaS transformation and hardware outsourcing impacting operations.

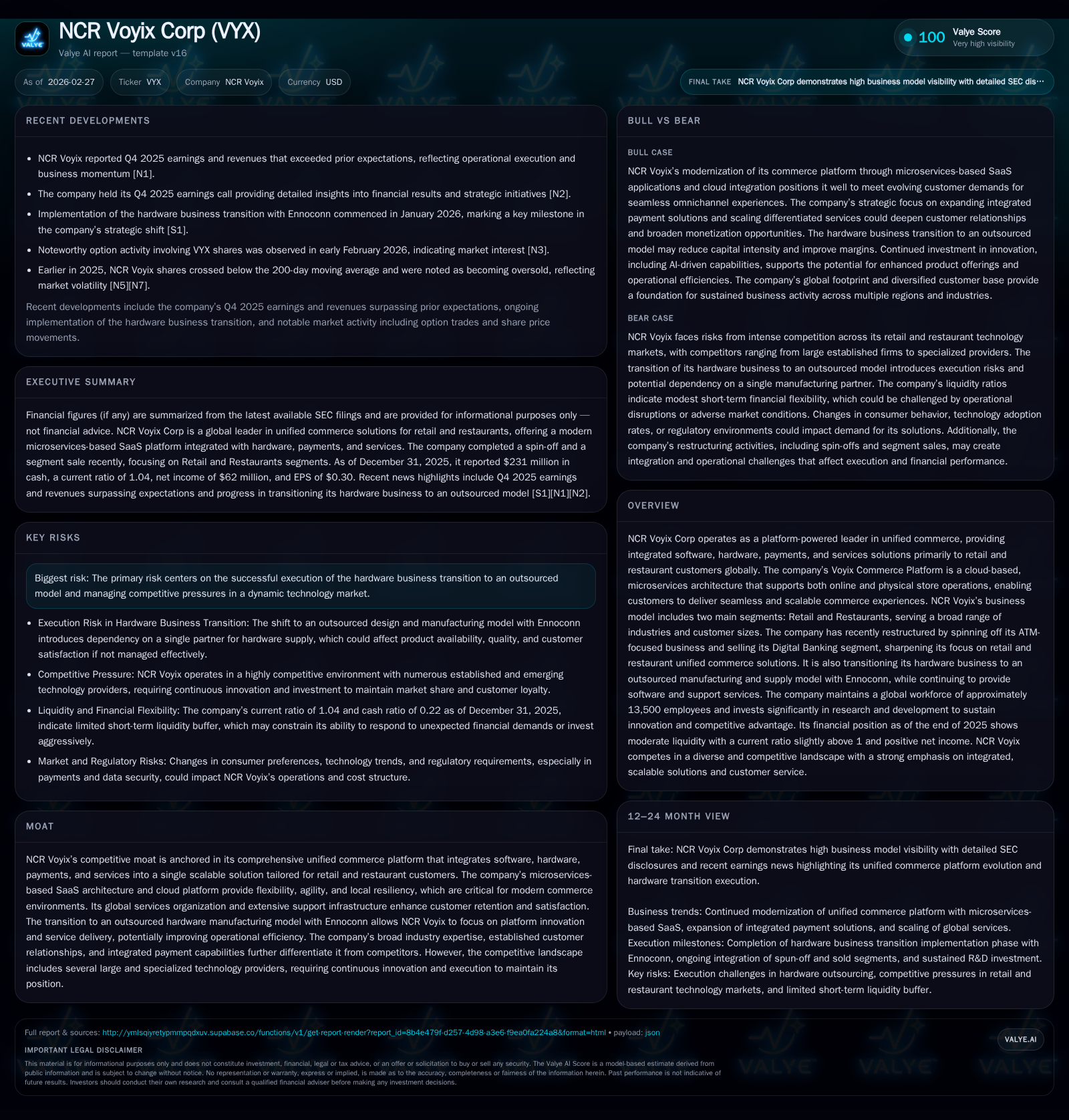

NCR Voyix Corp has strategically repositioned itself as a platform-focused leader in unified commerce, serving retail and restaurant industries globally. The company’s modernized microservices-based SaaS software portfolio, integrated payments, and comprehensive services underpin its competitive moat. It has divested non-core business lines, including spinning off ATM operations and selling Digital Banking. A key 2026 initiative is transitioning hardware manufacturing to outsourced partner Ennoconn, shifting from direct production to an agent sales model. While revenues and profitability have shown volatility historically, recent operational improvements reflect progress toward scalable growth despite ongoing execution risks in hardware transitions.

Company Overview

NCR Voyix Corporation has undergone significant strategic reshaping over the past three years to emerge as a platform-centric entity focused on unified commerce solutions for retail and restaurant customers worldwide. Historically a mixed-technology conglomerate including ATM manufacturing and Digital Banking services, NCR Voyix divested these legacy units — spinning off ATM-related businesses as NCR Atleos in late 2023 and selling its Digital Banking segment in September 2024 for $2.45 billion cash plus contingent consideration [S23]. This refocus aligns the company around integrating software-as-a-service (SaaS), payments, outsourced hardware sales, and professional services through its proprietary Voyix Commerce Platform.

Headquartered in Atlanta with approximately 13,500 employees globally across nearly 30 countries [S22], NCR Voyix seeks to address growing consumer demand for frictionless shopping and dining experiences combining digital ordering, checkout options, loyalty programs, analytics, and store operations management deployed via a cloud-based microservices architecture [S4][S6][S8][S10].

Historical Financial Performance

NCR Voyix's financial trajectory reflects significant structural transition with underlying volatility. The top-line revenue showed a steep increase between 2020 ($1.63B) and 2021 ($7.16B), reflecting prior acquisitions or business model changes [F1]. Operating income swung from a loss of -$130 million in 2023 to positive $26 million in FY2025. Net income also rebounded from -$423 million in 2023 to $62 million in FY2025 after a notable spike of $958 million in FY2024 linked to gains from the Digital Banking sale treated as discontinued operations [F1].

Operating cash flow remained negative at -$210 million in FY2025 during ongoing investments related to transformation efforts. Capital expenditures declined markedly post-transition ($30 million in FY2024 versus $130 million in FY2023) reflecting reduced direct manufacturing activities [F1]. This resulted in negative free cash flow for the period.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 62 | -210 | 26 | -93.5% | |

| 2024 | 958 | -132 | 2 | 30 | +326.5% |

| 2023 | -423 | 694 | -130 | 130 | -805.0% |

| 2022 | 60 | 447 | 489 | 92 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 74 | 6.5 | |

| 2024 | 56 | -162 | 102.7 |

| 2023 | 564 | -1692.0 | |

| 2022 | 0 | 355 | 4.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue data post-2021 is not publicly disclosed or affected by segment changes; share buybacks commenced after transformation starting FY2024.

Business Model & Segments

Following divestitures, NCR Voyix operates primarily through two reportable segments: Retail and Restaurants. The Retail segment serves convenience stores with fuel offerings, grocery chains, drugstores, mass merchandisers, department stores, and specialty retailers. The Restaurants segment targets quick-service to full-service dining operators.

Central to the offering is the Voyix Commerce Platform — a cloud-native microservices architecture powering SaaS applications that support both online and physical store operations including POS (point-of-sale), self-checkout solutions enhanced with AI/ML technologies like computer vision for fraud reduction, kitchen display systems, and back-office tools such as labor and inventory management [S10][S12][S20].

Payments are integrated end-to-end within POS/SCO systems via gateways (Voyix Connect) and processing services (Voyix Pay), enabling acceptance of diverse payment types including credit/debit cards, gift cards, fleet/fuel cards with advanced security measures like point-to-point encryption that reduce chargebacks [S7][S20].

Global service offerings include professional software deployment services alongside managed network support based on ITIL frameworks delivering comprehensive store technology management supported by worldwide field technicians [S7].

Strategic Shift: Hardware Business Transition

A key strategic initiative is the transition of point-of-sale and self-checkout hardware design and manufacturing to Taiwan-based Ennoconn Corporation under an ODM model effective January 2026 following an August 2024 agreement [N1][S23].

Under this arrangement:

- Ennoconn assumes responsibility for design, manufacturing, warranty servicing, inventory management, and direct shipping of hardware products.

- NCR Voyix acts as a sales agent earning commission revenues on these hardware sales without exposure to inventory or production risks.

- Internal focus intensifies on advancing software innovation along with service delivery including support and maintenance of these devices.

This shift aims at improving operational efficiency by reducing capital-intensive manufacturing while leveraging Ennoconn’s scale advantages but introduces execution risk regarding migration timing and quality assurance given hardware’s critical role within omnichannel commerce ecosystems [S6][S13][S25].

Growth Prospects & Innovation Focus

Leadership prioritizes expanding adoption of their enhanced SaaS portfolio powered by AI-driven analytics offering flexible modularity catering from small operators up to large international enterprises requiring multi-language & multi-currency support [S8][S11].

Innovations include embedding machine learning into self-checkout fraud detection via computer vision along with automated inventory/labor management tools enhancing retailer efficiency.

Expansion plans involve broader geographic payment acceptance networks targeting commercial fuel transactions while leveraging the extensive field services network for deeper international client penetration.

NCR Voyix holds over 900 U.S. patents protecting platform innovations which provide barriers against new entrants while selectively licensing technologies strategically [S24].

Risks & Competitive Dynamics

The company faces competition from established players such as Aptos, Oracle, Toast, Lightspeed among others across varied verticals [S9]. Competitive advantage depends on integrated software/payment/service bundles paired with evolving capabilities behind proprietary APIs.

Key risks include:

- Execution challenges during hardware business migration impacting customer satisfaction.

- Regulatory compliance complexities especially related to global payment processing increasing operational costs or scrutiny [S18].

- Technological disruption if competitors outpace innovation or pricing strategies.

- Risks associated with AI integration ensuring safety without reputational harm or errors [S25].

Historical environmental remediation liabilities exist but are not currently expected to materially impact financials given divestitures and provisions made previously [S5].

Capital Allocation & Liquidity

NCR Voyix holds approximately $231 million in cash equivalents with a current ratio near parity at ~1.04 indicating balanced short-term asset coverage over liabilities [F1][S14].

Debt financing includes senior notes maturing through the late decade maintaining manageable leverage relative to earnings capacity growth expectations [F1][S15].

Share repurchases resumed post-restructuring beginning FY2024 with $56 million deployed then increasing to $74 million in FY2025 signaling confidence in capital return aligned with strategic milestones. No dividends have been declared recently as reinvestment into R&D (~$155 million annually) continues supporting SaaS platform evolution [F1][S23][S9].

Outlook & Analytical Considerations

While precise forward guidance is limited beyond qualitative outlooks emphasizing platform adoption acceleration ([N2],[S13]), key areas warrant monitoring:

- Continued shift of revenue mix toward recurring SaaS/subscription streams versus transaction/hardware commissions post-Hardware Business Transition.

- Margin expansion driven by operating leverage as SaaS adoption grows combined with lower fixed costs due to outsourced hardware sales.

- Normalization of cash flow following completion of transition expenses critical for sustainable capital returns.

- New customer wins expanding verticals/geographies demonstrating platform scalability among enterprise clients seeking unified commerce suites.

- Progress updates regarding Ennoconn ODM partnership mitigating integration risk amid supply chain uncertainties prevalent industry-wide.

In summary, NCR Voyix stands at a pivotal juncture shaping its next phase of growth as an integrated unified commerce solutions provider enabled by cloud-native technologies while navigating inherent short-term execution risks associated with its strategic transformation.

This analysis is based solely on available public filings as of February 27th, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments